We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Mortgage broker - ask me anything

Comments

-

I was wondering if as brokers you had come across this before or could offer a comment on what options I should consider..

i am planning on moving home. Have sale agreed on both my property and on the property I am buying. The new property is more expensive and I will require additional borrowing.

With a good wind I believe the sale could complete August/September however I am on a fixed rate with my current lender until 1st Oct and so moving before will result in an early repayment charge (ERC) of 1% of the outstanding loan.

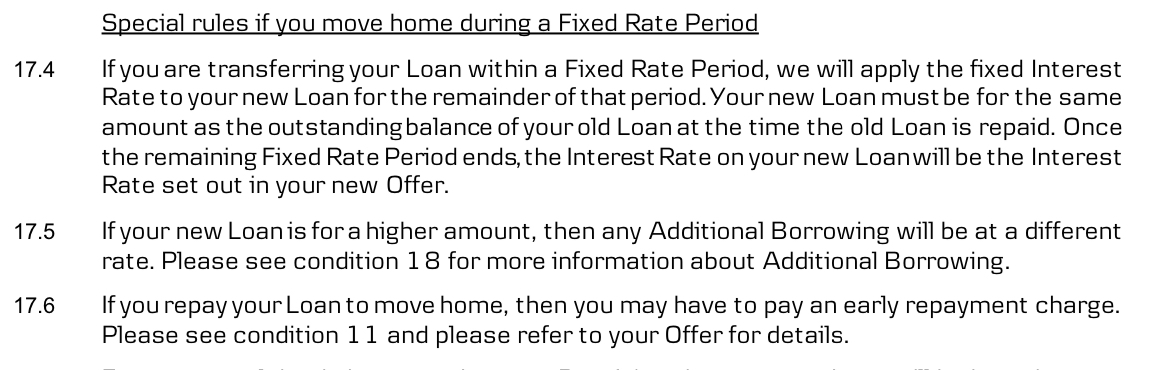

I have been told I can port the loan but this will leave me with two products and all the headaches that can cause. My understanding was as you approach the end of a fixed rate you can negotiate a new deal and if moving they can offer you new product on the whole amount of the loan and you avoid the early repayment charges. However the customer service team have told me this isn't the case.I have checked through the mortgage terms and conditions and have linked them below, I believe condition 11.11 describes exactly what I want to do but I am being told it's describing porting.Section 17 of the same terms and conditions deals with porting.I know other lenders offer what I am describing it’s set out really clearly as “option 2” on Santander’s website when you search “existing customer moving home”Whilst I accept that my lender (Danske bank) may differ I believe their terms and conditions suggest I should be able to.Because I have just joined the forum I can't post a link however I have copied the relevant section below or if you are feeling particularly helpful you could google - "Danske Bank mortgage general terms and conditions"11.11 Additional rules if you repay your loan and move home during a fixed rate period

We will not charge you an early repayment charge if all of the following conditions apply;

a) You move home and repay your loan in full during a fixed rate period;

b) We have agreed to give you a new loan secured over your new home; and

c) The new loan begins on the date your old loan is repaid.

I would appreciate any comment on the above, let me know if I am barking up the wrong tree or if I should try again with Danske.

Finally, if they insist on me either porting or paying the ERC - should I then be arranging a product transfer on my existing loan so there’s something in place to port, and at the same time arrange a home mover loan for the remainder?it all sounds messy because the PT will be based on my remaining in the current property but then the new loan would be for the new house and it feels like a difficult needs and circumstances conversation.Again would welcome any advice on how you would proceed.Cheers0 -

@martyziff Quick comments -

- the specifics of porting, switching fixes, ERC in the last few months of a fix, etc. depends on the specific lender- unless I’ve misunderstood, I’ve not heard of lenders that offer to do what you want unconditionally: pay off a fix midway through and waive the ERC if you take another fix, unless all this is linked to a port, or a non-simultaneous port (where ERC is refunded within x months), or within x months of fix end

- some lenders do waive ERC in the last X months of the fix, no idea what Danske bank’s policy is on that

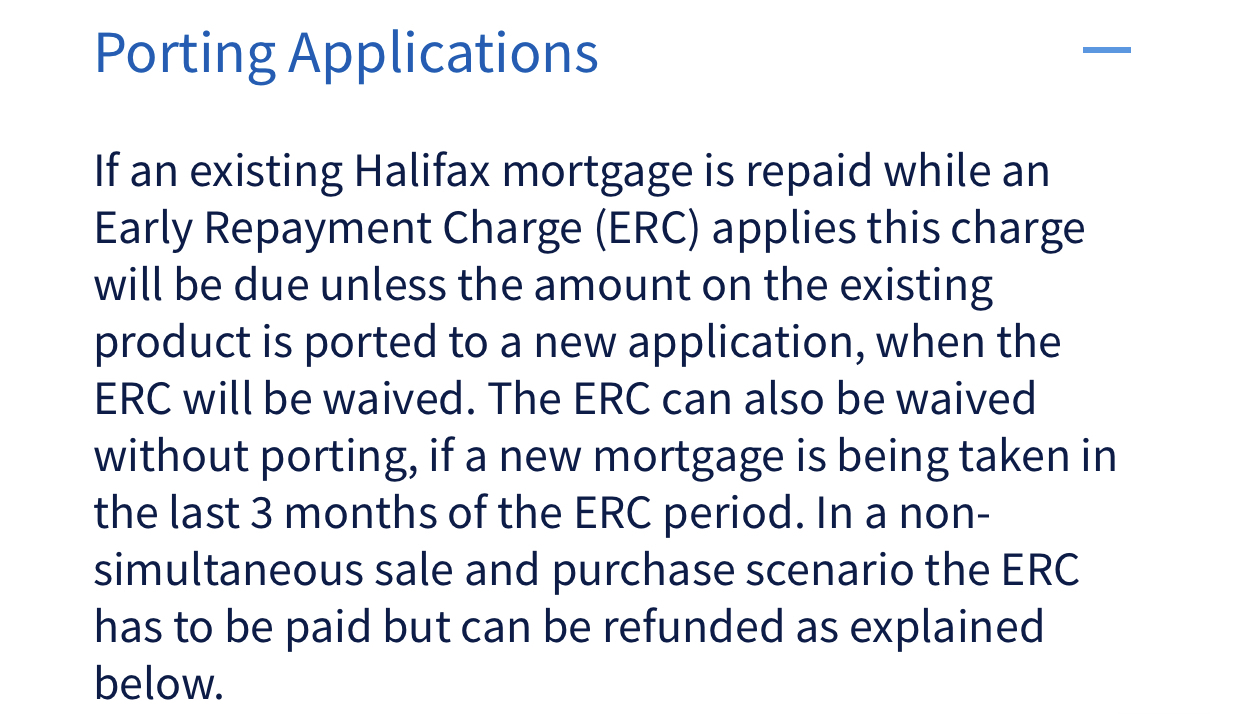

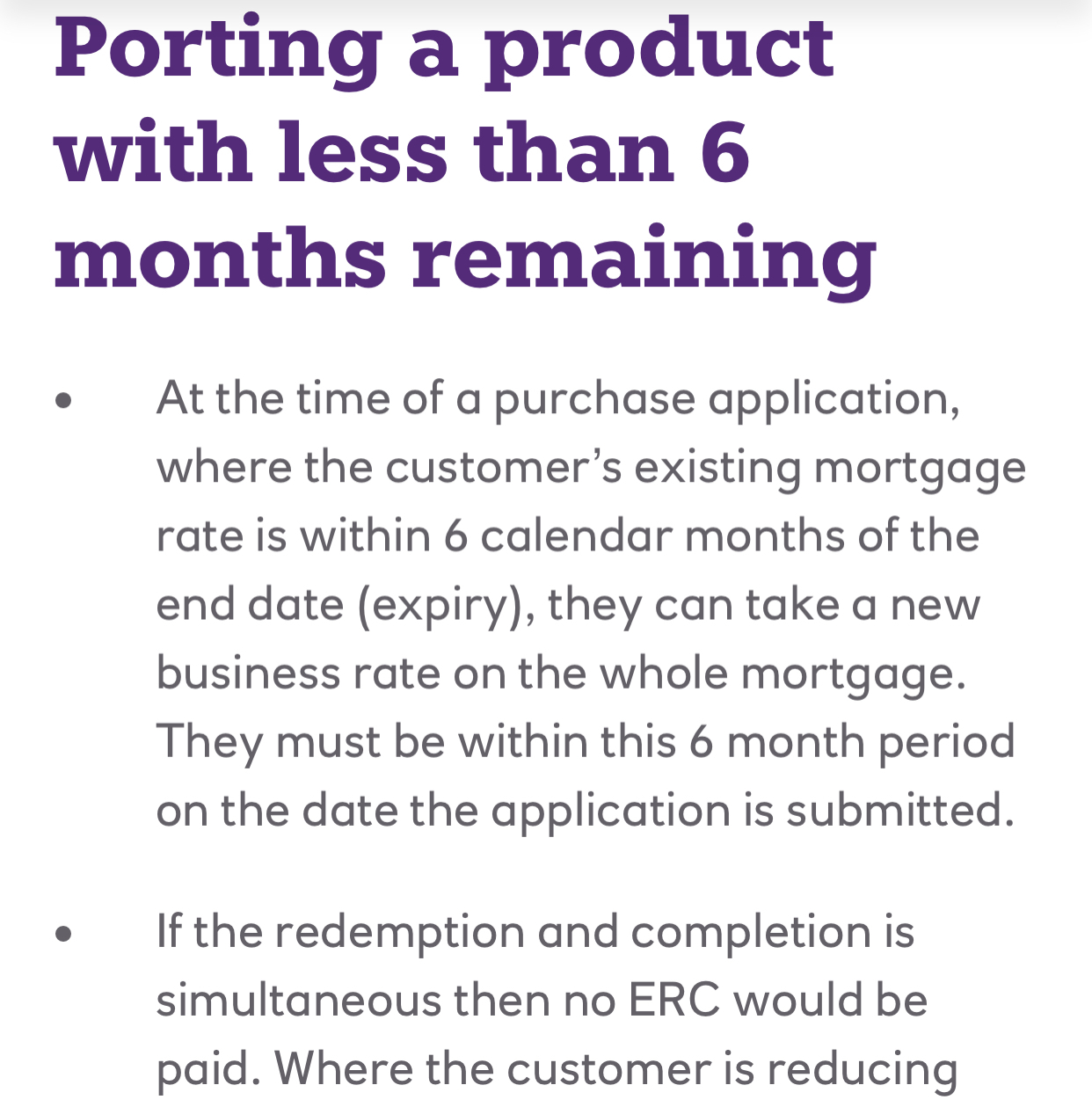

This is one example (Halifax) which illustrates the above And another (NatWest) which does what you want, in the last 6 months of the fix

And another (NatWest) which does what you want, in the last 6 months of the fix What works better for you - paying the 1% ERC and using the ‘best’ whole of market lender available to you OR port+additional with Danske, depends on the numbers, what rates are out there, how competitive Danske’s rates are, etc. It might well be that there isn’t much in it. All the best!

What works better for you - paying the 1% ERC and using the ‘best’ whole of market lender available to you OR port+additional with Danske, depends on the numbers, what rates are out there, how competitive Danske’s rates are, etc. It might well be that there isn’t much in it. All the best!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

K_S said:@martyziff Quick comments -

- the specifics of porting, switching fixes, ERC in the last few months of a fix, etc. depends on the specific lender- unless I’ve misunderstood, I’ve not heard of lenders that offer to do what you want unconditionally: pay off a fix midway through and waive the ERC if you take another fix, unless all this is linked to a port, or a non-simultaneous port (where ERC is refunded within x months), or within x months of fix end

- some lenders do waive ERC in the last X months of the fix, no idea what Danske bank’s policy is on that

This is one example (Halifax) which illustrates the aboveAnd another (NatWest) which does what you want, in the last 6 months of the fixWhat works better for you - paying the 1% ERC and using the ‘best’ whole of market lender available to you OR port+additional with Danske, depends on the numbers, what rates are out there, how competitive Danske’s rates are, etc. It might well be that there isn’t much in it. All the best!Thanks so much for this.My fixed rate comes to an end in on oct 1st this year so I will be within 3 months by the time of the move so it seems if I was with Halifax, NatWest, Lloyds or Santander I’d be golden but Danske have confirmed that I can’t and I must either pay the ERC or port. I wouldn’t mind porting but it’s just a faff having two loans - Those terms and conditions specifically section 11.11 that I mentioned are in my opinion misleading but there’s not much I can do about it..

Mad that iv to pay a fee to leave a lower rate sooner to go to a higher rate… especially when doing so I may as well look at the market as a whole and as you say potentially take better rate.Thanks for your help!0 -

We went through this before. You can't just say "they won't do what I want so their T&Cs are wrong", even if other lenders might have the option you want.MartyZiff said:

Those terms and conditions specifically section 11.11 that I mentioned are in my opinion misleading but there’s not much I can do about it..0 -

I appreciate that, but it’s more a case that their terms and conditions appear, in my opinion, to describe what the other lenders do.BarelySentientAI said:

We went through this before. You can't just say "they won't do what I want so their T&Cs are wrong", even if other lenders might have the option you want.MartyZiff said:

Those terms and conditions specifically section 11.11 that I mentioned are in my opinion misleading but there’s not much I can do about it..I.e. allow a home mover to avoid an ERC providing the old loan is repaid, a new loan is agreed on a new property and it begins on the day the old loan is repaid. And to be fair the mortgage advisor, and her manager agreed that they read as I understood them and so they escalated it to some back office team who were involved in product design.Unfortunately for me the outcome I got from them tonight was that they don’t offer the same as these other lenders which is obviously up to them and ultimately on me to read the conditions but as I said previously the conditions at 17 seem to to make a distinction between transferring a loan (17.4) and repaying the loan (17.6)

And to be fair the mortgage advisor, and her manager agreed that they read as I understood them and so they escalated it to some back office team who were involved in product design.Unfortunately for me the outcome I got from them tonight was that they don’t offer the same as these other lenders which is obviously up to them and ultimately on me to read the conditions but as I said previously the conditions at 17 seem to to make a distinction between transferring a loan (17.4) and repaying the loan (17.6) When you factor in the wording in the terms, the consultants being unsure when I queried it and that other lenders offer this.. I think it’s reasonable that I seek out some further opinions from people who understand it better than me.Thanks again for your input.1

When you factor in the wording in the terms, the consultants being unsure when I queried it and that other lenders offer this.. I think it’s reasonable that I seek out some further opinions from people who understand it better than me.Thanks again for your input.1 -

Hi,My Halifax mortgage offer states the below:‘Your first monthly payment includes interest from the day we send the loan money to your conveyancer, plus your first monthly mortgage payment. Please look at the 'Amount of each instalment' section of the Mortgage Illustration. It sets out your first payment assuming your mortgage starts on the 1st of the following month. Your first monthly payment may be different as it depends on when your loan starts.’‘We collect your payments by direct debit on 1st of each month.’I’m planning on exchanging on the 25th of this month and then complete a few days later, 27 or 28th of June.

My questions are:Will my first EMI be on 1st of July or 1st of August?Does the bank sent the money to the solicitor on exchange or completion?If I change my completion to the 1st of July, will the first EMI then be set for the 1st of August?Thank you in advance for your assistance.0 -

The bank sends the money when your solicitor asks for it - commonly the day before completion.

Unlikely they'd arrange a direct debit for 1 July if drawdown is only 28 June IMO0 -

-

Just quoting myself to say I resolved the issue with Scottish Power, they've apologised and removed the inaccurate information. HSBC faffed about re the port of my Premier Mortgage, and tried to lower the amount on offer, so I went to a broker who secured a mortgage offer within 48 hours from another lender.sadiedoll said:

Thanks, appreciate the response.K_S said:

@sadiedoll Sorry to hear about this. Scottish Power has form for this issue (incorrectly billing after move), for a few years now, and it beggars belief that they haven't fixed it yet!sadiedoll said:I sold my house recently to move closer to elderly parent, who is unwell. Tried to port my HSBC mortgage, to find out that Scottish Power have registered a default against me for the final bill on the old house (which is paid, and default is showing as settled).

My mortgage is with HSBC, who I know are a really strict lender, but I have significant saving/investments with them and a little while remaining on a low rate mortgage. I've obviously contacted Scottish Power to try and get the default removed, but a) they might refuse and b) time is ticking on my mortgage port, I only have a few months left.

What are my options for other lenders if I can't get this default removed? (Borrowing is a little over 2x salary, earn nearly 50k and have a 65k cash deposit).

- if its a like for like port (no additional borrowing or worse LTV), the lender can sometimes exercise a good amount of discretion to manually override policy/affordability/credit-fails so it is possible that this doesn't scupper your plans. If you've already redeemed the mortgage and are looking to port with a gap, I don't know whether or not this would apply.

- if you are looking at port+additional, then you will need to pass HSBC credit scoring for the port. The default may or may not have an impact, that'll depend on the specifics. HSBC's credit scoring is any more/less strict than other mainstream lenders.

- off of the top of my head, Scottish Power reports to Experian and unfortunately for you HSBC also uses Experian. If that is indeed the case and the HSBC port is a no go, you should have other mainstream options - lenders that use Equifax and don't ask an explicit question about defaults so other than losing the ERC on the port and the remaining time on the low rate fix, you shouldn't be a lot worse off.

Removing the default - I'm sure you have done this already but if not, start with a clear written complaint to Scottish power contactus@scottishpower.com and take it from there.

All the best.

I'd repaid the last mortgage and had six months to port with HSBC, I've got until August 1st...

Scottish Power seem to have registered the default with TransUnion and Equifax as well! I've raised a dispute with the CRAs, a complaint with SP, and via Resolver. Will threaten them with the Ombudsman to see if that forces their hand. Absolutely furious.

If I can't get it shifted reasonably quickly, I'll need to contact a broker and see what they can do - the mortgage advisor I'm dealing with at HSBC claims she can't even get it to underwriting, due to the default coming up when she runs a credit check.

Lesson learned - HSBC are notoriously awful re lending, I was only with them as we have investment accounts held there, but that made not a jot of difference to them. And also, a good mortgage broker is worth a few hundred pounds, he was excellent, reassuring and took care of everything. Thanks to @K_S for advice, it was much appreciated.1 -

Hi,

My husband and I are both first time buyers and need some advice please.

We recently paid off our joint IVA with a full and final offer in May 2024. This drops off our credit file in September.

I am in the process of settling an employment tribunal claim with my employer out of court. This will be our deposit. As part of the agreement, I'll be leaving my employment of over 10yrs. I am currently job searching.

My husband is looking for work too after being off work since made redundant in 2020. He had some health issues which are now resolved and we needed childcare. He also upskilled in that time period and did some contract and volunteer work I his field to keep skill current.

My questions is how much of a risk will a lender see us as due to the way we got our deposit, our new empty and poor credit file. I am guessing we need to disclose where the deposit came from?

And also how bad is it that my husband not having work since 2020.

We are both looking for work before applying for a mortgage and will continue working.

We rent privately and our rent just went up by 50%. It is now in line with similar size rental houses.

The increase in rent is eating into our ability to save. We are finding out as much info as we can to see what our options are, regarding getting a mortgage.

Thank you for your time

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards