Current debt-free wannabe stats:

We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Mortgage broker - ask me anything

Comments

-

Hiya

I have been trying to find information on this to no avail - really appreciate your thoughts!

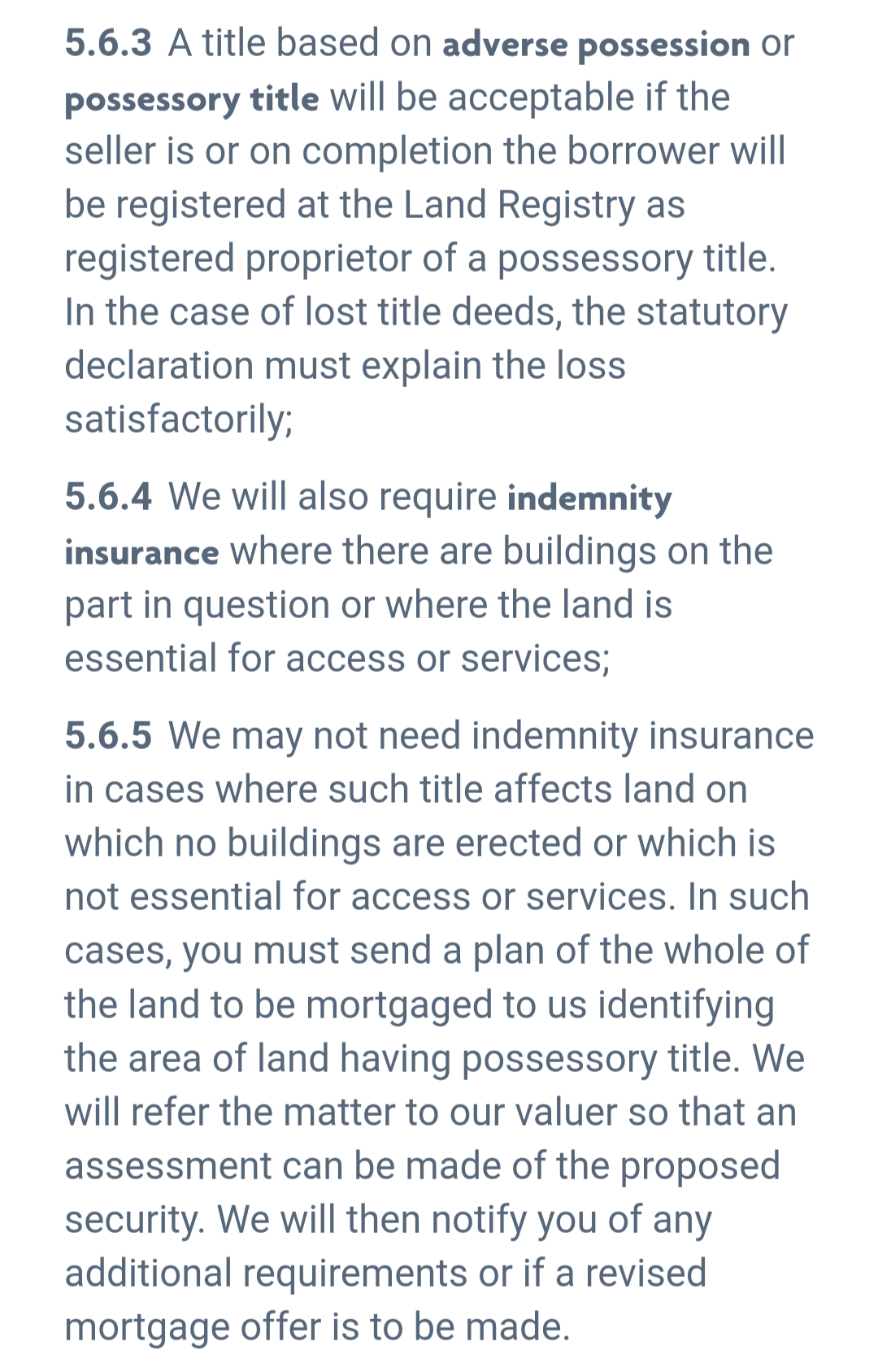

I have just found out that about half of the garden of the house I'm buying is not owned by anyone (not in any Title), but it meets the conditions for adverse possession. The seller is applying for Possessory Title and indemnity insurance for the sale.

I already received a mortgage offer from Santander for the house, prior to discovering this. I have read the condition below and am worried this will mean they won't give me the mortgage now, because the house and some of the garden is Freehold, but the other half of the garden is Possessory Title.

What do you think?

Credit card: £8,524.31 | Loan: £3,224.80 | Student Loan (Plan 1): £5,768.55 | Total: £17,517.66Debt-free target: 21-Mar-2027

Debt-free diary0 -

@annetheman I've no idea tbh as this kind of stuff usually only comes up at conveyancing and is dealt with between the conveyancer and lender.annetheman said:Hiya

I have been trying to find information on this to no avail - really appreciate your thoughts!

I have just found out that about half of the garden of the house I'm buying is not owned by anyone (not in any Title), but it meets the conditions for adverse possession. The seller is applying for Possessory Title and indemnity insurance for the sale.

I already received a mortgage offer from Santander for the house, prior to discovering this. I have read the condition below and am worried this will mean they won't give me the mortgage now, because the house and some of the garden is Freehold, but the other half of the garden is Possessory Title.

What do you think?

As per the CML handbook for Santander, these appear to the requirements that Santander asks of the conveyancer with regard to possessory title.

https://lendershandbook.ukfinance.org.uk/

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi,

is there any benefit to going back to the broker who managed m current mortgage (Barclays) when I’m looking to move, port the mortgage and take on additional borrowing?

I’m leaning towards going to Barclays direct

thanks0 -

Thanks, appreciate the response.K_S said:

@sadiedoll Sorry to hear about this. Scottish Power has form for this issue (incorrectly billing after move), for a few years now, and it beggars belief that they haven't fixed it yet!sadiedoll said:I sold my house recently to move closer to elderly parent, who is unwell. Tried to port my HSBC mortgage, to find out that Scottish Power have registered a default against me for the final bill on the old house (which is paid, and default is showing as settled).

My mortgage is with HSBC, who I know are a really strict lender, but I have significant saving/investments with them and a little while remaining on a low rate mortgage. I've obviously contacted Scottish Power to try and get the default removed, but a) they might refuse and b) time is ticking on my mortgage port, I only have a few months left.

What are my options for other lenders if I can't get this default removed? (Borrowing is a little over 2x salary, earn nearly 50k and have a 65k cash deposit).

- if its a like for like port (no additional borrowing or worse LTV), the lender can sometimes exercise a good amount of discretion to manually override policy/affordability/credit-fails so it is possible that this doesn't scupper your plans. If you've already redeemed the mortgage and are looking to port with a gap, I don't know whether or not this would apply.

- if you are looking at port+additional, then you will need to pass HSBC credit scoring for the port. The default may or may not have an impact, that'll depend on the specifics. HSBC's credit scoring is any more/less strict than other mainstream lenders.

- off of the top of my head, Scottish Power reports to Experian and unfortunately for you HSBC also uses Experian. If that is indeed the case and the HSBC port is a no go, you should have other mainstream options - lenders that use Equifax and don't ask an explicit question about defaults so other than losing the ERC on the port and the remaining time on the low rate fix, you shouldn't be a lot worse off.

Removing the default - I'm sure you have done this already but if not, start with a clear written complaint to Scottish power contactus@scottishpower.com and take it from there.

All the best.

I'd repaid the last mortgage and had six months to port with HSBC, I've got until August 1st...

Scottish Power seem to have registered the default with TransUnion and Equifax as well! I've raised a dispute with the CRAs, a complaint with SP, and via Resolver. Will threaten them with the Ombudsman to see if that forces their hand. Absolutely furious.

If I can't get it shifted reasonably quickly, I'll need to contact a broker and see what they can do - the mortgage advisor I'm dealing with at HSBC claims she can't even get it to underwriting, due to the default coming up when she runs a credit check.0 -

@sadiedoll If the default is showing on both Equifax and Experian, then it’s definitely going to limit your non-HSBC options. Even so, as a utility default, if that’s the one and only blemish, you should still be able to get a mainstream/ish with an alternate lender or product line like Accord cascade, the Leeds’ equivalent, etc. or a lender that doesn’t credit score.sadiedoll said:

Thanks, appreciate the response.K_S said:

@sadiedoll Sorry to hear about this. Scottish Power has form for this issue (incorrectly billing after move), for a few years now, and it beggars belief that they haven't fixed it yet!sadiedoll said:I sold my house recently to move closer to elderly parent, who is unwell. Tried to port my HSBC mortgage, to find out that Scottish Power have registered a default against me for the final bill on the old house (which is paid, and default is showing as settled).

My mortgage is with HSBC, who I know are a really strict lender, but I have significant saving/investments with them and a little while remaining on a low rate mortgage. I've obviously contacted Scottish Power to try and get the default removed, but a) they might refuse and b) time is ticking on my mortgage port, I only have a few months left.

What are my options for other lenders if I can't get this default removed? (Borrowing is a little over 2x salary, earn nearly 50k and have a 65k cash deposit).

- if its a like for like port (no additional borrowing or worse LTV), the lender can sometimes exercise a good amount of discretion to manually override policy/affordability/credit-fails so it is possible that this doesn't scupper your plans. If you've already redeemed the mortgage and are looking to port with a gap, I don't know whether or not this would apply.

- if you are looking at port+additional, then you will need to pass HSBC credit scoring for the port. The default may or may not have an impact, that'll depend on the specifics. HSBC's credit scoring is any more/less strict than other mainstream lenders.

- off of the top of my head, Scottish Power reports to Experian and unfortunately for you HSBC also uses Experian. If that is indeed the case and the HSBC port is a no go, you should have other mainstream options - lenders that use Equifax and don't ask an explicit question about defaults so other than losing the ERC on the port and the remaining time on the low rate fix, you shouldn't be a lot worse off.

Removing the default - I'm sure you have done this already but if not, start with a clear written complaint to Scottish power contactus@scottishpower.com and take it from there.

All the best.

I'd repaid the last mortgage and had six months to port with HSBC, I've got until August 1st...

Scottish Power seem to have registered the default with TransUnion and Equifax as well! I've raised a dispute with the CRAs, a complaint with SP, and via Resolver. Will threaten them with the Ombudsman to see if that forces their hand. Absolutely furious.

If I can't get it shifted reasonably quickly, I'll need to contact a broker and see what they can do - the mortgage advisor I'm dealing with at HSBC claims she can't even get it to underwriting, due to the default coming up when she runs a credit check.

A broker is unlikely to be able to help with overriding the HSBC credit-score fail, but might be able to place you with an alternate option above depending on the specifics. If/when you do speak to a broker, make sure you get your Experian+Equifax or Checkmyfile report prior to that so they can see exactly what is on it.

All the best!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Thanks for the advice - SP have emailed to say they will remove the default, already gone from Equifax and TransUnion. Have provided the evidence to HSBC, so fingers crossed!K_S said:

@sadiedoll If the default is showing on both Equifax and Experian, then it’s definitely going to limit your non-HSBC options. Even so, as a utility default, if that’s the one and only blemish, you should still be able to get a mainstream/ish with an alternate lender or product line like Accord cascade, the Leeds’ equivalent, etc. or a lender that doesn’t credit score.sadiedoll said:

Thanks, appreciate the response.K_S said:

@sadiedoll Sorry to hear about this. Scottish Power has form for this issue (incorrectly billing after move), for a few years now, and it beggars belief that they haven't fixed it yet!sadiedoll said:I sold my house recently to move closer to elderly parent, who is unwell. Tried to port my HSBC mortgage, to find out that Scottish Power have registered a default against me for the final bill on the old house (which is paid, and default is showing as settled).

My mortgage is with HSBC, who I know are a really strict lender, but I have significant saving/investments with them and a little while remaining on a low rate mortgage. I've obviously contacted Scottish Power to try and get the default removed, but a) they might refuse and b) time is ticking on my mortgage port, I only have a few months left.

What are my options for other lenders if I can't get this default removed? (Borrowing is a little over 2x salary, earn nearly 50k and have a 65k cash deposit).

- if its a like for like port (no additional borrowing or worse LTV), the lender can sometimes exercise a good amount of discretion to manually override policy/affordability/credit-fails so it is possible that this doesn't scupper your plans. If you've already redeemed the mortgage and are looking to port with a gap, I don't know whether or not this would apply.

- if you are looking at port+additional, then you will need to pass HSBC credit scoring for the port. The default may or may not have an impact, that'll depend on the specifics. HSBC's credit scoring is any more/less strict than other mainstream lenders.

- off of the top of my head, Scottish Power reports to Experian and unfortunately for you HSBC also uses Experian. If that is indeed the case and the HSBC port is a no go, you should have other mainstream options - lenders that use Equifax and don't ask an explicit question about defaults so other than losing the ERC on the port and the remaining time on the low rate fix, you shouldn't be a lot worse off.

Removing the default - I'm sure you have done this already but if not, start with a clear written complaint to Scottish power contactus@scottishpower.com and take it from there.

All the best.

I'd repaid the last mortgage and had six months to port with HSBC, I've got until August 1st...

Scottish Power seem to have registered the default with TransUnion and Equifax as well! I've raised a dispute with the CRAs, a complaint with SP, and via Resolver. Will threaten them with the Ombudsman to see if that forces their hand. Absolutely furious.

If I can't get it shifted reasonably quickly, I'll need to contact a broker and see what they can do - the mortgage advisor I'm dealing with at HSBC claims she can't even get it to underwriting, due to the default coming up when she runs a credit check.

A broker is unlikely to be able to help with overriding the HSBC credit-score fail, but might be able to place you with an alternate option above depending on the specifics. If/when you do speak to a broker, make sure you get your Experian+Equifax or Checkmyfile report prior to that so they can see exactly what is on it.

All the best!

Spoke to NatWest (current account provider) and a broker yesterday, both said the mortgage was do-able even if HSBC won't play ball, which means I only lose the last 6 months of my cheap rate and the ERC - which isn't a massive deal in the greater scheme of things.0 -

@sadiedoll Glad to hear things are moving in the right direction! NatWest only checks Equifax so you should be ok on that front now that your Equifax report is clear of any defaults.sadiedoll said:

Thanks for the advice - SP have emailed to say they will remove the default, already gone from Equifax and TransUnion. Have provided the evidence to HSBC, so fingers crossed!K_S said:

@sadiedoll If the default is showing on both Equifax and Experian, then it’s definitely going to limit your non-HSBC options. Even so, as a utility default, if that’s the one and only blemish, you should still be able to get a mainstream/ish with an alternate lender or product line like Accord cascade, the Leeds’ equivalent, etc. or a lender that doesn’t credit score.sadiedoll said:

Thanks, appreciate the response.K_S said:

@sadiedoll Sorry to hear about this. Scottish Power has form for this issue (incorrectly billing after move), for a few years now, and it beggars belief that they haven't fixed it yet!sadiedoll said:I sold my house recently to move closer to elderly parent, who is unwell. Tried to port my HSBC mortgage, to find out that Scottish Power have registered a default against me for the final bill on the old house (which is paid, and default is showing as settled).

My mortgage is with HSBC, who I know are a really strict lender, but I have significant saving/investments with them and a little while remaining on a low rate mortgage. I've obviously contacted Scottish Power to try and get the default removed, but a) they might refuse and b) time is ticking on my mortgage port, I only have a few months left.

What are my options for other lenders if I can't get this default removed? (Borrowing is a little over 2x salary, earn nearly 50k and have a 65k cash deposit).

- if its a like for like port (no additional borrowing or worse LTV), the lender can sometimes exercise a good amount of discretion to manually override policy/affordability/credit-fails so it is possible that this doesn't scupper your plans. If you've already redeemed the mortgage and are looking to port with a gap, I don't know whether or not this would apply.

- if you are looking at port+additional, then you will need to pass HSBC credit scoring for the port. The default may or may not have an impact, that'll depend on the specifics. HSBC's credit scoring is any more/less strict than other mainstream lenders.

- off of the top of my head, Scottish Power reports to Experian and unfortunately for you HSBC also uses Experian. If that is indeed the case and the HSBC port is a no go, you should have other mainstream options - lenders that use Equifax and don't ask an explicit question about defaults so other than losing the ERC on the port and the remaining time on the low rate fix, you shouldn't be a lot worse off.

Removing the default - I'm sure you have done this already but if not, start with a clear written complaint to Scottish power contactus@scottishpower.com and take it from there.

All the best.

I'd repaid the last mortgage and had six months to port with HSBC, I've got until August 1st...

Scottish Power seem to have registered the default with TransUnion and Equifax as well! I've raised a dispute with the CRAs, a complaint with SP, and via Resolver. Will threaten them with the Ombudsman to see if that forces their hand. Absolutely furious.

If I can't get it shifted reasonably quickly, I'll need to contact a broker and see what they can do - the mortgage advisor I'm dealing with at HSBC claims she can't even get it to underwriting, due to the default coming up when she runs a credit check.

A broker is unlikely to be able to help with overriding the HSBC credit-score fail, but might be able to place you with an alternate option above depending on the specifics. If/when you do speak to a broker, make sure you get your Experian+Equifax or Checkmyfile report prior to that so they can see exactly what is on it.

All the best!

Spoke to NatWest (current account provider) and a broker yesterday, both said the mortgage was do-able even if HSBC won't play ball, which means I only lose the last 6 months of my cheap rate and the ERC - which isn't a massive deal in the greater scheme of things.All the best.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

As we are less than 6 months away from my current mortgage deal with Halifax expiring, I've applied and had a mortgage application accepted by NatWest. The mortgage offer has been sent to the bank's solicitors and they've sent me through loads of stuff too.Our mortgage expires on 30 September 2024 so I'm hoping we can get a better rate before this (whether NatWest or elsewhere - although most likely will stick with NatWest). Do I need to / should I still complete all the paperwork now with NatWest's solicitors now? Just seems mad to complete everything 4 months in advance when I may want to change the product/bank later.0

-

Hello, does anyone have any idea which lenders accept gifts from someone that will be living in the property? My mother will be moving in with us as I am her full time carer. she is gifting some money from the sale of her house so we can buy a more suitable property for her needs. All the lenders we have tried will not accept the gift even with a letter saying it is not repayable. Thanks x0

-

@littlemissam There definitely are a handful of lenders that will consider gift from someone that will reside at the property but won’t be on the deeds. So if that is the only thing stopping you, don’t give up yet.littlemissam said:Hello, does anyone have any idea which lenders accept gifts from someone that will be living in the property? My mother will be moving in with us as I am her full time carer. she is gifting some money from the sale of her house so we can buy a more suitable property for her needs. All the lenders we have tried will not accept the gift even with a letter saying it is not repayable. Thanks x

If you’ve used a broker and they haven’t been able to place it then it might be a no go for a combination of reasons. If you haven’t used a broker I would suggest speaking to one, the MSE guide here can help you find one, including plenty of fee-free ones.

https://www.moneysavingexpert.com/mortgages/best-mortgages-cashback/#step3All the best.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards