We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

@annetheman As far as the lender is concerned, whether it’s at 0% or 30% doesn’t matter to them, they’ve already factored the balance in at a certain monthly cost assumption (3-5% of outstanding balance).annetheman said:Hi (this is the most helpful thread on the MSE, for sure!)

I have a Santander mortgage offer which expires in September 2024. I am still waiting for my buyer to be approved by housing association, so I don't expect to complete until about August or worst case scenario September.

I applied with my current credit balances and it is not a condition to clear the balance before completion.

I have a Barclaycard with 0% interest on the balance of £4,700 until July 2025 - currently about £8,000 remaining credit.

I also have a NatWest CC with 0% interest on the balance of £7,000 until July 2024 - currently only £600 remaining credit.

I want to move the NatWest balance to the Barclaycard, so that I don't start incurring interest at APR from July 2024.

To avoid 2 months of high interest before completion, can I move the balance to the other card? Or best not to make any changes at all and just swallow the high APR until the mortgage is drawn down? My outgoing payments will be higher because although the Barclays balance is 0% and I have less owed on it, it has a much higher monthly payment than Natwest.

Thanks for your advice!!

If you already have an offer and don’t expect to drawdown funds for a good few months, transferring the balance between the cards while keeping the total balance no higher than what’s declared on the application *should not* cause issues.

The issues that can arise with this scenario is due to delays in credit bureaus updating the balances, so often for a few weeks after the BT you could have cc1 show the old balance while cc2 shows the new balance, thus overstating the balance. If you then request drawdown of funds, that can sometimes trigger a refresh of the credit data thus causing issues with affordability or a credit-score (lender scoring, nothing to do with the Experian score) fail.

But if you have a good few months between the BT and expected drawdown, I wouldn’t expect the above to come into play.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Can someone please help me, I feel like I'm losing my mind!

I have been answering questions and providing documents for the underwriter at Santander for weeks now. The last question came on Monday, they wanted official confirmation of how me returning to work shortly will affect my benefits. I used the entitled to website to get a pdf calculation but they wanted each benefit office to provide the confirmation, I knew this wouldn't be a thing they would do but I called UC and council tax support, only to find out they really won't provide this. The change needs to happen then I will get the new award. Only trouble is with council tax it could take six weeks to receive an amended award. I don't have six weeks unfortunately, my ma has gone back to them to say I am unable to get a pre change confirmation and I'm awaiting another reply.

This was the final thing before going to offer, it's been ongoing since 1/03 and I am just so so gutted I'm going to fail at the final hurdle!

Do underwriters ever accept that sometimes people cannot physically get what they are asking for?

I'm buying a new build and completion is due may/June so I don't have long at all to get a mortgage and get all the legals done!

Tomorrow my ma is putting in an application with Barclays, is this my better option?0 -

@mumsta77 Sorry this is one of those non-standard cases where it’s hard to give any useful info as the devil is in the details that your broker is best familiar with.mumsta77 said:Can someone please help me, I feel like I'm losing my mind!

I have been answering questions and providing documents for the underwriter at Santander for weeks now. The last question came on Monday, they wanted official confirmation of how me returning to work shortly will affect my benefits. I used the entitled to website to get a pdf calculation but they wanted each benefit office to provide the confirmation, I knew this wouldn't be a thing they would do but I called UC and council tax support, only to find out they really won't provide this. The change needs to happen then I will get the new award. Only trouble is with council tax it could take six weeks to receive an amended award. I don't have six weeks unfortunately, my ma has gone back to them to say I am unable to get a pre change confirmation and I'm awaiting another reply.

This was the final thing before going to offer, it's been ongoing since 1/03 and I am just so so gutted I'm going to fail at the final hurdle!

Do underwriters ever accept that sometimes people cannot physically get what they are asking for?

I'm buying a new build and completion is due may/June so I don't have long at all to get a mortgage and get all the legals done!

Tomorrow my ma is putting in an application with Barclays, is this my better option?

With regard to documents, your broker needs to speak to Santander to understand if they will accept any alternate documents to evidence benefits post return to work, or if there are any other permutations or combinations that will work.

Hopefully they have spoken to Barclays, run your case past them in detail and understood their evidence requirements properly before submitting the case. And not just gone with the next cheapest lender in the list and hope it works out.

All the best, I hope you get to offer soon!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Thank you, I have put forward a couple of points today which should help affordability but I guess it's how set they are on seeing official proof of impact of earnings... It's literally £25 a week or so difference according to entitled to website.K_S said:

@mumsta77 Sorry this is one of those non-standard cases where it’s hard to give any useful info as the devil is in the details that your broker is best familiar with.mumsta77 said:Can someone please help me, I feel like I'm losing my mind!

I have been answering questions and providing documents for the underwriter at Santander for weeks now. The last question came on Monday, they wanted official confirmation of how me returning to work shortly will affect my benefits. I used the entitled to website to get a pdf calculation but they wanted each benefit office to provide the confirmation, I knew this wouldn't be a thing they would do but I called UC and council tax support, only to find out they really won't provide this. The change needs to happen then I will get the new award. Only trouble is with council tax it could take six weeks to receive an amended award. I don't have six weeks unfortunately, my ma has gone back to them to say I am unable to get a pre change confirmation and I'm awaiting another reply.

This was the final thing before going to offer, it's been ongoing since 1/03 and I am just so so gutted I'm going to fail at the final hurdle!

Do underwriters ever accept that sometimes people cannot physically get what they are asking for?

I'm buying a new build and completion is due may/June so I don't have long at all to get a mortgage and get all the legals done!

Tomorrow my ma is putting in an application with Barclays, is this my better option?

With regard to documents, your broker needs to speak to Santander to understand if they will accept any alternate documents to evidence benefits post return to work, or if there are any other permutations or combinations that will work.

Hopefully they have spoken to Barclays, run your case past them in detail and understood their evidence requirements properly before submitting the case. And not just gone with the next cheapest lender in the list and hope it works out.

All the best, I hope you get to offer soon!

He said he was going through Barclays criteria with a fine tooth comb yesterday but I don't think he's spoken to them about my circumstances.

I just want the yes from Santander to save me the redemption and let me keep the cheap rate I'm currently on, seems so unfair!

Thanks for your advice x0 -

We are about to remortgage, and stuck between a fix or a tracker.

The fixed rate is 4.57% @£2888pm and the tracker is 5.40% (tracking 0.15% above base) @£3208pm. With the fix, a new fixed rate/product switch can be applied at 18 months. We were hoping that rate cuts would be firmly on the cards right above now.

Additionally, am I right in thinking the fixed period starts from application? I.E. if we apply this week then, we can apply for a product switch in 18months time from this week or is it from completion?

0 -

@Maka344Maka344 said:We are about to remortgage, and stuck between a fix or a tracker.

The fixed rate is 4.57% @£2888pm and the tracker is 5.40% (tracking 0.15% above base) @£3208pm. With the fix, a new fixed rate/product switch can be applied at 18 months. We were hoping that rate cuts would be firmly on the cards right above now.

Additionally, am I right in thinking the fixed period starts from application? I.E. if we apply this week then, we can apply for a product switch in 18months time from this week or is it from completion?

End date of a “2 year” fix - depends on the lender. Generally speaking it will be one of following - exactly 24 months from the 1st of the month following completion (eg: Nationwide) or the fix will end at a certain date specific to that product that may mean you get a fix that is a few months less/more than 2 years (eg: Halifax).

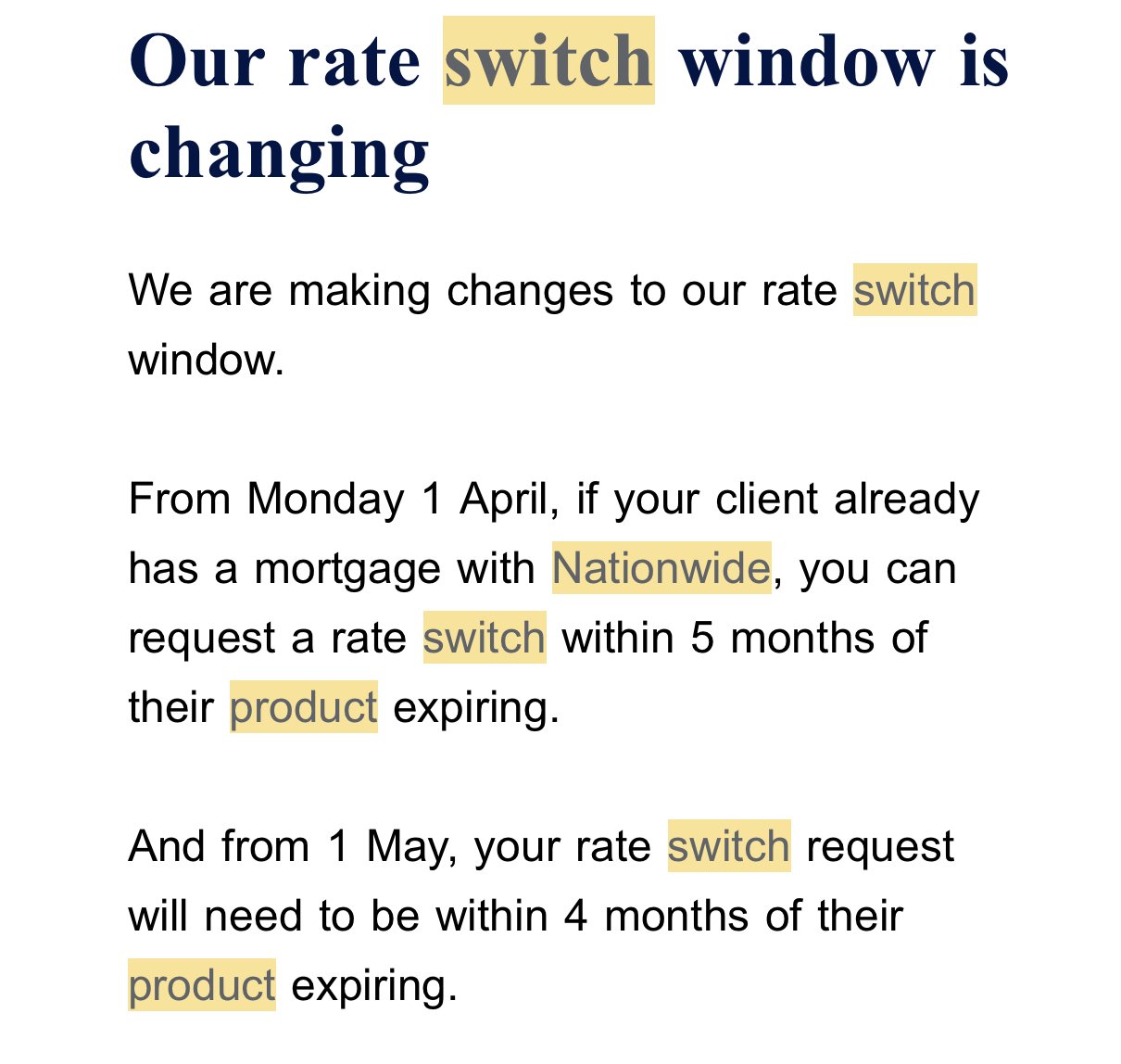

How early you can secure a product switch will again depend on the lender and their policy at that point of time in the future. Most lenders will fall within the 4-6 month (from the end of the fix) category. Do keep in mind that this can change. For example see the Nationwide change below

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Thank you for taking the time to reply. This is helpful, we are looking at Barclays. Interesting how the rate switch windows can change.K_S said:

@Maka344Maka344 said:We are about to remortgage, and stuck between a fix or a tracker.

The fixed rate is 4.57% @£2888pm and the tracker is 5.40% (tracking 0.15% above base) @£3208pm. With the fix, a new fixed rate/product switch can be applied at 18 months. We were hoping that rate cuts would be firmly on the cards right above now.

Additionally, am I right in thinking the fixed period starts from application? I.E. if we apply this week then, we can apply for a product switch in 18months time from this week or is it from completion?

End date of a “2 year” fix - depends on the lender. Generally speaking it will be one of following - exactly 24 months from the 1st of the month following completion (eg: Nationwide) or the fix will end at a certain date specific to that product that may mean you get a fix that is a few months less/more than 2 years (eg: Halifax).

How early you can secure a product switch will again depend on the lender and their policy at that point of time in the future. Most lenders will fall within the 4-6 month (from the end of the fix) category. Do keep in mind that this can change. For example see the Nationwide change below0 -

Hi! Firstly I have severe anxiety so I’m an absolute worry head so I just wanted to ask for some clarification, so I’m sorry if this is something obvious/silly. I frequently overthink the smallest things into the biggest things 😅Me and my OH current mortgage deal ends Jan 2026 (so a while away) but I am looking to put the 20% HTB loan in with the remortgage.House worth: £180,000

Current Mortgage: £93000

Help to buy: £36000

So we are looking at a total to remortgage at £129000ish

We earn £56k between us

And have excellent credit scores on Experian that’s squeaky clean bar one missed payment 2 years ago that was paid straight away and was due to the DD not being set up correctly

my concern is our DTI - by the time we come round to remortgage next June/July our DTI is sitting at 35% (with a new mortgage rate included at £700)

We will have 3 loans and no CC, however one loan is under my dad and I just pay him back monthly so not directly connected to me but I’ve added this to the DTI (which I think is right?)

Will a 35% DTI affect us getting a higher mortgage to get rid of the HTB? And if yes would it be potentially worth doing a 2 year fixed rate and paying the HTB interest instead at the risk of house prices rising, as by this point all the loans would be paid?Thank you in advance!0 -

@mellowmay The vast majority of lenders don’t care about DTI as a discrete measure and for the handful that do (mostly small building societies) it’s based only on unsecured debt and afaik not calculated in the way you’ve described. I wouldn’t worry about DTI. With debt what matters is the outstanding balance for cc debt and the minimum monthly payment for non cc debt.

Just play around with your actual numbers on a couple of lender affordability calculators, and they should tell you if the background debt is an issue that may stop you from borrowing 130k at 75% LTV with a 56k income on the maximum term the lender allows for you. I suspect it won’t be an issue.

https://www.halifax-intermediaries.co.uk/tools-calculators/mortgage-affordability-calculator.htmlhttps://online.accordmortgages.com/public/mortgages/quick_enquiry.doMellowMay said:Hi! Firstly I have severe anxiety so I’m an absolute worry head so I just wanted to ask for some clarification, so I’m sorry if this is something obvious/silly. I frequently overthink the smallest things into the biggest things 😅Me and my OH current mortgage deal ends Jan 2026 (so a while away) but I am looking to put the 20% HTB loan in with the remortgage.House worth: £180,000

Current Mortgage: £93000

Help to buy: £36000

So we are looking at a total to remortgage at £129000ish

We earn £56k between us

And have excellent credit scores on Experian that’s squeaky clean bar one missed payment 2 years ago that was paid straight away and was due to the DD not being set up correctly

my concern is our DTI - by the time we come round to remortgage next June/July our DTI is sitting at 35% (with a new mortgage rate included at £700)

We will have 3 loans and no CC, however one loan is under my dad and I just pay him back monthly so not directly connected to me but I’ve added this to the DTI (which I think is right?)

Will a 35% DTI affect us getting a higher mortgage to get rid of the HTB? And if yes would it be potentially worth doing a 2 year fixed rate and paying the HTB interest instead at the risk of house prices rising, as by this point all the loans would be paid?Thank you in advance!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

If my mortgage is 6.9% and the early redemption penalty is 4% am I saving 2.9% by overpaying or have I got this wrong?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards