We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

@[Deleted User] Someone looking to do this would typically use a bridging loan to buy the property, fix it up and then remortgage it to a standard mortgage (resi or BTL depending on what they intend to do with it) or sell it for a profit to pay off the bridging loan.[Deleted User] said:

Thanks. How would you buy it if you have to fix it up first to get a mortgage?K_S said:

@[Deleted User][Deleted User] said:I see a lot of wrecked houses on the market in need of complete renovation. Say £50k or more. Is there any way to mortgage that?

Or how about self builds?

Would need to borrow about 300-350k on a 63k income.

Wrecked houses requiring complete renovation - you'd have to get something like a bridging loan, make it habitable and then re-mortgage to a BTL or residential mortgage depending on what you intend to do with it.

Self-build - you'll need a self-build mortgage which will usually allow you to buy land and fund the build cost

I guess it depends what they consider habitable. I wouldn't live there, but you could.

Seems impossible anyway. A huge loan and a huge mortgage.

A bridging loan would usually be up to 60-70% LTV, so you'd either need a cash deposit or sufficient equity in another property that you own to bring the total LTV down to the required level.

It's not uncommon tbh, but usually people doing it are experienced investors/landlords looking to rent it out or sell it.

People going down this route to buy to live in is much rarer, not least because the intention to live in it makes the bridging loan a regulated product which reduces the options available and makes it harder to tick the required boxes.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Just a question on affordability criteria for mortgage applications.

We have applied for a home mover mortgage as we are looking to upsize. We are looking for a £280k mortgage (£75k increase to existing £205k) on a £380k property so just under 75% LTV. Our annual income is approx £72k, mine is £36k employed part time and my husbands average self employed profit for the last two years is £34k I also get an annual bonus of around £2k. Two dependents but no childcare costs and no debt, plus £10k in savings. We have extended term to retirement age on advice of mortgage advisor so adding on another 8 years. Yet still referring on affordability. What else could be affecting our affordability? The mortgage payments will actually be less than we have recently been paying on the existing mortgage and a loan that we have just paid off.The MA was including my regular payments for a work share saving scheme as a commitment but i thought this would not be included as these can be stopped at any time, and I have the purchased shares which I can also cash in. Could this be what is affecting the application?0 -

@s3323Ned I assume you're porting with your current lender, using the bank's internal mortgage adviser, and adding additional borrowing totalling up to 280k at 75% LTV. That being the case, with most lenders, generally speaking you will be expected to meet their affordability calculations (will differ across lenders) to borrow the required amount of 280k.S3323Ned said:Just a question on affordability criteria for mortgage applications.

We have applied for a home mover mortgage as we are looking to upsize. We are looking for a £280k mortgage (£75k increase to existing £205k) on a £380k property so just under 75% LTV. Our annual income is approx £72k, mine is £36k employed part time and my husbands average self employed profit for the last two years is £34k I also get an annual bonus of around £2k. Two dependents but no childcare costs and no debt, plus £10k in savings. We have extended term to retirement age on advice of mortgage advisor so adding on another 8 years. Yet still referring on affordability. What else could be affecting our affordability? The mortgage payments will actually be less than we have recently been paying on the existing mortgage and a loan that we have just paid off.The MA was including my regular payments for a work share saving scheme as a commitment but i thought this would not be included as these can be stopped at any time, and I have the purchased shares which I can also cash in. Could this be what is affecting the application?

You can get a very rough idea of the numbers by googling the lender's detailed affordability calc and plugging in the numbers. For example if Nationwide then google "nationwide for intermediaries affordability calculator".

Sharesave payments - lenders treat payslip deductions in different ways, some might ignore share-save deductions, some might only ignore pension deductions, some might not even ignore pension deductions, etc. If you current lender's policy is to treat sharesave deductions as a committed outgoing, then it could well impact affordability.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

New Query on Remortgage 'Right to Buy' please?

We purchased our home through the right to buy scheme in March 2022, on a 2yr fixed deal, with Kensington.

Part of the right to buy process includes a 5yr pre-emption period, allowing the council to reclaim a reduced amount year on year of the original discount, if we ever sold on. Works out we approximately 'gain back/keep' 20% a year of the original discount over the 5 years.

How does this work when looking to remortgage, can any of that 40% be used when remortgaging? Are there any difficulties remortgaging a right to buy with this pre-emption, different to when i was first mortgaging it? Do i still need a 'right to buy' mortgage product, or a standard one this time round?

Also, could I with a solicitors help, buy myself out of the pre-emption period, has anyone done this or worked with this? I am not looking to sell, but would like to do some urgent renovations.

Thanks so much - Lisa 0

0 -

Thanks. Just clutching at straws but it looks like it's not going to work.K_S said:

@[Deleted User] Someone looking to do this would typically use a bridging loan to buy the property, fix it up and then remortgage it to a standard mortgage (resi or BTL depending on what they intend to do with it) or sell it for a profit to pay off the bridging loan.[Deleted User] said:

Thanks. How would you buy it if you have to fix it up first to get a mortgage?K_S said:

@[Deleted User][Deleted User] said:I see a lot of wrecked houses on the market in need of complete renovation. Say £50k or more. Is there any way to mortgage that?

Or how about self builds?

Would need to borrow about 300-350k on a 63k income.

Wrecked houses requiring complete renovation - you'd have to get something like a bridging loan, make it habitable and then re-mortgage to a BTL or residential mortgage depending on what you intend to do with it.

Self-build - you'll need a self-build mortgage which will usually allow you to buy land and fund the build cost

I guess it depends what they consider habitable. I wouldn't live there, but you could.

Seems impossible anyway. A huge loan and a huge mortgage.

A bridging loan would usually be up to 60-70% LTV, so you'd either need a cash deposit or sufficient equity in another property that you own to bring the total LTV down to the required level.

It's not uncommon tbh, but usually people doing it are experienced investors/landlords looking to rent it out or sell it.

People going down this route to buy to live in is much rarer, not least because the intention to live in it makes the bridging loan a regulated product which reduces the options available and makes it harder to tick the required boxes.0 -

Morning, my daughter is now in a position to buy. 20K deposit recently qualified as a nurse, so band 5 wage. She's done a mortgage in principle online. Looked at 3 houses, really liked one that is in her budget . The estate agent is pushing her to use their independent broker. She banks with nationwide and has a LISA with Nottingham BS.

What should she do next? Who would be the better mortgage advisor/supplier?

Thanks for any advice0 -

A question about understanding the 'balance' used for overpayments please.

We are looking at a 2yr fixed deal with Natwest which allows overpayment of 20% of the balance per year. We are looking to increase our monthly payments (to the maximum amount allowed) to reduce the term of the mortgage overall. My question is around the balance used to calculate the 20%. Is it:

1) 20% of the outstanding balance at the start of the year, or

2) 20% of the balance as at the previous month (given that the overpayments will be month on month), or

3) something else entirely that I haven't thought of!

The difference between points 1 & 2 above can mean several months of the mortgage term (as in point 1 will pay the mortgage off much quicker than point 2).

Thanks for your help!

1p a day challenge #47 £1.89/£671.61

SPC #025 2020 £947.360 -

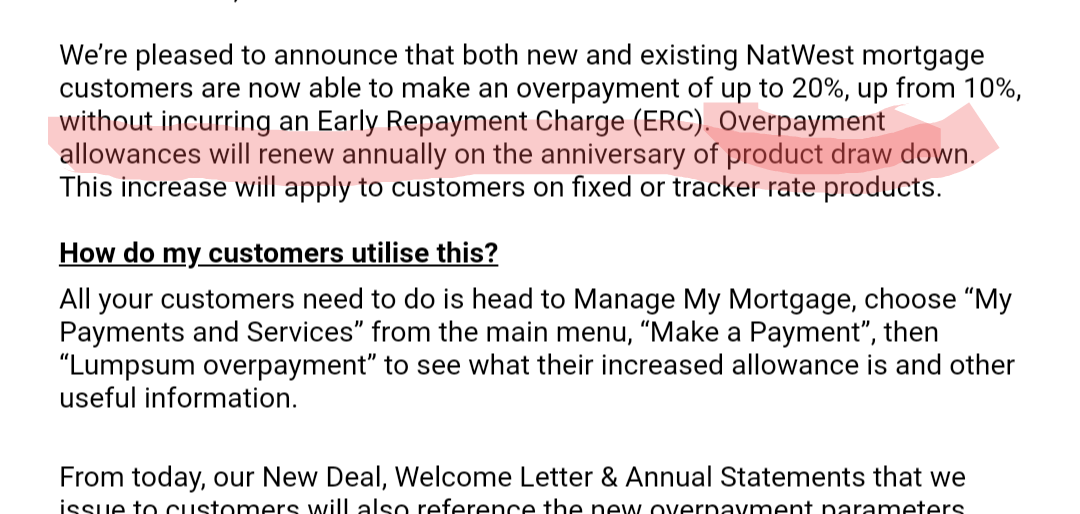

@mrsme As per the comms they sent out, the o/p allowance resets on the mortgage anniversary so I would expect that to be the amount that 20% is based on. I don't know of any lenders who do it as given in point 2.MrsMe said:A question about understanding the 'balance' used for overpayments please.

We are looking at a 2yr fixed deal with Natwest which allows overpayment of 20% of the balance per year. We are looking to increase our monthly payments (to the maximum amount allowed) to reduce the term of the mortgage overall. My question is around the balance used to calculate the 20%. Is it:

1) 20% of the outstanding balance at the start of the year, or

2) 20% of the balance as at the previous month (given that the overpayments will be month on month), or

3) something else entirely that I haven't thought of!

The difference between points 1 & 2 above can mean several months of the mortgage term (as in point 1 will pay the mortgage off much quicker than point 2).

Thanks for your help!

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Good evening all,

I'm trying to find out some information on TML (The Mortgage Lender) as we have just submitted an application with them via our Broker.

We have previously been declined by Aldermore for the same loan amount and broker's advised up to try TML.

Can any of the MA's on here (or anyone with experience of using them) provide some insight as to their process and turnaround?

We've paid the £815 valuation and application fee and confirmed full application submitted following DIP accept.

Any insight or advise welcomed regarding this lender

thank you

0 -

Hi, we have been looking at properties to buy cash but have seen a house that would require a small mortgage. Excellent credit score, no debt and renting at moment. Never thought about registering on electoral roll for rented property and was on it in last property. Applied about 3 weeks ago. Got letter saying we would be added on 1st of June. Is this likely to be a problem when applying for a mortgage of around £30000. Earnings more than cover payments. Thanks0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards