We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

Sorry. When I put the details into Nationwide's 'How much can I borrow?' calculator.K_S said:

@doraspenlow Sorry it's not clear to me - who's saying that you can't borrow the extra 15k?doraspenlow said:Hello. Thanks for this thread. I am looking for some help on affordability. We'd like to take out Green Additional Borrowing with Nationwide to put solar panels on the roof, but currently the calculator is coming back with a big fat zero on what they will lend. Here's our situation:

House value: £465k

Mortgage outstanding: £230k

Would like to borrow about: £15k

Two borrowers, but only one earns. Full time permanent, on £70k pa

24.5 years left on mortgage term.

Three children, but discounting one as a dependant as he is 21 and works full time. Others are 19 (away at uni) and 11.

Currently £4300 on a 0% credit card (about 2 years left on the 0% so I haven't seen the point in hurrying to pay it).

£215 per month on a car lease (2 years to go).

What's best to do here? Even fully paying back the credit card leaves it tight on what they say they'll lend. To the point where if I then concede to spending £100 a month on petrol they won't do it. Are they really saying that we can't afford £90 a month extra on the mortgage to make energy bills lower?

Any advice, or maybe idiosyncracies about the Nationwide form it might help to know about. I would hate for them to be double counting anything. Maybe it's just a busted flush.0 -

@doraspenlow With the limited info and numbers in your post I would be surprised if you couldn't borrow what you needed and suspect it's just a matter of making it fit, most likely by stretching the term if at all possible (Nationwide will potentially go up to 75 for the older borrower) and/or or trimming the cc balance.doraspenlow said:

Sorry. When I put the details into Nationwide's 'How much can I borrow?' calculator.K_S said:

@doraspenlow Sorry it's not clear to me - who's saying that you can't borrow the extra 15k?doraspenlow said:Hello. Thanks for this thread. I am looking for some help on affordability. We'd like to take out Green Additional Borrowing with Nationwide to put solar panels on the roof, but currently the calculator is coming back with a big fat zero on what they will lend. Here's our situation:

House value: £465k

Mortgage outstanding: £230k

Would like to borrow about: £15k

Two borrowers, but only one earns. Full time permanent, on £70k pa

24.5 years left on mortgage term.

Three children, but discounting one as a dependant as he is 21 and works full time. Others are 19 (away at uni) and 11.

Currently £4300 on a 0% credit card (about 2 years left on the 0% so I haven't seen the point in hurrying to pay it).

£215 per month on a car lease (2 years to go).

What's best to do here? Even fully paying back the credit card leaves it tight on what they say they'll lend. To the point where if I then concede to spending £100 a month on petrol they won't do it. Are they really saying that we can't afford £90 a month extra on the mortgage to make energy bills lower?

Any advice, or maybe idiosyncracies about the Nationwide form it might help to know about. I would hate for them to be double counting anything. Maybe it's just a busted flush.

With a further advance for existing borrowers, even the broker affordability calculator does not give an accurate output and I always need to tinker with a DIP to get an accurate figure.

I would recommend speaking to a Nationwide adviser who can suggest a way to get what you need if it is possible. Good luck!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

2 -

Hello

Hopefully a quick question, very grateful for any reply

We had an offer through with Santander 2 months ago, on a porting application. Since then our chain fell apart. We agreed a new cheaper property purchase and have asked to amend the offer today.Apparently the affordability criteria have changed in the last 2 months. Do you know whether this will be taken into account and they’ll reduce the offer amount?I’d have thought if we are keeping our existing rate (port), the house we’re buying is cheaper, loan balance will be reduced and ltv same, it would be a simple switch. Or is that wishful thinking?

Thanks!0 -

Thank you. I appreciate your time.

Are there any other details I can give you to help see if it's doable? I'm happy to.

Not sure that an extension is possible. We already did one of about 3 years a while back (before we'd thought of this). We're 45 and 41.

Is this something a broker could help with, or do you definitely think just speaking to NW is enough? Sorry for the further questions.0 -

@rudipickup Unfortunately with Santander, they see a change of property as a "material change" and will recalculate affordability based on the current calculator even if nothing else has changed.rudipickup said:Hello

Hopefully a quick question, very grateful for any reply

We had an offer through with Santander 2 months ago, on a porting application. Since then our chain fell apart. We agreed a new cheaper property purchase and have asked to amend the offer today.Apparently the affordability criteria have changed in the last 2 months. Do you know whether this will be taken into account and they’ll reduce the offer amount?I’d have thought if we are keeping our existing rate (port), the house we’re buying is cheaper, loan balance will be reduced and ltv same, it would be a simple switch. Or is that wishful thinking?

Thanks!

Whether or not this will have an impact on what you need to borrow will depend on the numbers and how close to the max borrowing you were when you first applied.

If you're doing a like for like port (ie with no additional borrowing), lenders do sometimes show discretion so hopefully it works out in the end.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Ok thanks for the reply

Hopefully it works out as we’re taking a smaller loan given the cheaper house.0 -

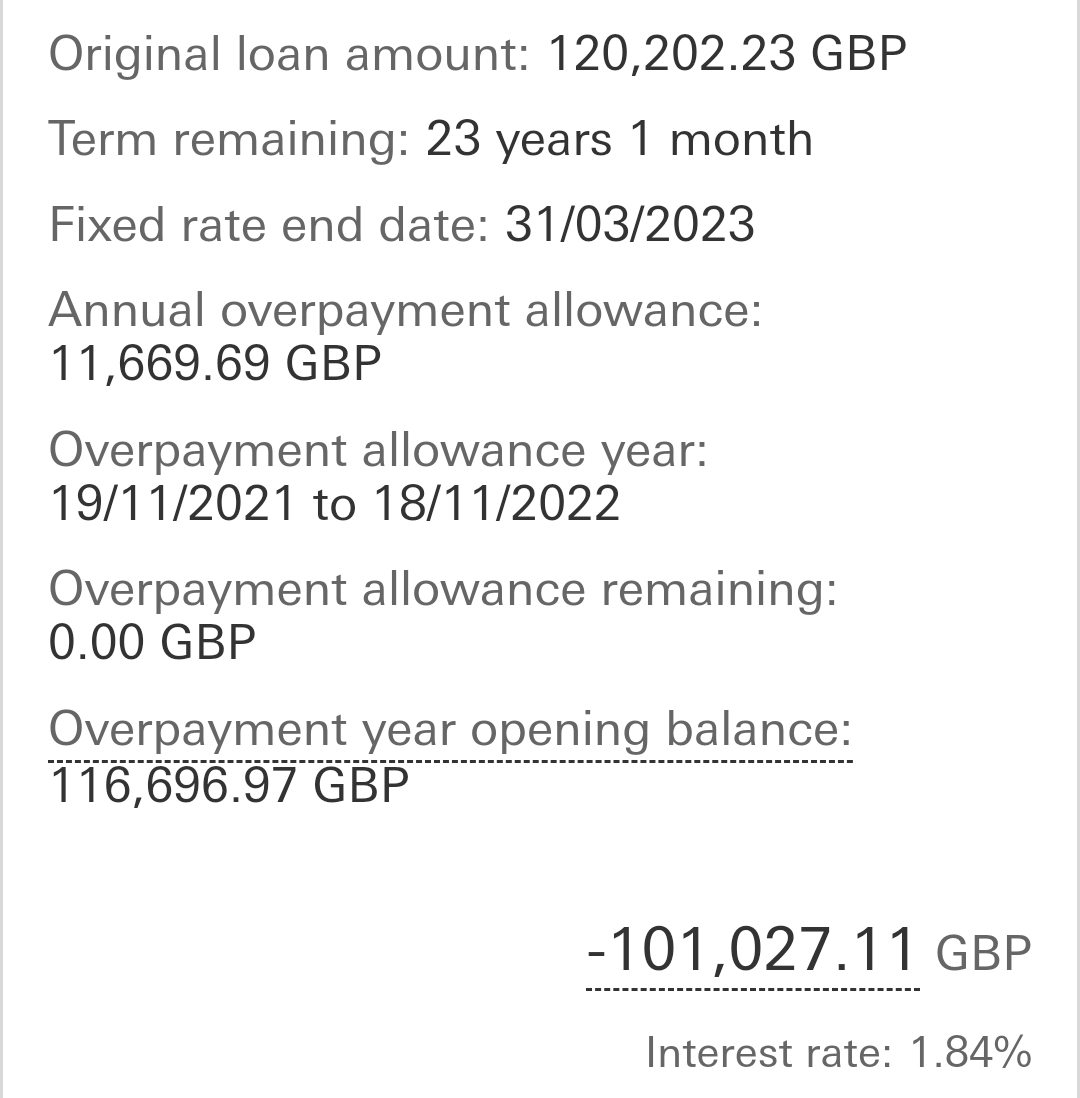

I'm a little bit confused by HSBCs ERC and hoping you can advise.

As you can see, our fixed rate is due to end in March '23, and given the rates of interest, I've decided to lock in a new rate now. That's at about 5.5% for 5 years.

As you can see, our fixed rate is due to end in March '23, and given the rates of interest, I've decided to lock in a new rate now. That's at about 5.5% for 5 years.

I've overpaid by the allowed 10% this year, and as soon as I take out the new deal I was going to overpay by the 10% again, so around £10k.

I was then considering overpaying by another c.£15k on top of the 10%, but know there's an Early Repayment Charge.

If it's worth doing given the penalties, I had a last minute thought, that I'd be best off doing this now with my fixed term about to end, than doing this when the new deal starts. Is that right? Trying to figure if I've understood that correctly!!

TIA0 -

Hi. We are using a broker and we are at the underwriting stage. Does the broker check statements etc before submitting so if anything doesn't look right would they flag it

Thanks0 -

@K_SK_S said:

@doraspenlow With the limited info and numbers in your post I would be surprised if you couldn't borrow what you needed and suspect it's just a matter of making it fit, most likely by stretching the term if at all possible (Nationwide will potentially go up to 75 for the older borrower) and/or or trimming the cc balance.doraspenlow said:

Sorry. When I put the details into Nationwide's 'How much can I borrow?' calculator.K_S said:

@doraspenlow Sorry it's not clear to me - who's saying that you can't borrow the extra 15k?doraspenlow said:Hello. Thanks for this thread. I am looking for some help on affordability. We'd like to take out Green Additional Borrowing with Nationwide to put solar panels on the roof, but currently the calculator is coming back with a big fat zero on what they will lend. Here's our situation:

House value: £465k

Mortgage outstanding: £230k

Would like to borrow about: £15k

Two borrowers, but only one earns. Full time permanent, on £70k pa

24.5 years left on mortgage term.

Three children, but discounting one as a dependant as he is 21 and works full time. Others are 19 (away at uni) and 11.

Currently £4300 on a 0% credit card (about 2 years left on the 0% so I haven't seen the point in hurrying to pay it).

£215 per month on a car lease (2 years to go).

What's best to do here? Even fully paying back the credit card leaves it tight on what they say they'll lend. To the point where if I then concede to spending £100 a month on petrol they won't do it. Are they really saying that we can't afford £90 a month extra on the mortgage to make energy bills lower?

Any advice, or maybe idiosyncracies about the Nationwide form it might help to know about. I would hate for them to be double counting anything. Maybe it's just a busted flush.

With a further advance for existing borrowers, even the broker affordability calculator does not give an accurate output and I always need to tinker with a DIP to get an accurate figure.

I would recommend speaking to a Nationwide adviser who can suggest a way to get what you need if it is possible. Good luck!

Just off the phone to Nationwide. Even with extending the term to 30 it's coming back as unaffordable, apparently. Nothing they can do. Won't let us speak to one of their proper advisors because the DIP was refused. Seems like a dead end.0 -

Do check at what point ERCs don't become payable, you don't want to be paying the ERC on the lot, just to increase your rate massively with under 6 months to go.Haywooddiablo said:I'm a little bit confused by HSBCs ERC and hoping you can advise.As you can see, our fixed rate is due to end in March '23, and given the rates of interest, I've decided to lock in a new rate now. That's at about 5.5% for 5 years.

I've overpaid by the allowed 10% this year, and as soon as I take out the new deal I was going to overpay by the 10% again, so around £10k.

I was then considering overpaying by another c.£15k on top of the 10%, but know there's an Early Repayment Charge.

If it's worth doing given the penalties, I had a last minute thought, that I'd be best off doing this now with my fixed term about to end, than doing this when the new deal starts. Is that right? Trying to figure if I've understood that correctly!!

TIAI'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards