We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

What number are you aiming for - solely DC pot

Comments

-

I understand a number of studies have shown this to Be sustainable over a 30+ year period with your withdrawal increasing by inflation each yearBritishInvestor said:

Reasonable on what basis?garmeg said:

3% seems a reasonable rule of thumb. What else do DC pot holders have to go on? Annuity rates make them barely worthwhile, at least before 65.BritishInvestor said:

I'd be wary about relying on this "rule of thumb"Mistermeaner said:Thinking about how much you want a year is great but dc pot only people don’t have that luxury - best rule of thumb is 3-4% of your pot as sustainable draw down income increasing each year with inflation

do you have a better way to calculate it ?Left is never right but I always am.1 -

That you run out of life before you run out of money.BritishInvestor said:

Reasonable on what basis?garmeg said:

3% seems a reasonable rule of thumb. What else do DC pot holders have to go on? Annuity rates make them barely worthwhile, at least before 65.BritishInvestor said:

I'd be wary about relying on this "rule of thumb"Mistermeaner said:Thinking about how much you want a year is great but dc pot only people don’t have that luxury - best rule of thumb is 3-4% of your pot as sustainable draw down income increasing each year with inflation3 -

Pretty sure BritishInvestor is a FA/IFA: maybe they could explain why 3-4% is unreasonable.Mistermeaner said:

I understand a number of studies have shown this to Be sustainable over a 30+ year period with your withdrawal increasing by inflation each yearBritishInvestor said:

Reasonable on what basis?garmeg said:

3% seems a reasonable rule of thumb. What else do DC pot holders have to go on? Annuity rates make them barely worthwhile, at least before 65.BritishInvestor said:

I'd be wary about relying on this "rule of thumb"Mistermeaner said:Thinking about how much you want a year is great but dc pot only people don’t have that luxury - best rule of thumb is 3-4% of your pot as sustainable draw down income increasing each year with inflation

do you have a better way to calculate it ?Most every study I’ve read on SWR suggests that is entirely reasonable.https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/ is pretty solid read.https://www.cnbc.com/2017/02/09/that-4-percent-rule-could-spell-trouble-for-early-retirees.html warns of “trouble”, but still suggests 3.5% is okay. Maybe you are Sam Dogan on that page.....

I’ve read some who suggest the UK should use 3-3.5%....although not really with any logic, to me, when one might be invested in precisely the same funds as an American....but either way, it still falls in the 3-4% range.

So: BritishInvestor, show us what you’re made of: why do you think 3% is unreasonable?Plan for tomorrow, enjoy today!1 -

1. The SWR assumption is based upon benchmark returns of broad asset classes. When you consider the potential real-world slippage that the "average" investor may experience such as:cfw1994 said:

Pretty sure BritishInvestor is a FA/IFA: maybe they could explain why 3-4% is unreasonable.Mistermeaner said:

I understand a number of studies have shown this to Be sustainable over a 30+ year period with your withdrawal increasing by inflation each yearBritishInvestor said:

Reasonable on what basis?garmeg said:

3% seems a reasonable rule of thumb. What else do DC pot holders have to go on? Annuity rates make them barely worthwhile, at least before 65.BritishInvestor said:

I'd be wary about relying on this "rule of thumb"Mistermeaner said:Thinking about how much you want a year is great but dc pot only people don’t have that luxury - best rule of thumb is 3-4% of your pot as sustainable draw down income increasing each year with inflation

do you have a better way to calculate it ?Most every study I’ve read on SWR suggests that is entirely reasonable.https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/ is pretty solid read.https://www.cnbc.com/2017/02/09/that-4-percent-rule-could-spell-trouble-for-early-retirees.html warns of “trouble”, but still suggests 3.5% is okay. Maybe you are Sam Dogan on that page.....

I’ve read some who suggest the UK should use 3-3.5%....although not really with any logic, to me, when one might be invested in precisely the same funds as an American....but either way, it still falls in the 3-4% range.

So: BritishInvestor, show us what you’re made of: why do you think 3% is unreasonable?

Platform fees

Active fund fees

Passive fund tracking error

Human behaviour (buying winning fund managers etc)

You'd need to be 100% sure that you were going to achieve returns pretty close to the benchmark.

2. Longevity. 30 years might be too conservative, especially if you are a couple.

That said, SWR is catering for the worst possible historical case, and most people, fortunately, didn't experience this.

There is the option of varying your spending dynamically according to market/inflationary outcomes.

https://finalytiq.co.uk/guyton-klinger-sustainable-withdrawal-rules/

0 -

You made it sound like 3-4% wasn’t reasonable. “Reasonable on what basis”, you said.BritishInvestor said:

1. The SWR assumption is based upon benchmark returns of broad asset classes. When you consider the potential real-world slippage that the "average" investor may experience such as:cfw1994 said:

Pretty sure BritishInvestor is a FA/IFA: maybe they could explain why 3-4% is unreasonable.Mistermeaner said:

I understand a number of studies have shown this to Be sustainable over a 30+ year period with your withdrawal increasing by inflation each yearBritishInvestor said:

Reasonable on what basis?garmeg said:

3% seems a reasonable rule of thumb. What else do DC pot holders have to go on? Annuity rates make them barely worthwhile, at least before 65.BritishInvestor said:

I'd be wary about relying on this "rule of thumb"Mistermeaner said:Thinking about how much you want a year is great but dc pot only people don’t have that luxury - best rule of thumb is 3-4% of your pot as sustainable draw down income increasing each year with inflation

do you have a better way to calculate it ?Most every study I’ve read on SWR suggests that is entirely reasonable.https://www.mrmoneymustache.com/2012/05/29/how-much-do-i-need-for-retirement/ is pretty solid read.https://www.cnbc.com/2017/02/09/that-4-percent-rule-could-spell-trouble-for-early-retirees.html warns of “trouble”, but still suggests 3.5% is okay. Maybe you are Sam Dogan on that page.....

I’ve read some who suggest the UK should use 3-3.5%....although not really with any logic, to me, when one might be invested in precisely the same funds as an American....but either way, it still falls in the 3-4% range.

So: BritishInvestor, show us what you’re made of: why do you think 3% is unreasonable?

Platform fees

Active fund fees

Passive fund tracking error

Human behaviour (buying winning fund managers etc)

You'd need to be 100% sure that you were going to achieve returns pretty close to the benchmark.

2. Longevity. 30 years might be too conservative, especially if you are a couple.

That said, SWR is catering for the worst possible historical case, and most people, fortunately, didn't experience this.

There is the option of varying your spending dynamically according to market/inflationary outcomes.

https://finalytiq.co.uk/guyton-klinger-sustainable-withdrawal-rules/

Then you quote Abraham’s post, which starts off with “More than 100 years of market data for a 60/40 portfolio puts the SWR for the UK at 3.7%”.

That article goes on to talk about the Guyton-Klinger rules, which aim to improve on things, and following those should see you being able to use 5.5%.

So.

Back to your first post on this topic: ‘ I'd be wary about relying on this "rule of thumb" ‘

Why are you wary of using 3-4%?

Or were you mysteriously building up to a punchline of “because you may die leaving too much money - take more!”?

Plan for tomorrow, enjoy today!0 -

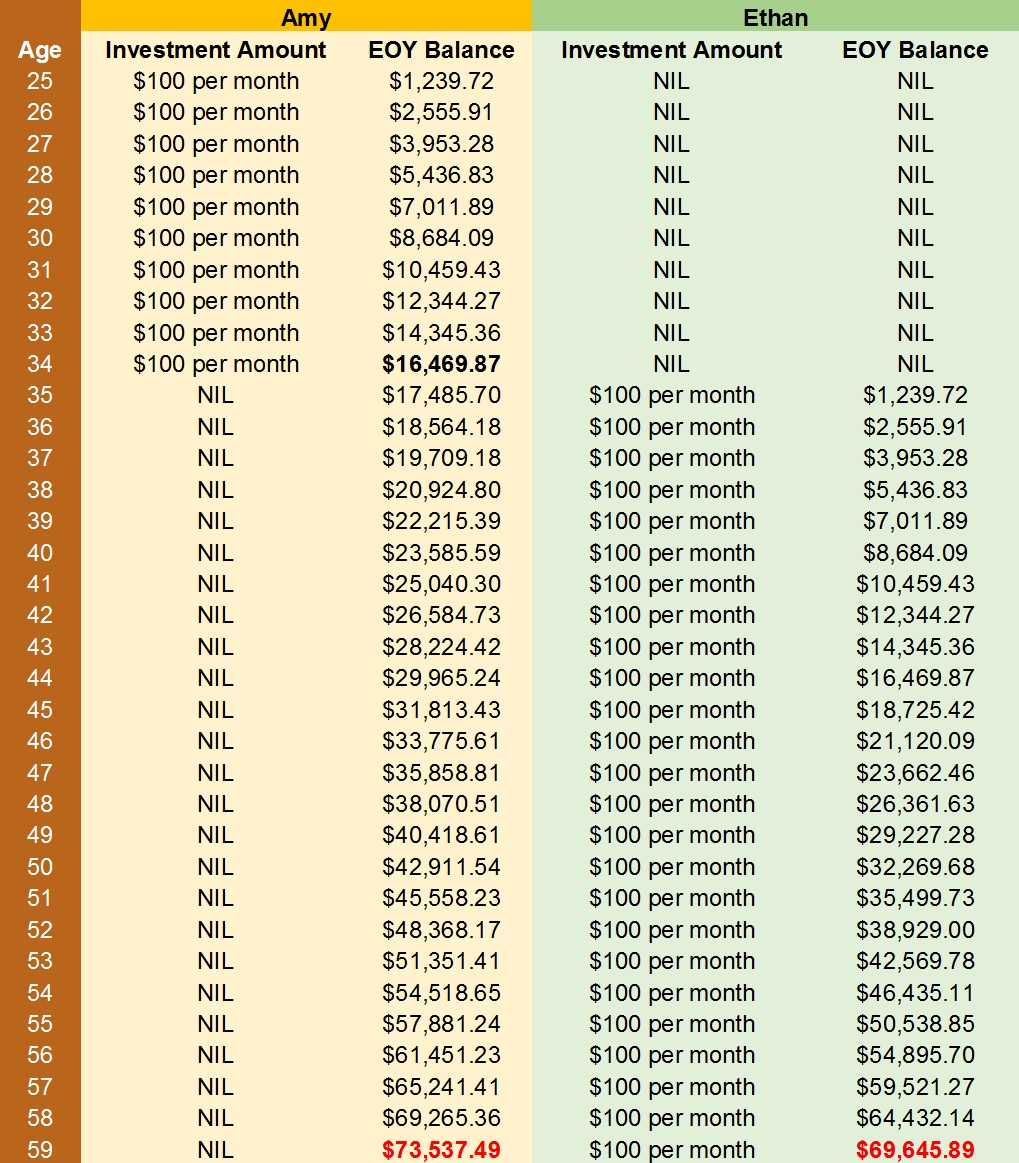

Thanks for this - I have seen a few of these images before but this is a nice clear one. I will be having this conversation with my daughter as she will be off to uni this year and I am trying to cover various life lessons in small doses over the next few months.Anonymous101 said:I’ve shared this, or something like it, many times with younger posters. Again the investment amounts or growth rates aren’t the main information. I think it illustrates the key take away that compounding is incredibly powerful and by investing whilst you’re letting time do most of the hard work.

For myself, I wish someone had pointed this out earlier. I have always been in a pension scheme, have always contributed enough to get the max employer contribution but for many years focussed on paying off the mortgage rather than paying more into the pension. I saw the light as I approached 50, decided that 58 would be a good time to retire (end of DD's uni course and end of mortgage) and then started to look at the numbers. Luckily OH has always paid more generously into a pension so he was in a better place.

I now sal sac 45% of my salary, get the 10% from employer on top but no NI contribution from them - this gets me into BR tax and means I put £40k into the pension. OH sal sac's £40k into his pension too. These are big numbers and they could have been smaller/smoother if I had started planning earlier - OH leaves all that sort of stuff to me.

We'll have an estimated £1.8m in pensions at 58 plus some ISAs. That will support our 'number'. If the world goes to hell in a handbasket then we could work longer but I would rather not. One tiny DB pension at 60 and then full SP at 67.I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.3 -

I disagree to an extent with that statement.Mistermeaner said:Thinking about how much you want a year is great but dc pot only people don’t have that luxury - best rule of thumb is 3-4% of your pot as sustainable draw down income increasing each year with inflation

The logical, to my mind, way of planing for retiremement is to identify what your target income is and then look at what the sources are. The latter, sources stage, is definitely easier with DB pension than with DC pension but the 3-4% guideline is a starting point.

If your target number is £15k a year and State Pension will give you £9k then you don't need a £1m DC pot. If your target is £50k a year then you may need north of £1m.6 -

Retiring very soon at 55, 750k in DC

Full State Pensions at 67 and 68

Downsizing, moving abroad and releasing another 100k in Equity

Currently cutting spending but am anticipating 35k a year, more on good years, less in bad1 -

Yup - thanks Anonymous101, great reminder!MallyGirl said:

Thanks for this - I have seen a few of these images before but this is a nice clear one. I will be having this conversation with my daughter as she will be off to uni this year and I am trying to cover various life lessons in small doses over the next few months.Anonymous101 said:I’ve shared this, or something like it, many times with younger posters. Again the investment amounts or growth rates aren’t the main information. I think it illustrates the key take away that compounding is incredibly powerful and by investing whilst you’re letting time do most of the hard work.

For myself, I wish someone had pointed this out earlier. I have always been in a pension scheme, have always contributed enough to get the max employer contribution but for many years focussed on paying off the mortgage rather than paying more into the pension. I saw the light as I approached 50, decided that 58 would be a good time to retire (end of DD's uni course and end of mortgage) and then started to look at the numbers. Luckily OH has always paid more generously into a pension so he was in a better place.

I now sal sac 45% of my salary, get the 10% from employer on top but no NI contribution from them - this gets me into BR tax and means I put £40k into the pension. OH sal sac's £40k into his pension too. These are big numbers and they could have been smaller/smoother if I had started planning earlier - OH leaves all that sort of stuff to me.

We'll have an estimated £1.8m in pensions at 58 plus some ISAs. That will support our 'number'. If the world goes to hell in a handbasket then we could work longer but I would rather not. One tiny DB pension at 60 and then full SP at 67.

I knocked up a version that also showed if you kept adding in...or indeed increased payments by the growth % - 5% in the example here:

Sure, there are plenty of unknowns....but if I'd appreciated that sooner, I'd be on my private island by now

I know I have happened upon some blogs on this over the years....& used this spreadsheet to remind our two about the power of early savings.

Plan for tomorrow, enjoy today!3 -

For anyone who remembers old school calculators the Holy Grail number to achieve was 5,318,008Deleted_User said:This is a thread for boasting. Cool7

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards