We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

Subsidence 12 years ago, House insurance queries...

delmonta

Posts: 502 Forumite

Hi, I bought my terraced house in Bristol 5 years ago. 12 years ago they had some relatively minor subsidence, due to a broken drain apparently.

I had a nightmare getting landlords insurance many years ago, but eventually got it with a broker. Now I'm moving back in and can't use them. I get some reasonable quotes coming up on comparison sites, but when I go to complete, they ask for some details about the subsidence, and I'm a bit confused...

- They ask for the cause, the only option that seems right is 'drain crash' Although I'm not certain what that means!

- They ask if the cause has been rectified or removed. I guess I can put removed, as they fixed the drain? But this was all before I lived there

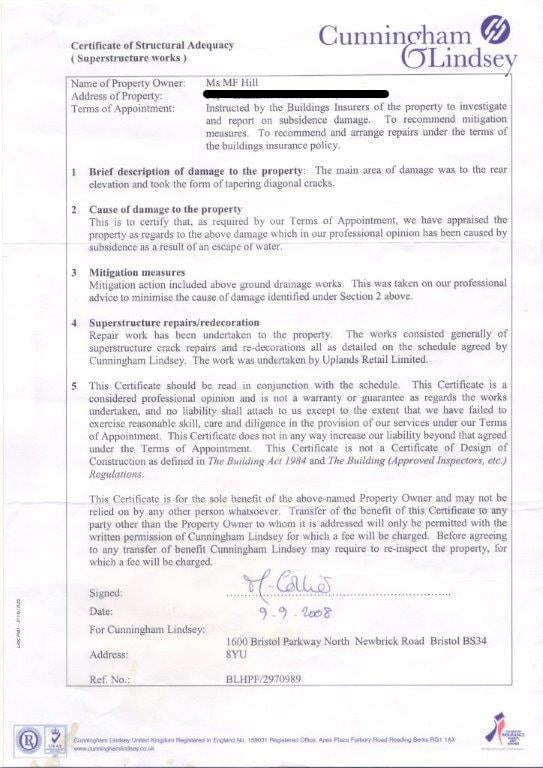

- And the main thing I'm confused about...they ask if I have a structural survey report. I do have these given to me by the last owner (attached images). But it says on these reports that the

surveys are for the benefit of the named property owner only, and I would have to pay a fee to get them transferred although they may want to do another survey. So can I say I have these reports for insurance, or not? It seems ridiculous if I had to pay for another expensive survey when the problem has been sorted and is no longer an issue.

- The last owner gave me two reports, one from 2008 when the issue arose, and one from 2010, when I'm guessing they came back to check on it. In the first report (attached) they say the subsidence was caused by escaped water (the drain). In the second report 2 years later they say it has been caused by consolidation subsidence! I'm so confused

- They ask for the cause, the only option that seems right is 'drain crash' Although I'm not certain what that means!

- They ask if the cause has been rectified or removed. I guess I can put removed, as they fixed the drain? But this was all before I lived there

- And the main thing I'm confused about...they ask if I have a structural survey report. I do have these given to me by the last owner (attached images). But it says on these reports that the

surveys are for the benefit of the named property owner only, and I would have to pay a fee to get them transferred although they may want to do another survey. So can I say I have these reports for insurance, or not? It seems ridiculous if I had to pay for another expensive survey when the problem has been sorted and is no longer an issue.

- The last owner gave me two reports, one from 2008 when the issue arose, and one from 2010, when I'm guessing they came back to check on it. In the first report (attached) they say the subsidence was caused by escaped water (the drain). In the second report 2 years later they say it has been caused by consolidation subsidence! I'm so confused

- Finally, the insurance company ask if there are any cracks above 2mm. I'm guessing they mean in the brick work, not the render?

Any advice would be greatly appreciated. My current insurance will be invalid very soon so I'm in a bit of a hurry!

thanks very much

thanks very much

1

Comments

-

@delmonta do you want to redact the property address from your images.

Mortgage started 2020, aiming to clear 31/12/2029.1 -

Aggregator sites have a common set of questions which work to varying degrees to for the different insurers and brokers that quote on them. Many don't have the identical questions/answers on their websites and so will use certain mapping rules to get a best proxy but you need to check all the details are right when you get through to the brokers/insurers website.

I would do the quote on your best understanding of the questions, find the company you like the look of and double check everything when you get to their site. If there are still things you aren't sure on double check with that particular company.

For cracks I would have anticipated it was any cracks and not just brickwork but again that would be for the company to confirm if you are in doubt.

1 -

Thanks, I am talking about when I get to the insurers websites after doing the comparison. As I said I had subsidence in the past, instead of just paying they ask me specific questions about subsidence.Sandtree said:Aggregator sites have a common set of questions which work to varying degrees to for the different insurers and brokers that quote on them. Many don't have the identical questions/answers on their websites and so will use certain mapping rules to get a best proxy but you need to check all the details are right when you get through to the brokers/insurers website.

I would do the quote on your best understanding of the questions, find the company you like the look of and double check everything when you get to their site. If there are still things you aren't sure on double check with that particular company.

For cracks I would have anticipated it was any cracks and not just brickwork but again that would be for the company to confirm if you are in doubt.I know often with insurance you can get it, or even call up and speak to someone at the call centre who will say its fine, only later to find out its void for some reason or other. I just dont want to risk that but I'm a bit confused about this situation0 -

No matter what you do there is always a risk but if you email them and get a response or a LiveChat transcript or note the time/date and number you called from for a telephone call and insurer would be exceptionally lucky to get away with anything but paying your claim in full if you entered the data they advised you to do upon explaining the situation and they said that was the correct way to answer.1

-

Maybe you would be better off avoiding comparison sites. They are aimed at the average house with average needs and average issues. If you fall outside that, you tend to find issues. Either at application or at claim.

Insurers that focus on the unusual or rural properties usually dont bat an eyelid when it comes to minor movement or movement that has been resolved.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Yeah you are right, I should get evidence of anything they advise. I'm just a bit confused in general about the whole subsidence issue. If it was caused by a drain and has been fixed, why do you still have to tell people. It's also an issue when selling the house. I understand if it was due to the land, but not due to an error that was fixed.Sandtree said:No matter what you do there is always a risk but if you email them and get a response or a LiveChat transcript or note the time/date and number you called from for a telephone call and insurer would be exceptionally lucky to get away with anything but paying your claim in full if you entered the data they advised you to do upon explaining the situation and they said that was the correct way to answer.0 -

Yeah thats what I had to do years ago as almost nobody would insure me. But it seems to have changed now, you can enter that you had subsidence on comparison sites and you get a lot of options at the end. But yes they are asking some questions which I need to find solid answers todunstonh said:Maybe you would be better off avoiding comparison sites. They are aimed at the average house with average needs and average issues. If you fall outside that, you tend to find issues. Either at application or at claim.

Insurers that focus on the unusual or rural properties usually dont bat an eyelid when it comes to minor movement or movement that has been resolved.0 -

Insurance works on probability and statistically something that has broken once is more likely to break a second time. Similarly we had a broken drain years ago and it caused no problems to our house but clearly there is "something different" (I'm not an engineer) which means the same problem with your drain caused subsidence rather than just a stink. Again this means a repeat problem and more chances of the same problem.delmonta said:

I'm just a bit confused in general about the whole subsidence issue. If it was caused by a drain and has been fixed, why do you still have to tell people. It's also an issue when selling the house.

I'd be a touch less concerned on the selling issue... you will (or should have) gotten the house for a lower price due to its previous subsidence problem. When you go to sell the house, assuming no more problems, then the issue will be more remote and so have less of an impact on the price and you will be quids in. Obv the ones that have the real trouble are the people that buy a house with no problems, have major subsidence whilst they own it and then try to sell it 12 months later.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards