We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

How to get a private pension (Not employer)

I am wondering if it is possible to have a second pension, in adition to that one provided by the employer. My employer HR is based abroad, with solicitors normally being subcontracted to do the local UK taxes and what not - and I have historically found it very hard to have any sort of agreements to change the default pension values.

For this reason - I would like to contribute myself, taking advantage of the automatic 20% tax boost on any deposits - But i don't see how i can open a pension of my own - this seems to only be possible for those registered as self employed or through an employer.

Any lines of advise?

Comments

-

You can open a personal pension yourself; you don't even need to be employed or have any earnings to do so. Look back at some of the threads on this forum and you'll find plenty of info or look at https://www.moneysavingexpert.com/savings/discount-pensions/ (no point in repeating all that information here).

Otherwise google on 'opening a personal pension' and links a-plenty will pop up!Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

I would recommend that you look at an online company called Nutmeg as a very simple and straightforward option for opening a personal pension account. People often mention that their charges aren't particularly cheap, but they take care of all the 'complicated stuff' for you and have a very clear, plain English, online interface. Reading between the lines of your post, I suspect that, like me, that's what you want.0

-

For this reason - I would like to contribute myself, taking advantage of the automatic 20% tax boost on any deposits -

There isn't a 20% boost. Tax relief is 20% (assuming basic rate or not rate taxpayer). If you refer to it as a boost then it would be 25%.

But i don't see how i can open a pension of my own - this seems to only be possible for those registered as self employed or through an employer.All retail individual pensions will take contributions from you as long as you are a UK resident and you have relevant earnings.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

I would say that opening a SIPP with Vanguard and putting your money into one of their Lifestrategy funds would be a cheaper alternative to Nutmeg. They have five globally diverse multi asset funds that are named from Lifestrategy20 - Lifestrategy100. LS 20 having (in theory) the least amount of growth but the least amount of volatility and LS100 having the best growth but (again in theory) greater variation in the day to day fund price. If you have over ten years till you wish to claim your pension I would recommend just opening an account and making a regular payment into LS100 and forget about it for a while.

Edit: They will claim your tax relief for you automatically and add it to your account. If you are a higher rate tax payer you will have to sort that out separately.Think first of your goal, then make it happen!0 -

Thank you all for your comments.

Are the fees realy relevant - once all gains are taken into account (do these mean better investments, for example)? Also, is it wise to move older pensions (from previous employers) into a single fund or better to diversify and keep them separate?0 -

Throwing some figures out. Growth (included re-invested dividends) at say 6%, inflation at 2% and high fees 1.5% will mean only 2.5% real growth.cts_casemod said:Thank you all for your comments.

Are the fees realy relevant - once all gains are taken into account (do these mean better investments, for example)? Also, is it wise to move older pensions (from previous employers) into a single fund or better to diversify and keep them separate?

The funds above have 0.22% fees with a capped platform fee.0 -

Are fees relevant? Of course they are, especially over an extended time period. See https://www.thisismoney.co.uk/money/pensions/article-3802276/Rip-pension-charges-slogging-work-longer.htmlGoogling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

-

Also, is it wise to move older pensions (from previous employers) into a single fund or better to diversify and keep them separate?

There is no right or wrong answer to this .

Firstly diversify in this context means diversity of your investments within the pensions, For example making sure you have not too high % in one part of the world . Or too much concentration of equity investments for your risk tolerance, age etc

Diversity of the pension providers that hold the investments is less important . For example if you have fund XYZ in one pension and the same /similar in another pension , then that is not diversifying .( although its quite common)

However there may be some advantages in charges by merging pensions and easier admin.

It is easy to transfer most pensions as it easy to open one .

0 -

Cheers -

Here are some facts that could be of help for someone that gets it more than me, regarding my current pension:- Provider: AVIVA

- Plan: Aviva Pension BlackRock (50:50) Global Equity Index Tracker IE Plan.

- Currently the fund went down a bit: £15346 (out of just over 16K invested)

- 0.51 % Annual Management Charge

- The interface is limited to say the best.

- I can't find a way to add funds myself.

- I dont know how to track the gains/losses/projections over time (no graphs, just current value)

As to my current employer - The pension is not set yet - it will be with a company called 'friends lift' - if this is of any relevance.0 -

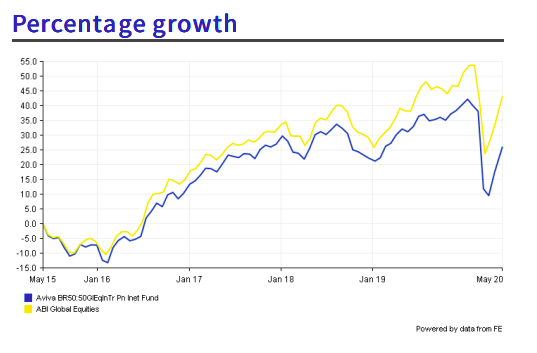

I can't find a way to add funds myself.My Aviva > Pension, Details > Make a single payment. (Can't find where to make a regular contribution - maybe ring them up?Pension Summary > How my pension is invested > Research funds, search for 'Global Equity Index Tracker' and open the 50:50 one. Graph from the pdf:I dont know how to track the gains/losses/projections over time (no graphs, just current value)

Or https://markets.ft.com/data/funds/tearsheet/summary?s=GB00BDH3PV81:GBP (at least that's the one that the PDF is for.)Conjugating the verb 'to be":

-o I am humble -o You are attention seeking -o She is Nadine Dorries0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 352K Banking & Borrowing

- 253.5K Reduce Debt & Boost Income

- 454.2K Spending & Discounts

- 245K Work, Benefits & Business

- 600.6K Mortgages, Homes & Bills

- 177.4K Life & Family

- 258.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.2K Discuss & Feedback

- 37.6K Read-Only Boards