We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Nudge in the right direction

bungleberg

Posts: 58 Forumite

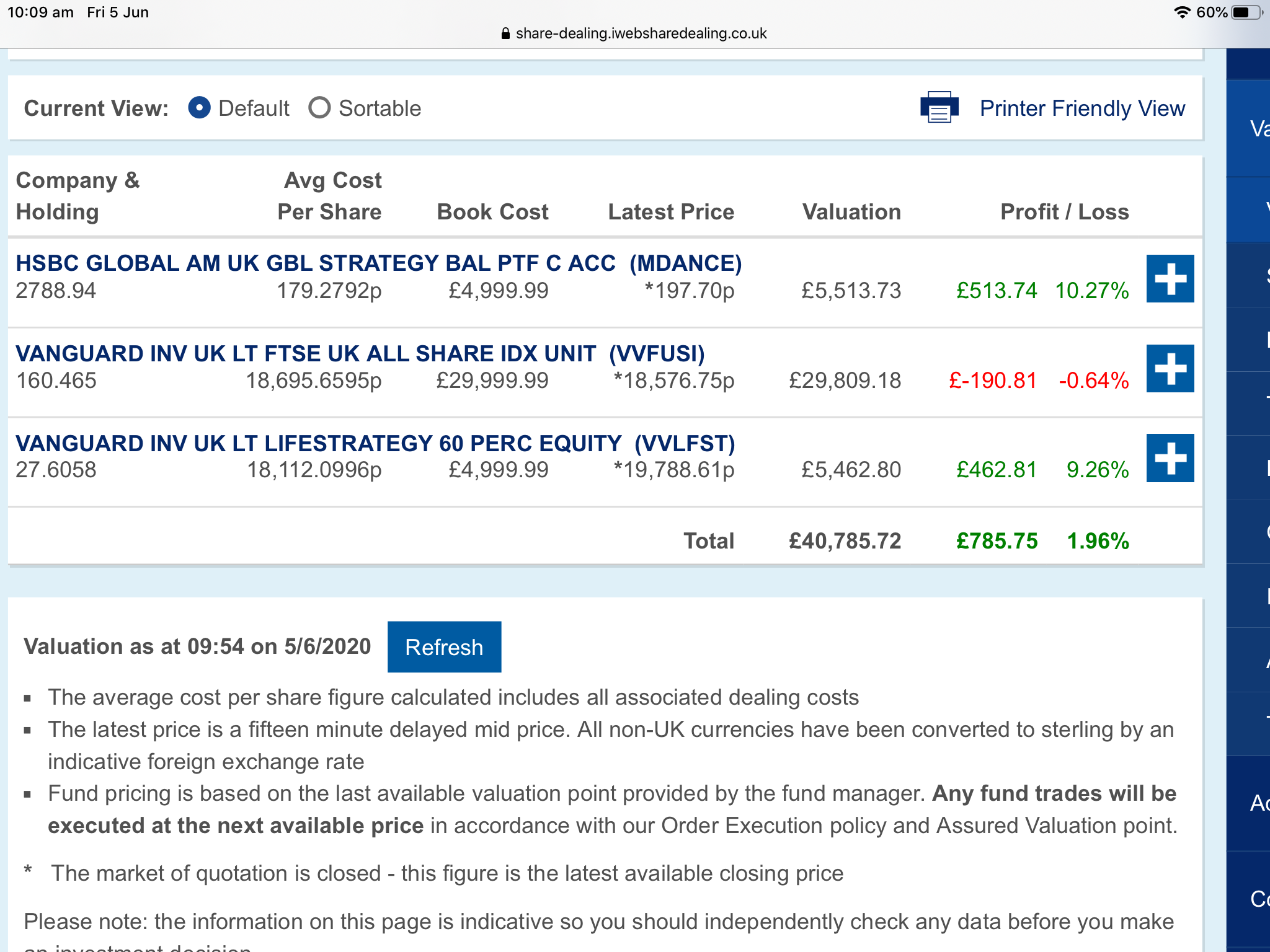

I’m 51 today and a reasonably new and novice investor. Mortgage free and have a decent size savings pot outside of the markets.

I’m 51 today and a reasonably new and novice investor. Mortgage free and have a decent size savings pot outside of the markets. I switched my cash ISA to stocks and shares just before the Covid 19 outbreak.

So it inevitably dropped, I opened a standard share dealing account and chucked some money in the FTSE all share at various points, on the way down. I believe it’s called trying to catch a falling knife!! I also added to my ISA in this new tax year and some of it has made a profit. After reading and digesting info on this forum. I have realised that a narrow spectrum index such as the FTSE Allshare is not the best investment. I made the decision to sell the FTSE All-share holding today as it’s virtually broke even and hopefully will not change too much by the time the order goes through the order goes through.

So it inevitably dropped, I opened a standard share dealing account and chucked some money in the FTSE all share at various points, on the way down. I believe it’s called trying to catch a falling knife!! I also added to my ISA in this new tax year and some of it has made a profit. After reading and digesting info on this forum. I have realised that a narrow spectrum index such as the FTSE Allshare is not the best investment. I made the decision to sell the FTSE All-share holding today as it’s virtually broke even and hopefully will not change too much by the time the order goes through the order goes through.

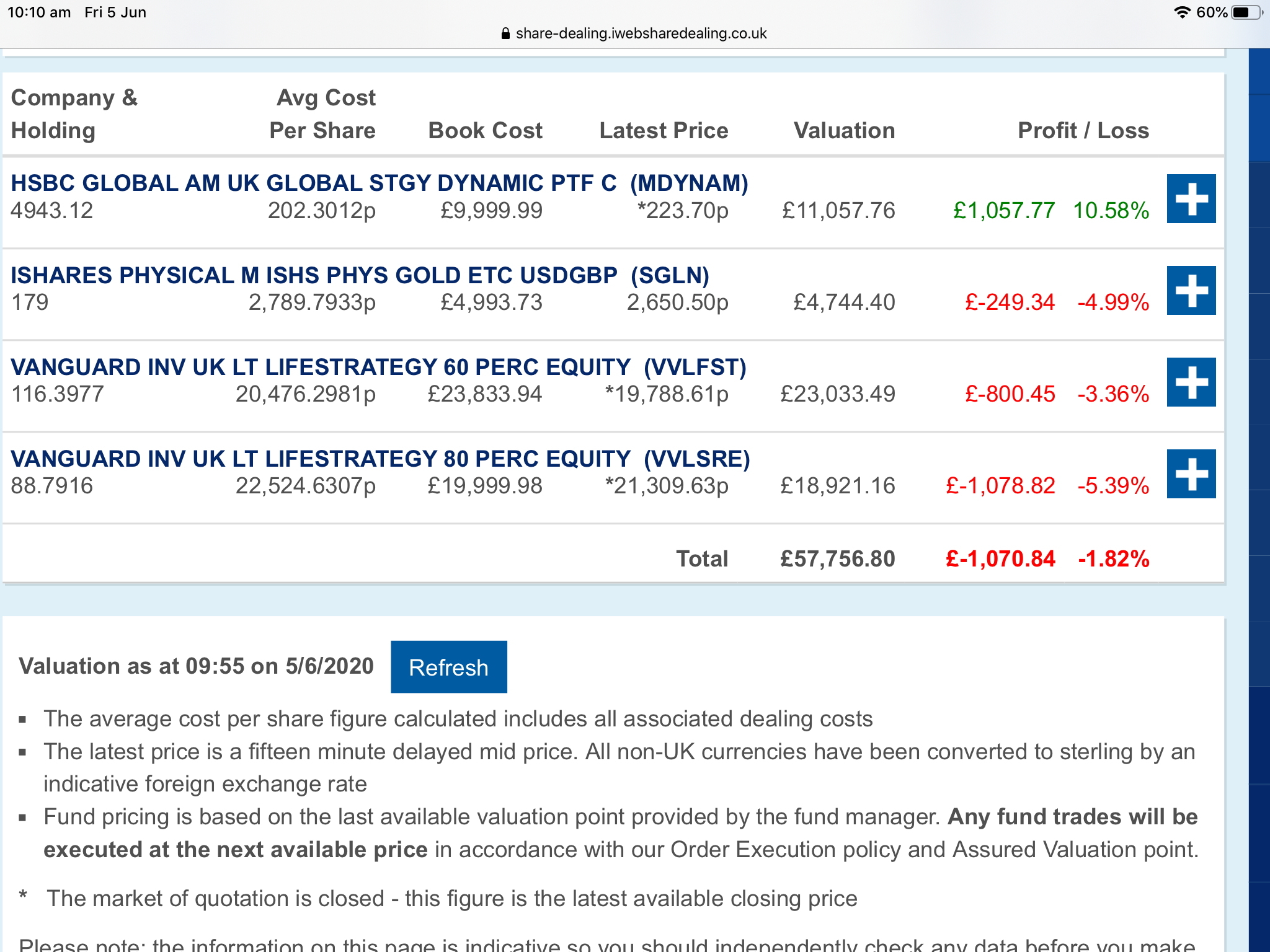

I wish to reinvest the capital in something more diversifies such as the Vanguard Lifestyle Strategies or the HSBC Dynamic/ Balanced Funds.

I’ve looked at the VWRL Vanguard Global ETF but what concerns me is that the dividends are paid in US. dollars so exchange rate can affect things.

I’m just after opinion on whether I should stay with the Funds I am currently invested in or perhaps invest in some different ones.

0

Comments

-

Good decision to dump the FTSE all share.Do NOT buy VLS because you woudl be buying back 25% of it, eg the top of the FTSEAS, due to its artificial "UK" 25% weighting.You are going to be affected by exchange rates if you buy global so I woudlnt worry about dividends in dollars because effectively so is all of it.Buy a global fund, mixed with bonds if thats your thing, and dont worry about exchange rates, thats inescapable.EDIT; Am i reading it right, have you also already got VLS60/60 /80? I would change those for another global balanced fund like HSBC (and I think LG do some?) on the same basis, eg that 25% of those are essentially your FTSEAS you just decided (wisely) to sell.1

-

Yes I do have the VLS 60/80, they were the bought just prior to COVID -19 outbreak as a switch from a cash ISA. Are you suggesting the funds would be better in the HSBC balanced/dynamic funds due to them have a more global allocation compared to the VLS 25% UK Weighting.AnotherJoe said:Good decision to dump the FTSE all share.Do NOT buy VLS because you woudl be buying back 25% of it, eg the top of the FTSEAS, due to its artificial "UK" 25% weighting.You are going to be affected by exchange rates if you buy global so I woudlnt worry about dividends in dollars because effectively so is all of it.Buy a global fund, mixed with bonds if thats your thing, and dont worry about exchange rates, thats inescapable.EDIT; Am i reading it right, have you also already got VLS60/60 /80? I would change those for another global balanced fund like HSBC (and I think LG do some?) on the same basis, eg that 25% of those are essentially your FTSEAS you just decided (wisely) to sell.

0 -

bungleberg said:

Yes I do have the VLS 60/80, they were the bought just prior to COVID -19 outbreak as a switch from a cash ISA. Are you suggesting the funds would be better in the HSBC balanced/dynamic funds due to them have a more global allocation compared to the VLS 25% UK Weighting.AnotherJoe said:Good decision to dump the FTSE all share.Do NOT buy VLS because you woudl be buying back 25% of it, eg the top of the FTSEAS, due to its artificial "UK" 25% weighting.You are going to be affected by exchange rates if you buy global so I woudlnt worry about dividends in dollars because effectively so is all of it.Buy a global fund, mixed with bonds if thats your thing, and dont worry about exchange rates, thats inescapable.EDIT; Am i reading it right, have you also already got VLS60/60 /80? I would change those for another global balanced fund like HSBC (and I think LG do some?) on the same basis, eg that 25% of those are essentially your FTSEAS you just decided (wisely) to sell.Absolutely. You wisely sold the FTSEAS.But in effect, of the equity component of each VLSxx , 25% of that is FTEAS. O of VLS60, 15% = FTSEAS. And VLS80, 20% is. So you've still got a fair chunk of FTSEAS.I would swap it for a Vanguard, HSBC or L&G equivalent equity/bond fund that doesn't have the artificial weighting of 25% UK.0 -

Apart from the UK weighting , what appear to be very similar multi asset funds from different providers do not move exactly in tandem . So IMHO it is a good idea to have more than one anyway , although not everybody seems to agree.1

-

If the FTSEAS fund has been sold then the OP has already removed some home bias. A lot depends on how much further to go for the sake of diversity. VLS80 allocates 4 x more capital to the UK than the FTSE All-World tracker (a lot) but the HSBC Dynamic/ Balanced Funds option has > 3x the charges.

However, I do think these lifestrategy type offers are solving a problem that doesn't exist because 80% VWRL & 20% VGOV is a better diversified, cheaper and simpler VLS80. Not exactly like for like but close enough for many I would've thought.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards