We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Lack of cover for coronavirus with travel insurers - am I the idiot here?

frankiefmg

Posts: 5 Forumite

Hi everyone, first time post so please be kind. Thank you in advance for any of the advice I may receive.

Myself and my fiance booked a once in a lifetime trip to Canada and the US in December 2019, we are supposed to travel at the end of August and into September 2020. My annual travel insurance policy expired in February and I took out a new policy with Coverforyou. I (perhaps stupidly) assumed that my travel insurance would cover me against being unable to travel due to coronavirus restrictions, having taken the policy out in February and booking the trip in December. It was not until they wrote to me at the end of March that I realised I did not have an optional "Trip Disruption cover" and thus am not covered.

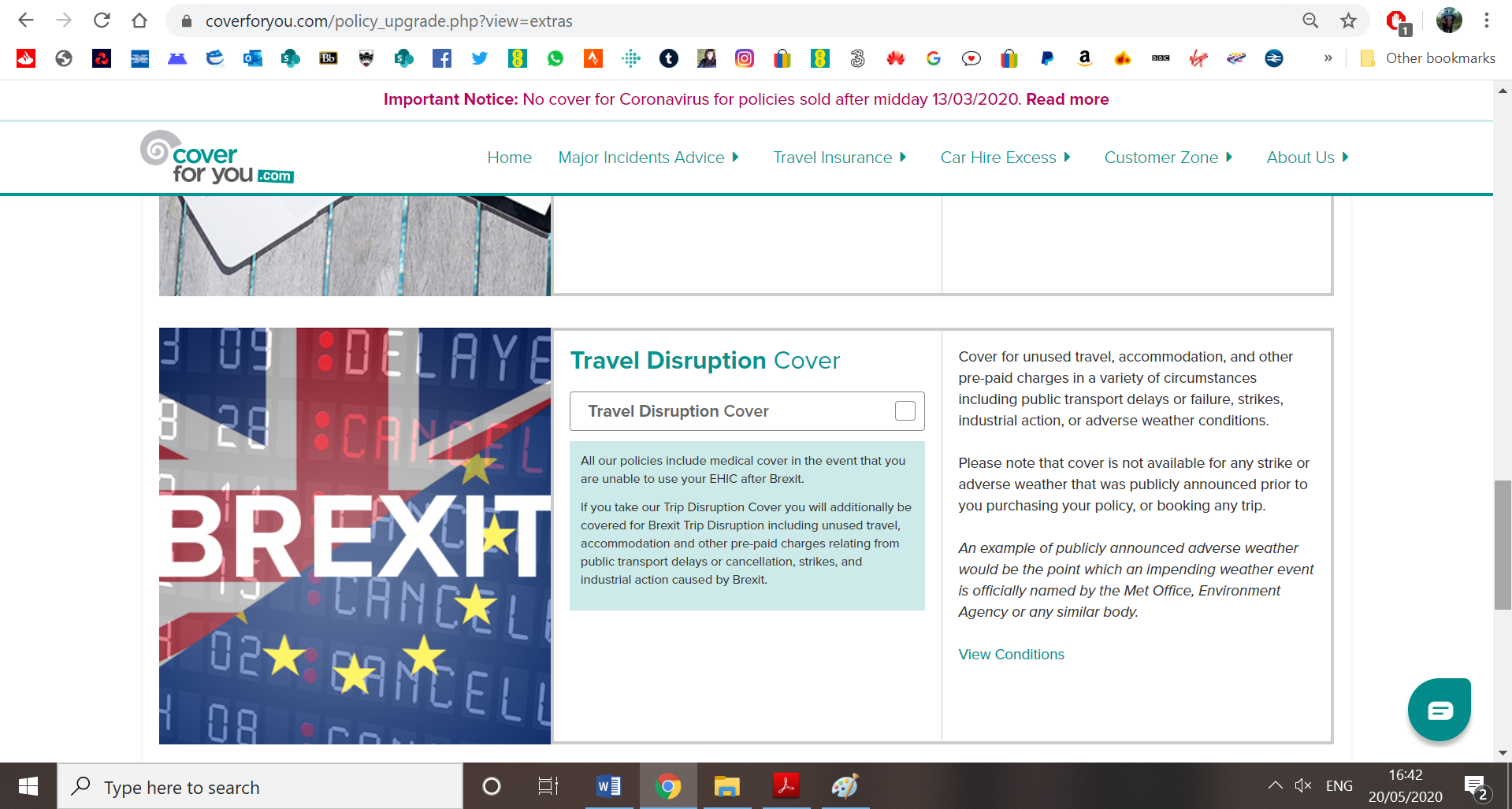

I took out the policy the week that we left the EU and at the time they were selling an add-on described as "Brexit Travel Insurance" (some pictures below), I wrongly assumed that this was an add-on relating to delays that may occur as a result of Brexit and as I foresaw none I did not purchase the add-on. As it turned out this was actually an add-on for overall trip disruptions and not just for delays that would potentially occur as a result of Brexit.

I have since written to them to say that I was misled by their marketing and do obviously require trip disruption cover - we have booked a multi-city holiday with various flights, hotels, car hires and ferry crossings (all booked independently). We are also visiting an active volcano and so obviously require some level of cancellation cover. They have replied saying that as the trip disruption add-on was available at the time of purchase they believe that I purposefully opted out of buying such cover. This is not the case as I genuinely thought the policy would cover FCO advice as a minimum, and that I was being sold a Brexit product. I've never claimed on travel insurance before (despite having always purchased it), so it seems ludicrous to me that it doesn't cover you for cancellations by default.

I have requested that, if I buy the optional Trip Disruption add-on now, they honour the T&C's that would have been in place had I bought it in February - essentially covering me for coronavirus cancellations. They have declined, sending me 10 pages of the Trip Disruption T&Cs that were available to me in February (felt like salt in the wounds, to be honest).

My next step was to take the case to the Financial Ombudsman Service - I had hoped for a little more empathy given the time at which I bought the policy (several days after Brexit) and the fact that I felt their marketing hid an essential piece of cover behind a nonessential add-on. My partner's policy with another insurer does include FCO advice as standard, and was notably cheaper than mine!

I was wondering if fellow MSE users thought I had a case for the FOS or whether this really was just my own fault for interpreting the product and it's T&Cs incorrectly. I should add I'm not intending to cancel the holiday, I am not claiming, and very much still hope we can go (more so now after I know I have no insurance to cover it :'( ), but unfortunately it is looking increasingly more like it will not be possible.

TIA

Myself and my fiance booked a once in a lifetime trip to Canada and the US in December 2019, we are supposed to travel at the end of August and into September 2020. My annual travel insurance policy expired in February and I took out a new policy with Coverforyou. I (perhaps stupidly) assumed that my travel insurance would cover me against being unable to travel due to coronavirus restrictions, having taken the policy out in February and booking the trip in December. It was not until they wrote to me at the end of March that I realised I did not have an optional "Trip Disruption cover" and thus am not covered.

I took out the policy the week that we left the EU and at the time they were selling an add-on described as "Brexit Travel Insurance" (some pictures below), I wrongly assumed that this was an add-on relating to delays that may occur as a result of Brexit and as I foresaw none I did not purchase the add-on. As it turned out this was actually an add-on for overall trip disruptions and not just for delays that would potentially occur as a result of Brexit.

I have since written to them to say that I was misled by their marketing and do obviously require trip disruption cover - we have booked a multi-city holiday with various flights, hotels, car hires and ferry crossings (all booked independently). We are also visiting an active volcano and so obviously require some level of cancellation cover. They have replied saying that as the trip disruption add-on was available at the time of purchase they believe that I purposefully opted out of buying such cover. This is not the case as I genuinely thought the policy would cover FCO advice as a minimum, and that I was being sold a Brexit product. I've never claimed on travel insurance before (despite having always purchased it), so it seems ludicrous to me that it doesn't cover you for cancellations by default.

I have requested that, if I buy the optional Trip Disruption add-on now, they honour the T&C's that would have been in place had I bought it in February - essentially covering me for coronavirus cancellations. They have declined, sending me 10 pages of the Trip Disruption T&Cs that were available to me in February (felt like salt in the wounds, to be honest).

My next step was to take the case to the Financial Ombudsman Service - I had hoped for a little more empathy given the time at which I bought the policy (several days after Brexit) and the fact that I felt their marketing hid an essential piece of cover behind a nonessential add-on. My partner's policy with another insurer does include FCO advice as standard, and was notably cheaper than mine!

I was wondering if fellow MSE users thought I had a case for the FOS or whether this really was just my own fault for interpreting the product and it's T&Cs incorrectly. I should add I'm not intending to cancel the holiday, I am not claiming, and very much still hope we can go (more so now after I know I have no insurance to cover it :'( ), but unfortunately it is looking increasingly more like it will not be possible.

TIA

0

Comments

-

Insurance cover varies widely from policy to policy. Onus is on the applicant to ensure that the cover procured meets their own requirements. Did you use a comparison site?

0 -

It was 4 months ago but from memory I think I found them via a comparison site and then visited their website directly.Thrugelmir said:Insurance cover varies widely from policy to policy. Onus is on the applicant to ensure that the cover procured meets their own requirements. Did you use a comparison site?

Edit: I also checked the cover had enough cancellation to cover my holiday. I was not aware/it was not clear to me that there were different criteria to be eligible for cancellation (e.g. medical or due to trip disruption).0 -

I feel the first question will be "Did you read your policy in the 14 day cooling-off period?"

Is it a DIY trip or a package holiday?

New User name as MSE gave me a number in my old one.

" I am not a number! I am a free man!"0 -

I read the 6 page Product Information Document which made no reference to trip disruption cover being an add-on, just stated:Life__Goes__On said:I feel the first question will be "Did you read your policy in the 14 day cooling-off period?"

Is it a DIY trip or a package holiday?

"We will pay up to £2,000 per person for your unused and irrecoverable costs if you have to cancel or cut short your trip as a result of one of a number of covered scenarios."

The breakdown of this was in their 42-page Policy Wording, stating on page 34 that Trip Disruption Cover is "only operative if indicated in the schedule".

Yes, it is a DIY holiday.

0 -

I sympathise as I always find insurance details confusing and laborious reading but I doubt you will get them to change their minds. You declined what was on offer at the time because you felt you didn't need it and although you didn't really understand what you were declining I don't think this would be a valid excuse (in their view). No harm in trying though.

You may just have to hope your trip is either cancelled completely, or goes ahead without any problems. Sorry - I can feel your pain and (not quite as much at stake as you) but I took out holiday cover for a staycation last month that didn't go ahead. I took it out in December before the name Coronavirus had entered 'my dictionary' and would you believe in the small print somewhere it excludes pandemics!!! Never even gave a pandemic a thought at the time. I know I will be going through any future insurance policies with a fine tooth comb!1 -

Thank you. I probably will refer to FOS, as I guess I have nothing to lose, I just didn't want to get my hopes too high depending on the MSE feedback. I am a frontline worker and I do so very hope that I do get to go on my holiday :'( I too will be reading future policies scrupulously.Tedber said:I sympathise as I always find insurance details confusing and laborious reading but I doubt you will get them to change their minds. You declined what was on offer at the time because you felt you didn't need it and although you didn't really understand what you were declining I don't think this would be a valid excuse (in their view). No harm in trying though.

You may just have to hope your trip is either cancelled completely, or goes ahead without any problems. Sorry - I can feel your pain and (not quite as much at stake as you) but I took out holiday cover for a staycation last month that didn't go ahead. I took it out in December before the name Coronavirus had entered 'my dictionary' and would you believe in the small print somewhere it excludes pandemics!!! Never even gave a pandemic a thought at the time. I know I will be going through any future insurance policies with a fine tooth comb!0 -

Travel insurance cover levels are an absolute nightmare - the thing with insurance is it covers a pre-defined set of scenarios, not everything with some exclusions.

I have every sympathy, as I hate pawing through pages of paperwork when taking out a new policy - these days I just tend to get the bare minimum medical cover and take the risk myself. There's next to zero chance of these companies paying up anyway in my experience.0 -

I've mattyprice4004 said:

Exclusions and limiting the extent of cover helps keep the cost of cover down. As that's what people want. Bottom line is they want it as cheap as possible. Otherwise they feel there's no value to be had.Travel insurance cover levels are an absolute nightmare - the thing with insurance is it covers a pre-defined set of scenarios, not everything with some exclusions.0 -

I agree with you but I personally was happy to pay what was required. I had already paid for an excess waiver, a health condition premium and for additional sports cover. I just didn't realise that travel insurance doesn't cover travel disruption by default, and thought they were offering me a niche add-on as part of a Brexit promotion.Thrugelmir said:I've mattyprice4004 said:

Exclusions and limiting the extent of cover helps keep the cost of cover down. As that's what people want. Bottom line is they want it as cheap as possible. Otherwise they feel there's no value to be had.Travel insurance cover levels are an absolute nightmare - the thing with insurance is it covers a pre-defined set of scenarios, not everything with some exclusions.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards