We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Business Bounce Back Loan terms and conditions for repaying the loan early

extrovert

Posts: 12 Forumite

Dear all

I recently applied for a bounce back loan with HSBC for my company. The loan has been approved and I have been sent a loan agreement to sign and return to receive the funds in my business account. However the terms and conditions relating to overpayment / early repayment are not clear. I have contacted HSBC's help line to no avail.

I intend to pay back the loan as soon as I can but use it during the current difficult times to survive as the loan does not cost my business anything for the first 12 months. The terms and conditions relating to the overpayment / early repayment suggest that I will be charged accrued interest for the overpayments / early settlement of the loan.

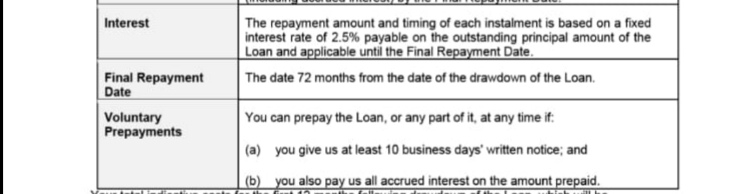

I have attached a picture of the terms and conditions. Please could anyone explain if I incur any interest if I let suppose pay off the loan in full in 11th month for example. Thanks

I recently applied for a bounce back loan with HSBC for my company. The loan has been approved and I have been sent a loan agreement to sign and return to receive the funds in my business account. However the terms and conditions relating to overpayment / early repayment are not clear. I have contacted HSBC's help line to no avail.

I intend to pay back the loan as soon as I can but use it during the current difficult times to survive as the loan does not cost my business anything for the first 12 months. The terms and conditions relating to the overpayment / early repayment suggest that I will be charged accrued interest for the overpayments / early settlement of the loan.

I have attached a picture of the terms and conditions. Please could anyone explain if I incur any interest if I let suppose pay off the loan in full in 11th month for example. Thanks

0

Comments

-

If you pay off the loan in the first year, you won't pay any interest on the loan - the government will be paying it1

-

Thank you for your prompt response. Doesn't "(b) you also pay us all accrued interest on the amount prepaid." mean the bank will charge interest if I repay the loan early?gt94sss2 said:If you pay off the loan in the first year, you won't pay any interest on the loan - the government will be paying it0 -

It is merely confirming that the monies paid off early are subject to interest until the day they are paid. In the first 12 months that means the government is liable for those interest payments, and after that you are.1

-

Thanks. Much appreciated.0

-

Finally, please confirm what would happen if say I pay back the loan after two years? My understanding now is that for the first year there are no payments due and no interest would be charged. First payment would be due on 13th month and would include interest charges. I would continue to make payments up until 23rd month and monthly payments would include interest charges. However when I settle the loan fully in 24th month I would not be charged any interest for remaining 4 years because the loan is settled. The settlement payment would not include any interest for remaining 4 years.

Is my understanding correct.

Thanks for your attention. I will look forward to your reply.

0 -

The reason the agreement is worded like this is that although the bank will receive the payment under the BBLS scheme for the first year's interest, this payment is technically made by the government to you and from you to the bank. It isn't paid (technically) by the govt to the bank on paper (though in practice it is).1

-

If you take the BBLS and clear the loan in month 23, you will only pay accrued interest up to month 23 (of which the first 12 months interest will have been covered by the Government). No interest liability for the remainder of the term - it will not work like some consumer 'buy-now-pay-later' deals.1

-

Thank you very much. This clarifies all the concerns I had.Grumpy_chap said:If you take the BBLS and clear the loan in month 23, you will only pay accrued interest up to month 23 (of which the first 12 months interest will have been covered by the Government). No interest liability for the remainder of the term - it will not work like some consumer 'buy-now-pay-later' deals.

0 -

Good morning, this is my first time posting anything on these forums, so my apologies if I'm not doing it quite right. I thought I would ask on this thread as it is to do with terms and conditions of a BBL.

I have applied for a BBL through Santander, and when reading through the agreement I noticed that it says that this loan is not covered by the Financial Services and Markets Act 2000 and so is not subject to the usual consumer protections under the Consumer Credit Act 1974. What exactly does this mean? I know it means i'm not protected, but what protection and how can I be at risk? Just want to fully understand what I am signing up for before agreeing.

Many thanks in advance for help with this.0 -

Broadly speaking it means you can't complain that they haven't offered alternatives or checked affordability or done any of the other things that are supposed to protect people from themselves.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards