We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Aprox £15k to invest.ISA + Stock & Shares ISA?

Comments

-

the attempts to stoke inflation being negative interest rates meaning more people will buy stocksMaxiRobriguez said:

Using the last five years of US stocks only is a very narrow window to justify that 2-5 years is "enough time"theselfishaltruist said:

Anything is better than the interest on a savings account. 2-5 years is enough time, considering your average mutual fund will go up about 6-7%. I don't believe there is a good chance of losing money. LOoking at the S&P 500 over the last five years shows increased by 50% from 2015 to today.grumiofoundation said:

As said above 2-5 years is a very short time period - decent chance you would end up having less money.Bobby_Bouche said:I have been reading for a few days and truth be told I am quite confused by ISA's (Stocks and Shares variant).

I have about £10k in a Halifax ISA cash presumably from previous tax years earning hardly anything and I have about £2-5K I'd like to invest in a stocks and shares ISA.

The money may be tied up for 2-5 years. as in you are willing to 'tie it up' for 2-5 years

As I am not clued up I'd prefer a Stocks and Shares ISA that is pre-picked as I'd not have enough knowledge to be able to choose myself.

I looked at Halifax and saw fees of £12 per year etc, and based on how little returns are these days that seems hardly worth the effort on such a small amount. You don't know what the return will be?

Ideally I'd like to sort my ISA out. What type of ISA?

Any help or advice would be greatly appreciated.

What are you planning to do with the money?

If for house purchase have you looked at lifetime ISA (cash)? 25% bonus on up to 4000 per year.

If for retirement probably pension or S and S LISA best.

Also, you can get a stocks and shares LISA, so you can invest in the market and still get the bonus. AJ Bell does one (I have one with them, although it's basically empty at the moment).

No offence, but I just don't think the evidence supports your view here. Investing is nearly always better than savings, especially over 5 years.

It might be, it might not be. Anyone who invested in the S&P500 in January 2006 (ie, 2 and a half years prior to the 2008 bear market) didn't see a positive capital return for six years.

Given we're about to see a seismic shift over the next 12-24 months of change in human behaviour, I'd suggest there's a strong case to argue the opposite to you. Prospect of sustained deflation is quite large, despite attempts to stoke inflation. Could result in significant losses over that time period.

Agree with other posters. If the money is needed in 2-5 years, it shouldn't be invested unless the money is only supplementing what could be achieved without it.0 -

Apologies If I did not say the intention. The £15k is money I have and do not really need to use it in the next 5-15 years etc. It's general savings and no actual use.eskbanker said:

You didn't really answer the question about your intentions, which are obviously your own business but 2-5 years is a fairly broad range and it isn't clear (to readers on here) what the significance of that period is, which could compromise recommendations.Bobby_Bouche said:

Thanks for replies.grumiofoundation said:What are you planning to do with the money?

I am over 40 so lifetime ISA is a no go. Money was ideally to go towards a house but I already have a deposit for that. I thought S and S isa might be good but did not realize needed longer than 5 years initially etc.

'Your average mutual fund' might increase by that sort of margin over the long term, but over a 2-5 year window could easily be negative (or more positive than 6-7% annually for that matter).theselfishaltruist said:

Anything is better than the interest on a savings account. 2-5 years is enough time, considering your average mutual fund will go up about 6-7%.

I have some other funds that will be used for a house purchase this year(or 2 depending on current housing market).

Many thanks to everyone who's chipped in.0 -

Maybe, maybe not.yellow1231231 said:

the attempts to stoke inflation being negative interest rates meaning more people will buy stocksMaxiRobriguez said:

Using the last five years of US stocks only is a very narrow window to justify that 2-5 years is "enough time"theselfishaltruist said:

Anything is better than the interest on a savings account. 2-5 years is enough time, considering your average mutual fund will go up about 6-7%. I don't believe there is a good chance of losing money. LOoking at the S&P 500 over the last five years shows increased by 50% from 2015 to today.grumiofoundation said:

As said above 2-5 years is a very short time period - decent chance you would end up having less money.Bobby_Bouche said:I have been reading for a few days and truth be told I am quite confused by ISA's (Stocks and Shares variant).

I have about £10k in a Halifax ISA cash presumably from previous tax years earning hardly anything and I have about £2-5K I'd like to invest in a stocks and shares ISA.

The money may be tied up for 2-5 years. as in you are willing to 'tie it up' for 2-5 years

As I am not clued up I'd prefer a Stocks and Shares ISA that is pre-picked as I'd not have enough knowledge to be able to choose myself.

I looked at Halifax and saw fees of £12 per year etc, and based on how little returns are these days that seems hardly worth the effort on such a small amount. You don't know what the return will be?

Ideally I'd like to sort my ISA out. What type of ISA?

Any help or advice would be greatly appreciated.

What are you planning to do with the money?

If for house purchase have you looked at lifetime ISA (cash)? 25% bonus on up to 4000 per year.

If for retirement probably pension or S and S LISA best.

Also, you can get a stocks and shares LISA, so you can invest in the market and still get the bonus. AJ Bell does one (I have one with them, although it's basically empty at the moment).

No offence, but I just don't think the evidence supports your view here. Investing is nearly always better than savings, especially over 5 years.

It might be, it might not be. Anyone who invested in the S&P500 in January 2006 (ie, 2 and a half years prior to the 2008 bear market) didn't see a positive capital return for six years.

Given we're about to see a seismic shift over the next 12-24 months of change in human behaviour, I'd suggest there's a strong case to argue the opposite to you. Prospect of sustained deflation is quite large, despite attempts to stoke inflation. Could result in significant losses over that time period.

Agree with other posters. If the money is needed in 2-5 years, it shouldn't be invested unless the money is only supplementing what could be achieved without it.

Anyone who is certain of what will happen is more than likely running a portfolio which is wildly more inefficient or risky than someone else who knows accepts limitations of their knowledge or uncertain and constructs a portfolio accordingly.1 -

you would agree lots of people are gong to look elsewhere if normal savings are low thats my only pointMaxiRobriguez said:

Maybe, maybe not.yellow1231231 said:

the attempts to stoke inflation being negative interest rates meaning more people will buy stocksMaxiRobriguez said:

Using the last five years of US stocks only is a very narrow window to justify that 2-5 years is "enough time"theselfishaltruist said:

Anything is better than the interest on a savings account. 2-5 years is enough time, considering your average mutual fund will go up about 6-7%. I don't believe there is a good chance of losing money. LOoking at the S&P 500 over the last five years shows increased by 50% from 2015 to today.grumiofoundation said:

As said above 2-5 years is a very short time period - decent chance you would end up having less money.Bobby_Bouche said:I have been reading for a few days and truth be told I am quite confused by ISA's (Stocks and Shares variant).

I have about £10k in a Halifax ISA cash presumably from previous tax years earning hardly anything and I have about £2-5K I'd like to invest in a stocks and shares ISA.

The money may be tied up for 2-5 years. as in you are willing to 'tie it up' for 2-5 years

As I am not clued up I'd prefer a Stocks and Shares ISA that is pre-picked as I'd not have enough knowledge to be able to choose myself.

I looked at Halifax and saw fees of £12 per year etc, and based on how little returns are these days that seems hardly worth the effort on such a small amount. You don't know what the return will be?

Ideally I'd like to sort my ISA out. What type of ISA?

Any help or advice would be greatly appreciated.

What are you planning to do with the money?

If for house purchase have you looked at lifetime ISA (cash)? 25% bonus on up to 4000 per year.

If for retirement probably pension or S and S LISA best.

Also, you can get a stocks and shares LISA, so you can invest in the market and still get the bonus. AJ Bell does one (I have one with them, although it's basically empty at the moment).

No offence, but I just don't think the evidence supports your view here. Investing is nearly always better than savings, especially over 5 years.

It might be, it might not be. Anyone who invested in the S&P500 in January 2006 (ie, 2 and a half years prior to the 2008 bear market) didn't see a positive capital return for six years.

Given we're about to see a seismic shift over the next 12-24 months of change in human behaviour, I'd suggest there's a strong case to argue the opposite to you. Prospect of sustained deflation is quite large, despite attempts to stoke inflation. Could result in significant losses over that time period.

Agree with other posters. If the money is needed in 2-5 years, it shouldn't be invested unless the money is only supplementing what could be achieved without it.

Anyone who is certain of what will happen is more than likely running a portfolio which is wildly more inefficient or risky than someone else who knows accepts limitations of their knowledge or uncertain and constructs a portfolio accordingly.0 -

theselfishaltruist said:Anything is better than the interest on a savings account not if you get back less than you put in (that COULD happen) . 2-5 years is likely enough time, considering your average mutual fund will is aiming to go up about 6-7%. I don't believe there is a good chance of losing money. Great - and your opinion has how much influence on world markets LOoking at the S&P 500 over the last five years shows increased by 50% from 2015 to today. unsurprisingly the best performing market in a long bull market has gone up a over 5 years - will the next 5 years be as good?

Also, you can get a stocks and shares LISA, so you can invest in the market and still get the bonus. AJ Bell does one (I have one with them, although it's basically empty at the moment).

No offence, but I just don't think the evidence supports your view here. I have no evidence, neither do you - thats the point Investing is nearly always better than savings, especially over 5 years - where did i say it wasn't?I think 2-5 years is a perfectly acceptable amount of time to invest money if you do it in the right places. see above re the actual impact your opinion hasAlso, I think with the pandemic, it might be a good time to invest. the FTSE is lower than is was at the moment, and so is the s&p500. Although, I think they will sink lower when the depression hits.. If/when that happens (and I cannot see any reason why it wont), that;s when you buy.

You don't seem to understand what risk actually means.

https://www.merriam-webster.com/dictionary/risk

Investing in the stock market always carries the RISK that you may not get back what you put in. You invest if you are willing to RISK this in return for greater returns. The longer you invest for, the lower the RISK of losing money.

No-one is saying don't invest (in fact most people on these forums would say the opposite) or that in 2-5 years you will definitely lose money, they are saying you have a much higher chance of losing money if you invest on a 5 year timescale compared to if you invest for 10 years, 15 years...

Can you guarantee in 2-5 years the OP will get back everything than you put in? The answer is no. Therefore if the OP could not afford/was not willing to RISK getting back less than they put in then a 5 year timescale could well end up being too short.

1 -

Personally, I think you could achieve similar results with cheaper fees just by opening an S&S ISA account with Vanguard on their website and choosing one of their Lifestrategy funds to invest in.649tom said:Hi all,

MY FIRST POST :-)))

I can recommend Numeg for a Stock and Shares ISA. I have chose the fully managed portfolio option with no fees for the first year. They invest your money globally across a broad spectrum of Exchange Traded Funds.

Check them out, they make investing simple and provide regular updates on the market via live conference calls that you can listen back to on youtube if you miss them. The app is also great.Think first of your goal, then make it happen!3 -

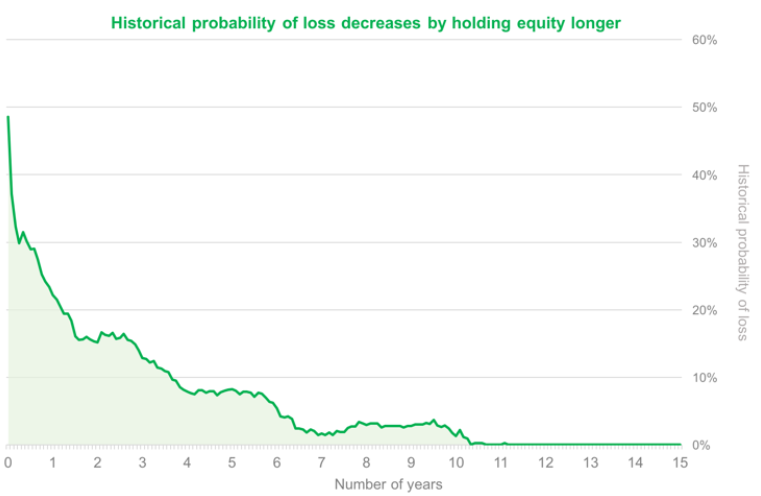

Well according to Nutmeg based on data from 1971 to 2018.....

0 -

Thank you to everyone who posted info on this topic. I've learned 1000% more than I knew a week ago.

I've read the comments here and other threads, as well as gone and read other information.

I think a managed s and s isa fund with mid risk is probably the way I will go for this tax year for me personally.

Many thanks.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards