We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Squeaky bum time!

Comments

-

This is my AJ Bell SIPP. I cannot find a similar analysis facility for my Hargreaves ISA unfortunately.LHW99 said:ffacoffipawb said:

The original strategy was to build a portfolio of investment trusts (because platform charges are capped) with a regular monthly income so that the dividend income could be drawn down to provide a pension income with the capital being left to grow in line with the dividend growth (as reasonably expected).cfw1994 said:

Yup....I bet many are questioning their choices this year, & plenty wringing their hands in angst.Deleted_User said:Tend to agree with DQ.

Perhaps a good time to do some reading. I am a big fan of Bernstein’s 4-book series on risk e.g. https://www.amazon.ca/Deep-Risk-History-Portfolio-Investing-ebook/dp/B00EV25GAM. Then re-evaluate your objectives and the overall policy. Then proceed. Making fundamental changes requires some learning and thinking. Everyone questions themselves and we all feel bad when portfolio underperforms but a bad day is usually the worst time to make fundamental changes.

You don’t mention amounts. A “fair bit of cash” perhaps means you have little need to draw on the investments for some time, should the markets dip and remain low for a while. That’s a good position to be in. If I’m brutally honest, I’m not sure what your original funds & strategy were, so take this with the proverbial seasoning.

For me, the logic is keep things low cost, broadly globally spread (the Lars Kroijer approach - I wimpier when I see people with a huge home bias - we are but 5-6% of GDP!). I also like some degree of risk on a certain percent of our funds (for growth & fun). In your shoes, perhaps an LS60 fund for 60-75% for that low cost element. Similar to the Global Equity Fund, although from what I see, that has slightly less track record. Not sure of the costs, but if we have a few years of low growth, I think containing them is key: every fraction of a percent in costs is a fraction of a percent you need your funds to grow at before breaking even....

For the growth and fun part, I suspect DQ is right suggestion you may have some overlap, but I can also get the “eggs and baskets” thinking behind it.

I always find it interesting that we all understand “Past performance of a particular fund manager tells us little about fund’s future performance”.....& yet that is often all that mere mortals have to go on. The fallout from Woodford indicates to me that many professionals don’t know much better either.....

For me, examining fact sheets to compare things is a useful exercise: did that around 15 or more years back, and the funds I changed to have served me well, with a few minor tweaks and adjustments along the way. Many will see me as naive. Working in IT & not the finance sector, as I do, I won’t argue with that....

My ISA, the same but with more ITs and smaller holdings thereof.

Both have come a cropper this year. However looking at how some individual FTSE 100 UK shares have performed I think I have come off lightly and grateful that I ditched HYP as a concept a few years ago.

I have enough cash outside pension for 5 years income (may as well use it as it is yielding naff all( but obviously want to make use of my tax free personal allowance as far as the pension income is concerned - use it or lose it! That does seem particularly UK heavy - we are overweight UK according to many, but only to around 1/2 the level you have. Also our US is around 2-3x yours. Otherwise we have a little more in Europe, and less in emerging Asia.There are headwinds everywhere just now, but I still feel I don't want to catch a falling knife, so although we are down still since the peak (but up considerably since the bottom) I have generally sat on my hands, except for a couple of small buy / sells which were semi-planned anyway.

That does seem particularly UK heavy - we are overweight UK according to many, but only to around 1/2 the level you have. Also our US is around 2-3x yours. Otherwise we have a little more in Europe, and less in emerging Asia.There are headwinds everywhere just now, but I still feel I don't want to catch a falling knife, so although we are down still since the peak (but up considerably since the bottom) I have generally sat on my hands, except for a couple of small buy / sells which were semi-planned anyway.

Probably best leave both alone while the COVID dust settles.0 -

ffacoffipawb said:The original strategy was to build a portfolio of investment trusts (because platform charges are capped) with a regular monthly income so that the dividend income could be drawn down to provide a pension income with the capital being left to grow in line with the dividend growth (as reasonably expected).

My ISA, the same but with more ITs and smaller holdings thereof.

Both have come a cropper this year. However looking at how some individual FTSE 100 UK shares have performed I think I have come off lightly and grateful that I ditched HYP as a concept a few years ago.

I have enough cash outside pension for 5 years income (may as well use it as it is yielding naff all( but obviously want to make use of my tax free personal allowance as far as the pension income is concerned - use it or lose it!If that was the original strategy, bailing out now at the bottom of the market may not be the best idea. For example, I would be really hesitant to crystallise heavy losses in the UK market now, only to reinvest in what is IMHO an overpriced global (mainly US) market.Surely the point of your strategy is that you are happy to ride out the volatility in share price knowing your IT's will continue to pay out dividends as they hopefully have built up cash reserves for just such an occasion, and the share prices will hopefully recover going forward (OEICs do not have this luxury and their dividend payments have been decimated). It's a bit like a buy-to-let landlord - what do you care if the housing market crashes and your house is worth half what you paid for it as long as the tenants keep coughing up £500/month in rent. Prices will recover at some point. I'm actually considering adding to my holding of CTY in my income portfolio as I find the current 6% dividend yield highly attractive and I have reasonable confidence it can be maintained, and even if it can't I don't expect it to stop completely.Our green credentials: 12kW Samsung ASHP for heating, 7.2kWp Solar (South facing), Tesla Powerwall 3 (13.5kWh), Net exporter0 -

Happy to do so but not sure if it will be helpful to you without describing my strategy (a long and boring subject). I stress that Mr DQ's aim is flexible drawdown and he can suspend withdrawals completely if the markets move against him. He can therefore afford to take higher risk. Performance is OK right now but his is a volatile portfolio and subject to large drops.ffacoffipawb said:Could you show your portfolio split by approx percentage, e.g. Fundsmith 10% etc?

Mr DQ's Racy Sub-Portfolio:

Core Funds (there are two simply because Mr DQ didn't want too much exposure to a single company). The first figure is the starting allocation in 2019. The second figure is the current allocation.

Vanguard FTSE Global All Cap 28.66% / 28.68%

L&G International Trust ex UK 28.66 / 29.16

Satellite Funds

Artemis US Smaller Companies 3.26 / 3.85

Baillie Gifford Shin Nippon 3.26 / 3.81

Fidelity Asian Values 1.63 / 1.32

Fidelity China Special Situations 2.77 / 3.22

Fidelity Index Europe ex UK 2.44 / 2.22

Fundsmith Equity 4.23 / 5.35

GAM Star Credit Opportunities 2.61 / 2.44

TB Amati UK Smaller Companies 2.61 / 2.61

RIT Capital Partners 2.61 / 2.14

Cash 17.26 / 15.20

Our consolidated portfolio is overweight UK and cash, and underweight bonds, but the UK features more in my (sub) portfolio (mostly a selection of VLS). The European Index Fund was included in Mr DQ's sub portfolio as I wanted to increase exposure to Europe across the consolidated portfolio and his HL SIPP (home of the satellites) was the most convenient platform from which to do so.

Note that the UK small cap fund has performed pretty well. The fund is up 12.35% since purchase in April last year.

The satellite portfolio is up 2.0% (1 mth) / 6.9% (3 mths) / 39.4% (6 mths) / 10.9% (1 yr).

Over the same periods the core portfolio (which includes the bulk of Mr DQ's wrapped cash) = -0.1% / 2.0% / 28.4% / 4.8%. The core funds are up a combined 12.76% since purchase in May 2019. As expected the high cash has been a drag but it was worth the peace of mind it gave in March.

I will likely reduce the allocation to Fundsmith, and marginally increase the allocation to China and Asia, when I rebalance later this year.

Our Consolidated Portfolio Allocations (at July):

Equities: 75.16%

Fixed Interest: 7.43

Money Market: 0.41

Cash: 16.99

USA: 41.03

UK: 15.28

Canada: 1.22

Pacific Asia: 3.70

Japan: 7.33

Global: 13.37

Europe xUK: 10.47

Emerging: 4.14

China: 2.96

3 -

Thanks for this, interesting and helpful.DairyQueen said:

Happy to do so but not sure if it will be helpful to you without describing my strategy (a long and boring subject). I stress that Mr DQ's aim is flexible drawdown and he can suspend withdrawals completely if the markets move against him. He can therefore afford to take higher risk. Performance is OK right now but his is a volatile portfolio and subject to large drops.ffacoffipawb said:Could you show your portfolio split by approx percentage, e.g. Fundsmith 10% etc?

Mr DQ's Racy Sub-Portfolio:

Core Funds (there are two simply because Mr DQ didn't want too much exposure to a single company). The first figure is the starting allocation in 2019. The second figure is the current allocation.

Vanguard FTSE Global All Cap 28.66% / 28.68%

L&G International Trust ex UK 28.66 / 29.16

Satellite Funds

Artemis US Smaller Companies 3.26 / 3.85

Baillie Gifford Shin Nippon 3.26 / 3.81

Fidelity Asian Values 1.63 / 1.32

Fidelity China Special Situations 2.77 / 3.22

Fidelity Index Europe ex UK 2.44 / 2.22

Fundsmith Equity 4.23 / 5.35

GAM Star Credit Opportunities 2.61 / 2.44

TB Amati UK Smaller Companies 2.61 / 2.61

RIT Capital Partners 2.61 / 2.14

Cash 17.26 / 15.20

Our consolidated portfolio is overweight UK and cash, and underweight bonds, but the UK features more in my (sub) portfolio (mostly a selection of VLS). The European Index Fund was included in Mr DQ's sub portfolio as I wanted to increase exposure to Europe across the consolidated portfolio and his HL SIPP (home of the satellites) was the most convenient platform from which to do so.

Note that the UK small cap fund has performed pretty well. The fund is up 12.35% since purchase in April last year.

The satellite portfolio is up 2.0% (1 mth) / 6.9% (3 mths) / 39.4% (6 mths) / 10.9% (1 yr).

Over the same periods the core portfolio (which includes the bulk of Mr DQ's wrapped cash) = -0.1% / 2.0% / 28.4% / 4.8%. The core funds are up a combined 12.76% since purchase in May 2019. As expected the high cash has been a drag but it was worth the peace of mind it gave in March.

I will likely reduce the allocation to Fundsmith, and marginally increase the allocation to China and Asia, when I rebalance later this year.

Our Consolidated Portfolio Allocations (at July):

Equities: 75.16%

Fixed Interest: 7.43

Money Market: 0.41

Cash: 16.99

USA: 41.03

UK: 15.28

Canada: 1.22

Pacific Asia: 3.70

Japan: 7.33

Global: 13.37

Europe xUK: 10.47

Emerging: 4.14

China: 2.960 -

As i am not sure what to do, it is best to do nothing.NedS said:ffacoffipawb said:The original strategy was to build a portfolio of investment trusts (because platform charges are capped) with a regular monthly income so that the dividend income could be drawn down to provide a pension income with the capital being left to grow in line with the dividend growth (as reasonably expected).

My ISA, the same but with more ITs and smaller holdings thereof.

Both have come a cropper this year. However looking at how some individual FTSE 100 UK shares have performed I think I have come off lightly and grateful that I ditched HYP as a concept a few years ago.

I have enough cash outside pension for 5 years income (may as well use it as it is yielding naff all( but obviously want to make use of my tax free personal allowance as far as the pension income is concerned - use it or lose it!If that was the original strategy, bailing out now at the bottom of the market may not be the best idea. For example, I would be really hesitant to crystallise heavy losses in the UK market now, only to reinvest in what is IMHO an overpriced global (mainly US) market.Surely the point of your strategy is that you are happy to ride out the volatility in share price knowing your IT's will continue to pay out dividends as they hopefully have built up cash reserves for just such an occasion, and the share prices will hopefully recover going forward (OEICs do not have this luxury and their dividend payments have been decimated). It's a bit like a buy-to-let landlord - what do you care if the housing market crashes and your house is worth half what you paid for it as long as the tenants keep coughing up £500/month in rent. Prices will recover at some point. I'm actually considering adding to my holding of CTY in my income portfolio as I find the current 6% dividend yield highly attractive and I have reasonable confidence it can be maintained, and even if it can't I don't expect it to stop completely.") 0

0 -

Interesting, thanks.ffacoffipawb said:

The original strategy was to build a portfolio of investment trusts (because platform charges are capped) with a regular monthly income so that the dividend income could be drawn down to provide a pension income with the capital being left to grow in line with the dividend growth (as reasonably expected).cfw1994 said:

Yup....I bet many are questioning their choices this year, & plenty wringing their hands in angst.Deleted_User said:Tend to agree with DQ.

Perhaps a good time to do some reading. I am a big fan of Bernstein’s 4-book series on risk e.g. https://www.amazon.ca/Deep-Risk-History-Portfolio-Investing-ebook/dp/B00EV25GAM. Then re-evaluate your objectives and the overall policy. Then proceed. Making fundamental changes requires some learning and thinking. Everyone questions themselves and we all feel bad when portfolio underperforms but a bad day is usually the worst time to make fundamental changes.

You don’t mention amounts. A “fair bit of cash” perhaps means you have little need to draw on the investments for some time, should the markets dip and remain low for a while. That’s a good position to be in. If I’m brutally honest, I’m not sure what your original funds & strategy were, so take this with the proverbial seasoning.

For me, the logic is keep things low cost, broadly globally spread (the Lars Kroijer approach - I wimpier when I see people with a huge home bias - we are but 5-6% of GDP!). I also like some degree of risk on a certain percent of our funds (for growth & fun). In your shoes, perhaps an LS60 fund for 60-75% for that low cost element. Similar to the Global Equity Fund, although from what I see, that has slightly less track record. Not sure of the costs, but if we have a few years of low growth, I think containing them is key: every fraction of a percent in costs is a fraction of a percent you need your funds to grow at before breaking even....

For the growth and fun part, I suspect DQ is right suggestion you may have some overlap, but I can also get the “eggs and baskets” thinking behind it.

I always find it interesting that we all understand “Past performance of a particular fund manager tells us little about fund’s future performance”.....& yet that is often all that mere mortals have to go on. The fallout from Woodford indicates to me that many professionals don’t know much better either.....

For me, examining fact sheets to compare things is a useful exercise: did that around 15 or more years back, and the funds I changed to have served me well, with a few minor tweaks and adjustments along the way. Many will see me as naive. Working in IT & not the finance sector, as I do, I won’t argue with that....

My ISA, the same but with more ITs and smaller holdings thereof.

Both have come a cropper this year. However looking at how some individual FTSE 100 UK shares have performed I think I have come off lightly and grateful that I ditched HYP as a concept a few years ago.

I have enough cash outside pension for 5 years income (may as well use it as it is yielding naff all( but obviously want to make use of my tax free personal allowance as far as the pension income is concerned - use it or lose it!

As mentioned, I understand many have a large “home bias”, but it still makes me wonder why, when the U.K. is so small on the global stage. Different views, I guess. Of course many companies there will be global operators, so it is not as clear cut as the pictures might paint!

I understand why DQ feels the US is overweight/overpriced, but I personally would not bet against it.

Yes, we are in for a rocky road in the months ahead, but having worked for US companies for almost 30 years, I still have some faith in their development and business methods.

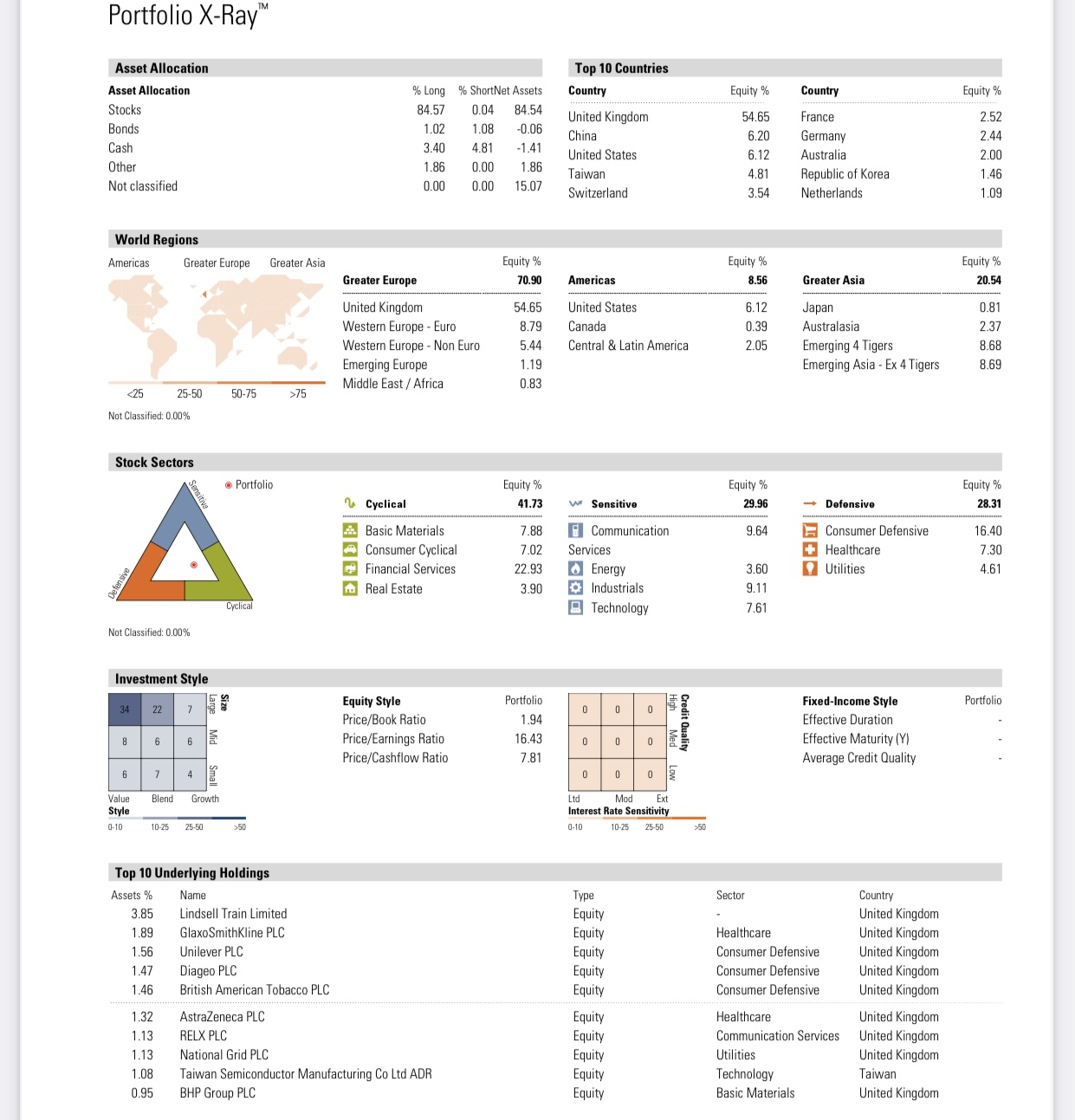

I am a simple being, with no deep portfolio x-rays into where we invest...but it is reasonably well spread. If you have no need to access the underlying money, I feel that the cycle of things will pick up well within your 5 year cash-holding timeframe. If I’m wrong, it’s time to invest in beans, water and shotguns!Plan for tomorrow, enjoy today!0 -

I'd not heard of HYP - it looks interesting and perfectly plausible. (There's an explainer here: https://www.stockopedia.com/content/high-yield-portfolio-what-is-hyp-investing-67857/).

I took the opposite view and decided that I wanted to be out of the UK (too many headwinds, too many loss-making banks) and in general to avoid high yielding stocks or anything labelled "income" because it risked compromising long term growth for regular dividends. Instead, I've gone with stuff I've held for ages (ATST, PNL, RCP, HGT, Fundsmith, SMT) and added some other bits that seemed like a good idea at the time (PHI, BGS, AVI). The last 12 months have been modestly positive on the whole (> 10%), so I'm not complaining. I can't say that my picks (mostly Investment Trusts) have been driven by any more developed strategy than that, so I realise I've been lucky. I'm planning a gradual move into global index trackers (SWDA, VWRL) for the core and some interesting stuff around the edges, but I'm at the start of that process and it will take some time.

I'm planning to retire next year and start drawdown, selling once or twice a year (undecided) to keep transaction costs down. It all seems much more serious once you realise that the plan has got to work and that there's no other income going to land in the bank account short of accepting defeat and heading back to work (I'm 59, so no state pension for a few years yet).

2 -

Use the dividend income generated to start to diversify your portfolio. Investors constantly search for maximum performance when it's optimal performance that counts. Holding a high % in equities will result in a highly correlated portfolio. Alternative investments should form a reasonable % of ones portfolio.ffacoffipawb said:

As i am not sure what to do, it is best to do nothing.NedS said:ffacoffipawb said:The original strategy was to build a portfolio of investment trusts (because platform charges are capped) with a regular monthly income so that the dividend income could be drawn down to provide a pension income with the capital being left to grow in line with the dividend growth (as reasonably expected).

My ISA, the same but with more ITs and smaller holdings thereof.

Both have come a cropper this year. However looking at how some individual FTSE 100 UK shares have performed I think I have come off lightly and grateful that I ditched HYP as a concept a few years ago.

I have enough cash outside pension for 5 years income (may as well use it as it is yielding naff all( but obviously want to make use of my tax free personal allowance as far as the pension income is concerned - use it or lose it!If that was the original strategy, bailing out now at the bottom of the market may not be the best idea. For example, I would be really hesitant to crystallise heavy losses in the UK market now, only to reinvest in what is IMHO an overpriced global (mainly US) market.Surely the point of your strategy is that you are happy to ride out the volatility in share price knowing your IT's will continue to pay out dividends as they hopefully have built up cash reserves for just such an occasion, and the share prices will hopefully recover going forward (OEICs do not have this luxury and their dividend payments have been decimated). It's a bit like a buy-to-let landlord - what do you care if the housing market crashes and your house is worth half what you paid for it as long as the tenants keep coughing up £500/month in rent. Prices will recover at some point. I'm actually considering adding to my holding of CTY in my income portfolio as I find the current 6% dividend yield highly attractive and I have reasonable confidence it can be maintained, and even if it can't I don't expect it to stop completely.0 -

I would be very careful about anything “alternative”. Requires experience and deep understanding of a whole range of issues like liquidity and all the hidden costs. Some instruments are very complicated and require you to read and understand a lot of small print.0

-

Only equities (investment trusts / OEICs) and cash for me. Dont see much value in bonds.Deleted_User said:I would be very careful about anything “alternative”. Requires experience and deep understanding of a whole range of issues like liquidity and all the hidden costs. Some instruments are very complicated and require you to read and understand a lot of small print.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards