We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Interest rates at historical lows, housing prices through the roof, wages stagnant and Brexit.

Comments

-

I wonder if the great housing ponzi scheme is now 'too big to fail'? If prices reverted to historic price/earnings ratios it would be game over!

No doubt the governbankment would find some more wheezes to keep the plates spinning?Funnily, i've been pondering a small Caddy sized van to facilitate a side project i'm going to work on. I havent seen much movement yet, but in theory markets like pickups and vans are likely to be hit by the upcoming downturn.Would be interesting to hear if anyone has direct experience?Why? So you can argue with them?0 -

CreditCardChris wrote: »You were charged 14% interest to buy a house which is now worth 500% - 1000% more than it was when you probably bought it? The good old days indeed.

Yes but wages then were perhaps 1/5th of what they are now.0 -

I wonder if the great housing ponzi scheme is now 'too big to fail'? If prices reverted to historic price/earnings ratios it would be game over!

No doubt the governbankment would find some more wheezes to keep the plates spinning?

There is no great Ponzi scheme. The price/earnings ratio hasnt changed. The difference is that now earnings are for 2 people. Prior to the 1980s in middle class families (the people who could afford to buy a house) the wife often did not work as running a house and looking after the children was a full time job. Those wives who did work were usually part time and/or low paid.0 -

-

There is no great Ponzi scheme. The price/earnings ratio hasnt changed. The difference is that now earnings are for 2 people. Prior to the 1980s in middle class families (the people who could afford to buy a house) the wife often did not work as running a house and looking after the children was a full time job. Those wives who did work were usually part time and/or low paid.

It's probably not a Ponzi scheme, not in the literal sense anyway, but the price to earnings ratio absolutely has changed.

If we lived in 'sensible' times with interest rates at say 5%, then people would be paying 7% on a mortgage, that would be unaffordable for a large number of people. That isn't the double figures often quoted but would still lead to a housing crisis and probable collapse. So no matter what is said about emergency interest rates having persisted for a decade and the economy needing near zero rates to grow, or at least survive, the main political reason that rates couldn't be increased is just down to the repossessions it would generate.

In the eighties, and back to the sixties, many people who weren't 'middle class' bought their own homes, and women have always worked. They might have worked fewer hours but for many families the extreme cost of childcare now wipes out a large chunk of of a second wage in any case.0 -

CreditCardChris wrote: »You were charged 14% interest to buy a house which is now worth 500% - 1000% more than it was when you probably bought it? The good old days indeed.

..not sure where you get those figures from?..our house cost £65k and in today's market would be about £140k / £150k at a push...you need to consider the area. Living in London is a lifestyle choice...higher wages but higher costs.

Around these parts property prices have been pretty static for almost 10yrs.

I am not denying that house purchasing for the younger generation is more difficult these days as can be seen from the ratio between salaries and property cost.

I would also consider a salary of £38k to be above average and rather good. Also note that you can't really expect a high interest rate for your savings and at the same time a low rate for your mortgage.0 -

I would also consider a salary of £38k to be above average and rather good.

So would I but guess what? The highest mortgage I can get is around ~£170,000 which pretty much excludes me from the entire south. https://i.gyazo.com/334d694ebafee6d6ad73eb6429234e6c.png

Sure I can probably get a 1 bedroom flat for £200,000 but that's a horrible reality to accept as I currently rent a flat and have to put up with noisy neighbours, banging of doors, babies crying and just general noise which travels through the building.

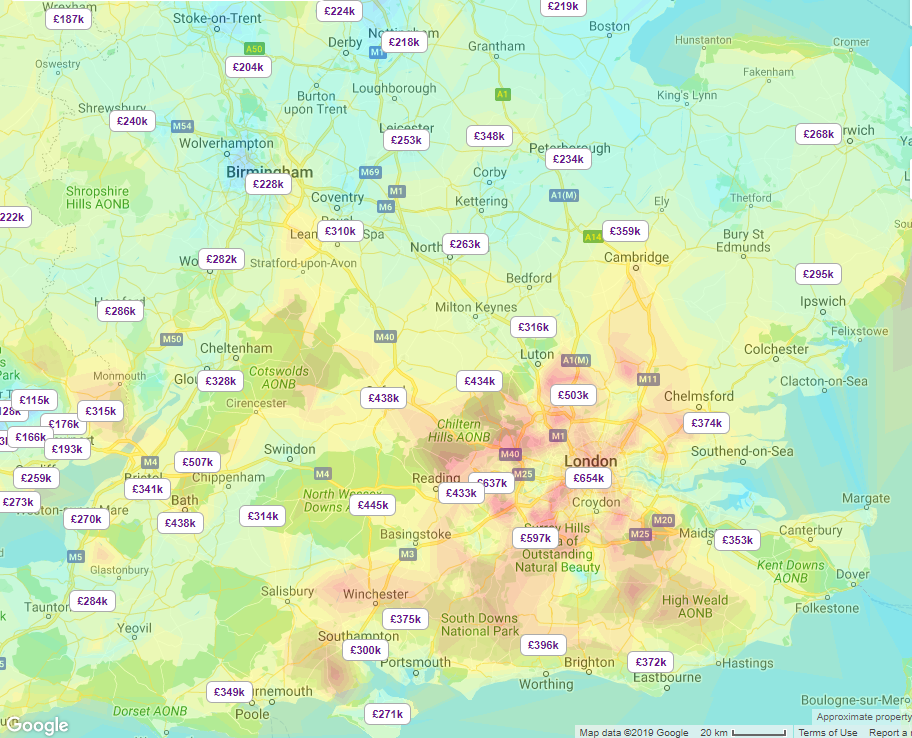

So it annoys me when everyone mentions London... It's not just London which is unaffordable, it's pretty much the entire south of the country.

If this was 2000 I'd be able to get a 4 bedroom detached house in outer London for £200,000. it's crazy!0 -

CreditCardChris wrote: »So would I but guess what? The highest mortgage I can get is around ~£170,000 which pretty much excludes me from the entire south. https://i.gyazo.com/334d694ebafee6d6ad73eb6429234e6c.png

Sure I can probably get a 1 bedroom flat for £200,000 but that's a horrible reality to accept as I currently rent a flat and have to put up with noisy neighbours, banging of doors, babies crying and just general noise which travels through the building.

So it annoys me when everyone mentions London... It's not just London which is unaffordable, it's pretty much the entire south of the country.

If this was 2000 I'd be able to get a 4 bedroom detached house in outer London for £200,000. it's crazy!

You also wouldn't be earning 40k a year. O and the horrible reality you describe is just life. I am depending on which paper you read on the cusp of being a millennial. I bought a pokey one bedroom shared ownership flat in 2001 that was mouldy . I owned 40 % of it so couldn't even afford a whole flat. (and I live in reading so not even London prices). I saved and overpayed and eventually moved up to a 2 bed terrace after 4 years and sold that at a loss 7 years later during the financial crisis. I bought the house I live in now which is a 4 bed semi in reading. I could 'afford' a nice detached house, most people on my salary are probably buying houses twice the value of mine but I choose to cut my cloth accordingly so I can invest and have wealth rather than a big showy house and a massive mortgage and stress

Methinks you have unrealistic expectations of what your starter home will be. Save up. Get started. In a few years time you'll wonder what all the fuss is about. Or don't and rent and invest instead0 -

CreditCardChris wrote: »And house prices were 1/10th of what they are now. Ergo house prices are 5x more expensive in relation to wages today than they were when you bought your house.

What don't you understand?

I suggest you rethink your maths. If wages have gone up 5-fold and house prices have gone up 10 times, then house prices are twice as expensive in relation to wages as they were. This can be simply explained by the fact that more women work now, are able to get decent salaries, and do not give up their careers when they have children. In the past mortgages were largely based on the man's wages, now they are based on joint wages. As twice as much money is available market economics ensures that house prices will rise to use it. Tough on singles who are priced out of the market, but then they did not usually buy a house in the past either but lived at home or rented until they got married.

Clearly house prices are affordable now. If they werent large numbers of houses would be standing empty. The market ensures that the number of people who can afford to buy a house approximately equals the number of houses available.0 -

Its a shame you can buy houses with self pity or the op could become a property tycoon.

I bought my flat in the south east last year, £11k deposit, £101k mortgage, whilst earning £22k. Its tiny, had no heating and no shower. But it got me on the property ladder and im paying my mortgage, not someone elses.

Unlike the op im very excited for the future and there has definitely never been a better time to be young. Have fun in Canada.0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards