We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

It's time to start digging up those Squirrelled Nuts!!!!

Comments

-

Possibly, either way it’s 4 years or 6 years. I’m enjoying my PT job. So if my health or something else happens then it’s an option to go at 60.pensionpawn said:

Retire earlier?L9XSS said:Moved my SIPP portfolio to cash in early November 2021.......just a hunch.....not trying to time the market, but did avoid the falls of 10/15/20% that some have felt. As interest rates rose so did the interest on my cash in my SIPP. I have moved about 40% back into funds and EFTs and will drip feed more, however I will leave 30% in cash in this SIPP whilst I’m getting a 3.2% rate. Continuing to work PT paying into work pension and adding £300 plus HMRC uplift into my SIPP. Mortgage is paid off. At 56 my income is 23k pa, At 60 my income will be around 43k p/a (DB pension plus PT work). At 62 retire. Unearned income should be around 40k p/a.

Problem might be spending it, due to years of saving and overpaying mortgage.1 -

For what its worth-my two penneth. Old habits do die hard. A "save before you buy" upbringing, taking the advice off here and from others, having made good DB provision and always seeking out the best deal has meant we are in a very fortunate position of circa £80k per annum from our pensions (me at 57 (firstly a SIPP and LGPS when I take at 60) and OH at 59 - my OH got out on a redundancy package last year at 58) with invested savings of £650k and no mortgage and state pensions still to come ! .

I did earn £24k from 34 days consultancy this year (which I sort of enjoyed doing even though it was largely unplanned but have decided I am not going to do as much this year or any at all so I get more structured in divesting my time better elsewhere as my wife has !!). In my head I need to spend any income earned on something to justify working so we have gone OTT and booked the Maldives next Xmas (but still looked for the cashback deals and best deal) and agreed to get new golf clubs for both of us this coming March (likely £5k when normally I scour e bay where I have found some real gems and get the buzz from finding these). Part of retirement plans was to give us the time to travel extensively so we are off to Thailand for 9 weeks next week although without our golf it would work almost as cheap as living at home !! as again found some great deals where to stay on line and with good knowledge of the areas we are visiting

We do have a plan to start decumilating which I appreciate is a very nice position to be in which I have satisfied myself we can afford to do (after checking and rechecking spreadsheets) but we do need to start spending. We could spend a lump of the savings to move to a better postcode but struggling to justify that as we like where we live so looks like we may just stay put and spend £100k plus upgrading accepting it is for us rather than adding any massive value (another alien concept) and instead use our available funds to see the world whilst fit and able whilst having what we want within reason.

I have to admit I am struggling with this concept as it is alien to me to spend so freely after 40 plus years of "not going without but not splurging" but I have to remember this is what we worked so hard for and that we only get one life, I look at my parents who are in their late 80's with failing health and who worry about future care bills whilst sitting on accumulating savings and in a property that I have no need to inherit my share of. So my New Years resolution is to live for the moment, not feel I should justify leaving work earlier than most and "spend, spend, spend" but always with one eye on a good cashback or sale deal") 7

7 -

Hi @L9XSS - if you don’t mind me asking, what SIPP “investment” yields 3.2% on cash? Of the various cash funds available to me in my employers Pension Plan, none are close to that ? - Thank you.L9XSS said:Moved my SIPP portfolio to cash in early November 2021.......just a hunch.....not trying to time the market, but did avoid the falls of 10/15/20% that some have felt. As interest rates rose so did the interest on my cash in my SIPP. I have moved about 40% back into funds and EFTs and will drip feed more, however I will leave 30% in cash in this SIPP whilst I’m getting a 3.2% rate. Continuing to work PT paying into work pension and adding £300 plus HMRC uplift into my SIPP. Mortgage is paid off. At 56 my income is 23k pa, At 60 my income will be around 43k p/a (DB pension plus PT work). At 62 retire. Unearned income should be around 40k p/a.

Problem might be spending it, due to years of saving and overpaying mortgage.0 -

Probably not the answer you are looking for, but short dated UK gilts (2 years) are currently yielding 3.5%. These may not be available to purchase individually in a work place pension though and buying a short dated UK gilt fund does not give the same guaranteed return.theblueflash said:

Hi @L9XSS - if you don’t mind me asking, what SIPP “investment” yields 3.2% on cash? Of the various cash funds available to me in my employers Pension Plan, none are close to that ? - Thank you.L9XSS said:Moved my SIPP portfolio to cash in early November 2021.......just a hunch.....not trying to time the market, but did avoid the falls of 10/15/20% that some have felt. As interest rates rose so did the interest on my cash in my SIPP. I have moved about 40% back into funds and EFTs and will drip feed more, however I will leave 30% in cash in this SIPP whilst I’m getting a 3.2% rate. Continuing to work PT paying into work pension and adding £300 plus HMRC uplift into my SIPP. Mortgage is paid off. At 56 my income is 23k pa, At 60 my income will be around 43k p/a (DB pension plus PT work). At 62 retire. Unearned income should be around 40k p/a.

Problem might be spending it, due to years of saving and overpaying mortgage.

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.1 -

Cater Allen have a 24 month fixed rate deposit account for pensions paying 4%, although it may not be available in a workplace pension.theblueflash said:

Hi @L9XSS - if you don’t mind me asking, what SIPP “investment” yields 3.2% on cash? Of the various cash funds available to me in my employers Pension Plan, none are close to that ? - Thank you.L9XSS said:Moved my SIPP portfolio to cash in early November 2021.......just a hunch.....not trying to time the market, but did avoid the falls of 10/15/20% that some have felt. As interest rates rose so did the interest on my cash in my SIPP. I have moved about 40% back into funds and EFTs and will drip feed more, however I will leave 30% in cash in this SIPP whilst I’m getting a 3.2% rate. Continuing to work PT paying into work pension and adding £300 plus HMRC uplift into my SIPP. Mortgage is paid off. At 56 my income is 23k pa, At 60 my income will be around 43k p/a (DB pension plus PT work). At 62 retire. Unearned income should be around 40k p/a.

Problem might be spending it, due to years of saving and overpaying mortgage.

https://www.caterallen.co.uk/accounts/fixed-term-deposit-account-for-pensions/pensions

2 -

Hi @theblueflash my Main SIPP is with Vanguard, it’s a personal plan and not a company pension. I have a workplace pension with NEST from my PT employer. Interest is credited to my Vanguard pension monthly (I’m not in drawdown and the monthly interest is just to the cash portion of my pension). I have two other smaller SIPPs with AJBell and HL, afaik they do not pay interest on cash reserves in a pension.1

-

HL do. Modest amounts, but they do pay something.....L9XSS said:Hi @theblueflash my Main SIPP is with Vanguard, it’s a personal plan and not a company pension. I have a workplace pension with NEST from my PT employer. Interest is credited to my Vanguard pension monthly (I’m not in drawdown and the monthly interest is just to the cash portion of my pension). I have two other smaller SIPPs with AJBell and HL, afaik they do not pay interest on cash reserves in a pension.1 -

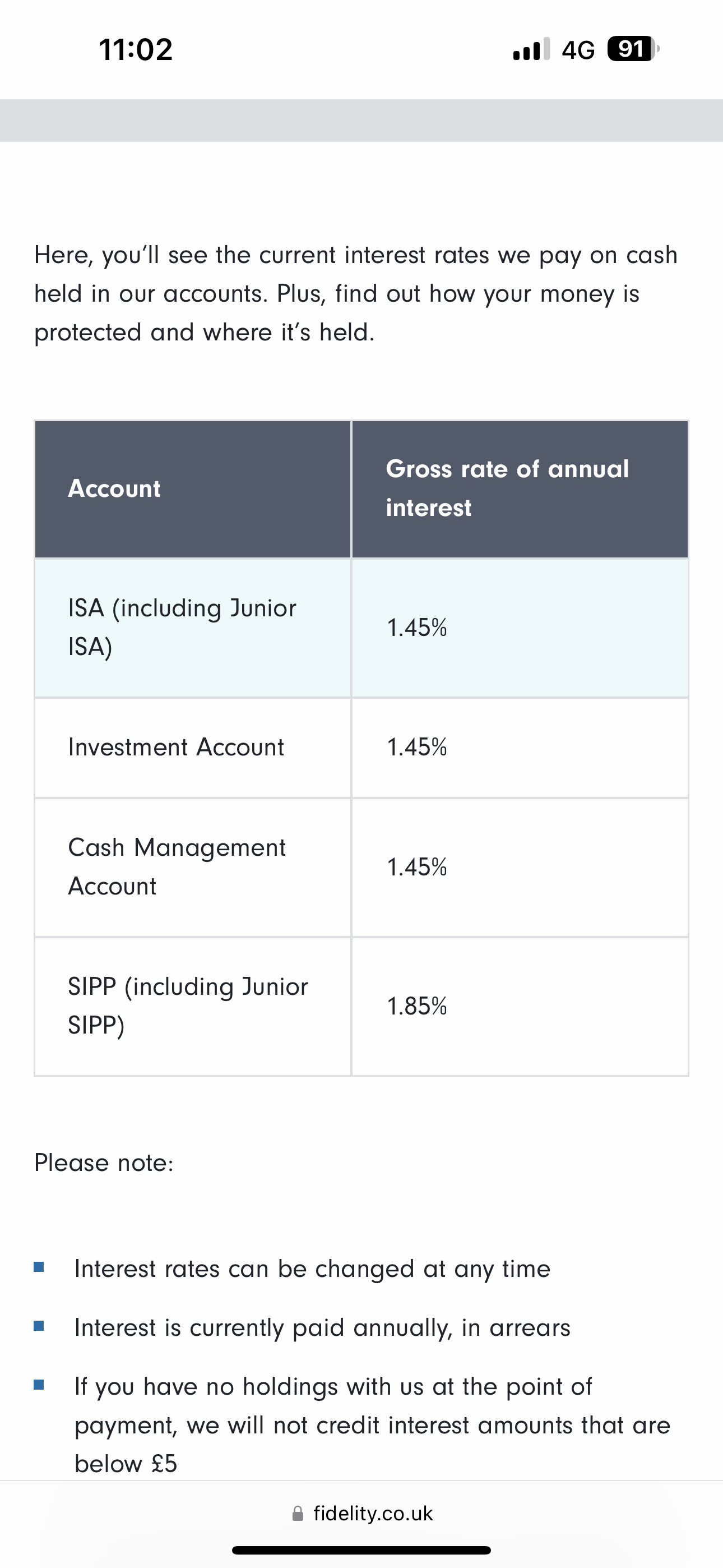

Fidelity are paying interest on cash held in Sipps

1 -

And a bit more next week, 1.7%+ for SIPPs https://www.hl.co.uk/charges-and-interest-ratesNebulous2 said:

HL do. Modest amounts, but they do pay something.....L9XSS said:Hi @theblueflash my Main SIPP is with Vanguard, it’s a personal plan and not a company pension. I have a workplace pension with NEST from my PT employer. Interest is credited to my Vanguard pension monthly (I’m not in drawdown and the monthly interest is just to the cash portion of my pension). I have two other smaller SIPPs with AJBell and HL, afaik they do not pay interest on cash reserves in a pension.

3 -

Prompted by another thread, I'd just add that overall we're at 64% Equities, 27% Other (bonds etc) and 9% cash.

How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards