We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

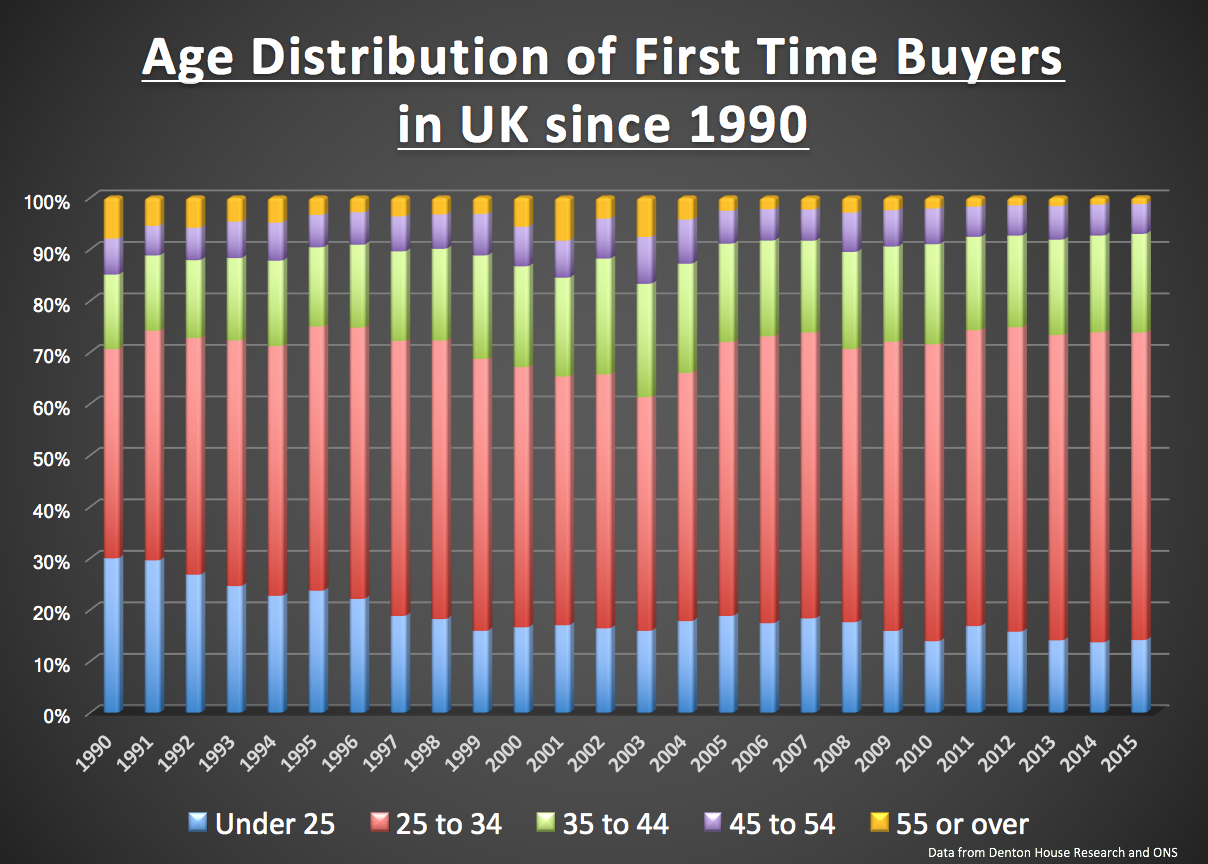

Where have all the 20 something’s gone?

Comments

-

we bought our first home on a single income, having saved hard, lived separately with our parents and didn`t have anything but second hand furniture and a new mattress when we married. We didn`t look around that much, didn`t look for that `feeling` when looking for a house. A house was simply a place to live and as long as it was decent and in a decent ie not rough area, then it did us. We were limited by how much x salary we could borrow. Different expectations in those days and different ethos re saving and spending

We bought a house four years ago and that was pretty much our situation too, although we didn't have the benefit of being able to live with parents and save. Our mortgage is based solely on my income as my partner is self-employed - he does make money but neither of us felt comfortable taking on a mortgage that we couldn't comfortably pay on just one income because of the erratic nature of his earnings, which are generally paid quarterly. It is still possible to do this - well it was four years ago, and I wouldn't say I was particularly well paid - but you do have to adjust your expectations and be realistic about what you can afford and where you can afford to live. The whole housing 'industry' peddles this ridiculous idea of 'forever homes' and 'dream homes' that does no-one any good (well except those making a profit from it), and leads to people taking on far more debt than they should.0 -

moneyistooshorttomention wrote: »Single people have always struggled unless well-paid or in a very cheap area. Welcome to our world.

You'll understand if I'm not that sympathetic - as no-one sympathised with us.

As a single person in 1988, age 26, I bought my first house. Ordinary worker, I don't think ordinary workers could do that with the high prices today.

I sold it after my divorce, just before house prices rocketed; I managed to buy my house last year, due to a windfall.0 -

0

0 -

40 years ago the majority of people bought with a single income anyway. Women didnt generally have full time careers. My dad bought our childhood home on a single income just before I was born he was a 24 year electrician!

I've never had a career. I've just had jobs personally.

Basically the way things went for a person with a job (paid a "womans wage" - rather than a "mans wage" - it was the 1970s after all) was that I had noticed there seemed to be problems for a woman trying to get a mortgage on her own.

Now those problems went at last at around my mid-20s and I promptly decided to buy a house on my own (having realised Mr Right seemed to be taking his time about turning up - which he never did).

At around the same time the problems married women had had having their income taken into account for mortgages too also went - which was promptly followed by starter houses in my dear area promptly going up from affordable for me (but I was going to have obstacles put in my way getting a mortgage) to unaffordable for me (because the 2nd income in a couple was being counted into the equation more).

So that worked out well for married women - but badly for singles.

Believe me - I gave some serious thought to doing what I saw a lot of other people doing (ie marrying "Mr Someone Else"). But the thought of the divorce I'd then have if I subsequently met Mr Right (as I knew I'd still be looking for him - so unfaithful) put me off that thought:rotfl:

A lot of how affordable (or otherwise) things were revolved around area of the country one was in (even then) and hence one had to be either married or well-paid in my area. I did contemplate moving to North of England to get a starter. Later life saw me having to move to West Wales to get the "detached with garden" house.0 -

The house that I bought in my middle 20s in the northwest is as affordable now to a single person doing the same job as I was doing as it was when I bought it. So no change there.

On the other hand in the 1970s London property was too expensive for the average single person to buy on their own without help from their parents or having a property to sell in another part of the country. Interest rates were higher then too.

I think you will find that a lot more 20 somethings could buy a house if they didn't have a car and used public transport or walked to work, had the cheapest bottom of the range phone used the internet at their local library, didn't eat out or have takeaways, didn't buy coffee or drinks out and basically didn't buy anything that they didn't actually need. Years ago buying somewhere to live was treated with more importance than anything else. So you wouldn't rent a 1 bed flat if you could house share etc.0 -

40 years ago the majority of people bought with a single income anyway. Women didnt generally have full time careers. My dad bought our childhood home on a single income just before I was born he was a 24 year electrician!

A single woman generally wouldn't have had the same earning power as a man 40 years ago though. They weren't generally encouraged to go to uni or into well paid trades/careers. Even in the 70s/80s and I'd say the 90s to be honest it was still expected that women would inevitably get married and then their man would take care of the money!0 -

So I’ve got a topic I’d like to discuss.

As others have said, there's a place for this sort of post.

However, to save everyone bother, like Godwin's Law, these discussions inevitably end like this:

https://www.youtube.com/watch?v=ue7wM0QC5LE

WARNING: Contains scenes of extreme smoking.0 -

The house that I bought in my middle 20s in the northwest is as affordable now to a single person doing the same job as I was doing as it was when I bought it. So no change there.

Are you sure? What are the figures? Because the place I bought only a decade ago in the North West would be nowhere near affordable now for somebody in the same job.0 -

Red-Squirrel wrote: »Are you sure? What are the figures? Because the place I bought only a decade ago in the North West would be nowhere near affordable now for somebody in the same job.

Round the corner from this one http://www.rightmove.co.uk/property-for-sale/property-53767230.html but not in quite such a nice area.

I paid £18950 for mine new and my deposit was £950. I seem to remember that I was earning about £6000 a year. So I borrowed around 3 times my salary. Now it would be worth about £100k so you with a 10% deposit and salary that is now £30k there is no difference. In fact it would be cheaper to buy now because the interest rates are lower so the monthly mortgage repayments would be less.0 -

I’m going to disagree with most of the posts here

I happen to live in a “cheap” part of the UK and house prices around the area are mostly reasonable and what I would say were in line with earnings.

Me and my partner bought 4 years ago, aged 24 on very modest incomes - I was on £15k at the time, he being self employed, his income for mortgage purposes was calculated as an average of 2 years earnings at £11k - we bought a 4 bed semi for £135k with 15% deposit.

Before that we privately rented for 6 years, for one year of which we survived on just one income whilst I finished my final year of uni. I certainly don’t feel like we desperately had to scrimp and live on beans as others have suggested.

Whilst I appreciate some areas of the UK are stupid prices, it’s not like that everywhere and I know we are very foruntate. But I do have to wonder if maybe some people waste money without even realising it rather than having it put aside for a deposit etc. We kitted our first flat out with all second hand furniture, drove second hand cars, had second hand phones. I don’t feel disadvantaged because of that.

I look at friends of similar ages who still live with parents, complain they can’t afford to rent etc, whilst they are driving around in the lastest Mercedes, with a brand new iPhone and a 50inch tv.MFW 2020 #111 Offset Balance £69,394.80/ £69,595.11

Aug 2014 £114,750 -35 yrs (2049)

Sept 2016 £104,800

Nov 2018 £82,500 -24 yrs (2042)0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards