We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Stamp duty... Help!!

Charlieaston

Posts: 1 Newbie

I was wondering if anyone is able to help?

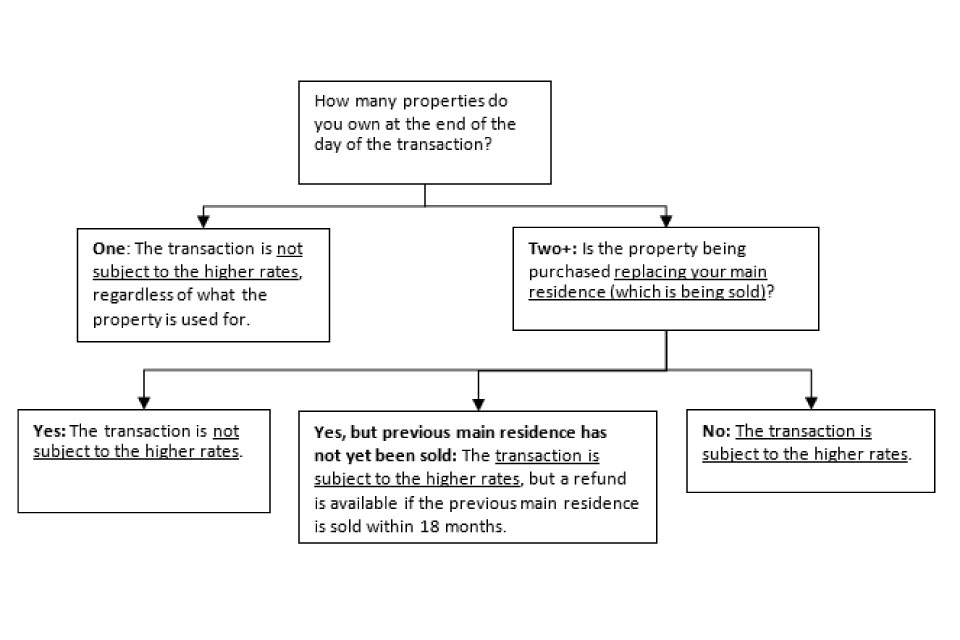

I do not own a residential property, I live with my Mum. My first purchase was a buy to let, which I paid standard stamp duty on as it was my only property. My second property was also a buy to let. This was charged at the higher rate. I have now sold and am replacing my initial property with a bigger buy to let. I have been told that this will be charged at the higher rate stamp duty because it is not my only property or my main residence. BUT, my argument is that I have replaced the initial property which was classed as my main property in terms of stamp duty. If I pay higher rate this means that I will not have any properties which have been charged at the standard rate. Surely I should be allowed one "main residence" in terms of stamp duty, despite the fact that they are both on buy to let mortgages?

I do not own a residential property, I live with my Mum. My first purchase was a buy to let, which I paid standard stamp duty on as it was my only property. My second property was also a buy to let. This was charged at the higher rate. I have now sold and am replacing my initial property with a bigger buy to let. I have been told that this will be charged at the higher rate stamp duty because it is not my only property or my main residence. BUT, my argument is that I have replaced the initial property which was classed as my main property in terms of stamp duty. If I pay higher rate this means that I will not have any properties which have been charged at the standard rate. Surely I should be allowed one "main residence" in terms of stamp duty, despite the fact that they are both on buy to let mortgages?

0

Comments

-

Is not your Mum's house your main residence?0

-

Your main residence is where you live.0

-

in what way do you reside in either of the 2 properties you own which are in fact occupied by your tenants?Charlieaston wrote: »Surely I should be allowed one "main residence" in terms of stamp duty, despite the fact that they are both on buy to let mortgages?

residence means what it says. You are not replacing a main residence, ypu wne from 0 to 1 property (thus paid standard rate), then, whilst retaining ownership of that, you subsequently bought an additional property going from 1 to 2 (higher rate) then 2 to 1 (no SDLT on a sale) and now you are again from 1 to 2 (HR), none of which have been your residences.0 -

Charlieaston wrote: »I was wondering if anyone is able to help?

I do not own a residential property, I live with my Mum. - okay, so that's your main residence. My first purchase was a buy to let, which I paid standard stamp duty on as it was my only property. - correct,

because it was your ONLY property, not because it was your 'main residence'. My second property was also a buy to let. This was charged at the higher rate. I have now sold and am replacing my initial property with a bigger buy to let. I have been told that this will be charged at the higher rate stamp duty because it is not my only property or my main residence. BUT, my argument is that I have replaced the initial property which was classed as my main property in terms of stamp duty. - no, it was your first property, nothing to do with main residence. If I pay higher rate this means that I will not have any properties which have been charged at the standard rate. - indeed, it's irrelevant what rate a property was previously charged at. The concept of stamp duty is a charge when you buy, which is not refunded when you sell.

The more times you buy, the more you pay. Surely I should be allowed one "main residence" in terms of stamp duty, despite the fact that they are both on buy to let mortgages? - the mortgage is irrelevant.

Higher rate SDLT is due on any purchase where you already own a property unless you are replacing your main residence. The concept of stamp duty was for each time you purchase, with no refund on sale. There is a caveat for people moving house on the additional 3% portion, not for changing your BTL portfolio.

What you think is fair aside, that's how it is, there's no grey area.0 -

As others have said, your main residence is your mum's house.

So there is no 'main residence' relief available on your latest purchase.0 -

Echo other views stated here. Main residence == The one you buy to live in.

As an aside, have you considered the change in laws about removing tax relief for the mortgage interest? By 2020 you will have to pay tax for every penny of rent you receive. Check - https://www.which.co.uk/money/tax/income-tax/guides/tax-on-property-and-rental-income/buy-to-let-mortgage-tax-relief-changes-explained0 -

When you buy a residential home for yourself, you will pay standard rate as far as I am aware.

But this BTL purchase will 100% incur higher rate stamp duty.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

You'll presumably be purchasing via a solicitor who will know the exact answer?0

-

No, you pay tax on profit, defined as rental income less non financing expenses. Then you get upto 20% tax relief on mortgage interest (from 2020, more until then). So if you are a basic rate then the result is you don't pay any tax on the financing portion, if you are higher rate then you pay less than your full rate on the fianncing portion.As an aside, have you considered the change in laws about removing tax relief for the mortgage interest? By 2020 you will have to pay tax for every penny of rent you receive. Check - https://www.which.co.uk/money/tax/income-tax/guides/tax-on-property-and-rental-income/buy-to-let-mortgage-tax-relief-changes-explained

No, when OP buys a residential home they will presumably not be selling another main residence (as they live with mum). As OP already owns property, the new purchase will be at higher rate, even if they move in.When you buy a residential home for yourself, you will pay standard rate as far as I am aware.

But this BTL purchase will 100% incur higher rate stamp duty.

It's not helpful to sprout wildly incorrect statements.0 -

Ouch! I did say as far as I am aware - I never actually commited myself 100%.It's not helpful to sprout wildly incorrect statements.

I have just have a look on the HMRC website and you are correct.

https://www.gov.uk/government/consultations/consultation-on-higher-rates-of-stamp-duty-land-tax-sdlt-on-purchases-of-additional-residential-properties/higher-rates-of-stamp-duty-land-tax-sdlt-on-purchases-of-additional-residential-propertiesI am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards