We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Halifax Clarity Card 'interest'

Comments

-

Opened account in April. The first ever transaction was a £10 purchase transaction done on 10 April. Statement date 16 April 2018 says I had to pay minimum £5 by 11 May 2018. And it says 'Next months estimated interest £0.16'. Presumably that's if I had paid the minimum payment. Anyway there is no doubt that my payments had covered this purchase before covering anything else. Correct?If you carried a balance forward from your previous statement then you'd presumably have an interest charge applied to the current statement, but I don't see this on your extracts. Is it possible that some of the £1.68 relates to trailing interest, even though it seems to be attributed to cash?0 -

....in which case your earlier post is rather misleading!OceanSound wrote: »Opened account in April. The first ever transaction was a £10 purchase transaction done on 10 April.

(as is their reference to 'balance from previous statement')OceanSound wrote: »I had a statement balance of £10 for March.0 -

No idea who put you up to leaving this as your first post. However, it's not up to me to convince Halifax. It's up to them to abide by the rules. 'highest interest first' is the practice all credit card companies must abide by.....You'd also probably have a very hard time convincing Halifax to change their systems to debit payments in "highest interest first" order too,.....0 -

OceanSound wrote: »No idea who put you up to leaving this as your first post. However, it's not up to me to convince Halifax. It's up to them to abide by the rules. 'highest interest first' is the practice all credit card companies must abide by.

There was a minimal balance on your card when you made the payment, the £124.14 extra put you in credit. The cash and purchases were still pending and hadn't yet posted to the account. Had you waited until the 23rd April to make the payment, you wouldn't have ended up in the situation you now find yourself in.

No-one "put me up" to post anything, if you think I've an ulterior motive somewhere that honestly says more about you than about me.0 -

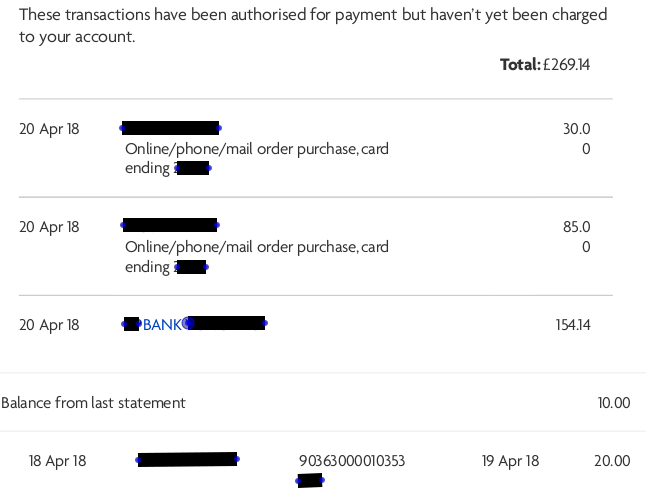

Payment allocation should happen immediately. The point is that there was nothing to allocate most of your payment to, since it was posted on the 20th before your cash withdrawal was posted on the 23rd. So it created a credit balance, which was mopped up by the transactions on the 23rd. It seems the purchases were posted before the cash withdrawal, so these mopped up the credit balance first.OceanSound wrote: »I always view pending transactions especially after a cash pull and take screenprint. This time was no exception. See below:

I think I would definitely have avoided the interest if I had done (2). i.e. paid off ATM withdrawal amount + send payment to cover all purchases. Then after the cash transaction is posted, there would just be the difference between ATM pull posted amount and pending transaction amount ( £156.50 - £154.14 = £2.36) to pay after a few days. When I say 'pay' I mean for this specific instance. However, I imagine it could end up as a credit if the exchange rate goes up (pound becomes stronger).

About (1): I don't know if waiting for transaction to post would have solved it on this occasion. See:

I had £10 balance from previous month. A £20 transaction on 18 April, then two purchases for £85 and £30 on the same date as the cash pull. They were all posted (entered) on the same date 23 April 2018. Surely, my payments of £154.14 and £2.36 should have gone towards:

1) Overdue balance from previous month (£10.00)

2) other transactions posted in the order:

a) cash transactions

b) purchases

c) balance transfers and money transfers

d) default charges (plus any interest or charges incurred as a result of those balances).

It's not really clear if the payment allocation happens immediately upon payment or when the statement is produced. If immediately, £10 of my £154.14 payment would have gone towards clearing last months balance, then the remainder of £144.14 should have gone towards clearing my cash transaction. This hasn't happened, only £9.82 from my payments of £156.50 has been allocated towards the cash transaction (see: screenprint on post#10)

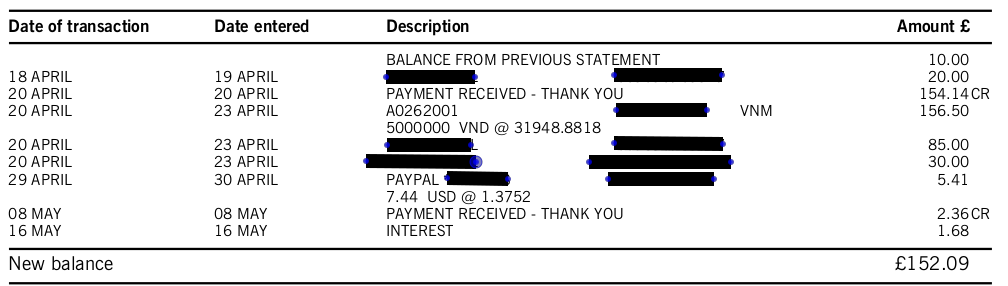

So:- Statement of £10

- Purchase of £20 (19th April)

- Payment of £154.14 (20th)

- This would have paid off the £30 balance, leaving a credit of £124.14

- Purchase of £85 (23rd)

- Purchase of £30 (23rd)

- Balance now credit of £9.14

- Cash withdrawal of £156.50 (23rd)

- Leaving balance of £147.36 of cash advance, so accruing interest

- Purchase of £5.41 (30th)

- Balance now £147.36 cash and £5.41 purchases

- Payment of £2.36 (8th May)

- Allocated to cash as per rules, as you now have a cash balance. Balance now £145 cash and £5.41 purchases

- Statement on 16th May:

- Interest calculated on cash: (147.36 x 15 + 145 x 9) x 0.01456*12/365 = £1.68

- Balance now £146.68 cash (with interest added) and £5.41 purchases

0 -

OceanSound wrote: »You've gone awfully quiet after my last post (You're usually a very vocal lot).

Because between 1.42pm and 5.13pm I was doing a day job, perhaps other posters had other things to do also (or even other threads to engage in)? The gist of your enquiry had been answered even if the detail hadn't been drilled down.0 -

Before we start

1) Do not pay off a cash withdrawal until it actually debits your account. (aka do not pay off a pending transaction)

2) It's cheaper to withdraw cash Sunday-Thursday. Otherwise it takes longer for the account to be debited, and you pay more interest while you are waiting.

Paying it off

1) Wait until the Halifax mobile app/website tells you that the cash withdrawal has actually been debited.

2) Make the payment. This should be for

a) The previous month's balance plus the cost of the cash withdrawal (if you haven't already paid off the card)

b) the cost of the cash withdrawal, (if you've already paid off last month's

balance)

I've used this method since day 1 (back in 2011), and I have never had more than pennies worth of interest* on the statement with the cash withdrawal, and no further interest after that, and I retained the interest free period on all card purchases.

The only time you can definitely get away with paying off a cash withdrawal before it debits is if you have a zero balance on the card, AND you have no pending card purchases.

PochiSoldi

* Still cheaper than any other method of obtaining foreign cash.0 -

Clearly I've hit a raw nerve.chattychappy wrote: »Because between 1.42pm and 5.13pm I was doing a day job, perhaps other posters had other things to do also (or even other threads to engage in)? The gist of your enquiry had been answered even if the detail hadn't been drilled down.

Is this the reason for a flurry of replies soon after my message at 4.13pm?perhaps other posters had other things to do also (or even other threads to engage in)?

You can see for yourself. Replies at 4:42pm, 2x mesages at 4:43pm.0 -

There was a minimal balance on your card when you made the payment, the £124.14 extra put you in credit. The cash and purchases were still pending and hadn't yet posted to the account. Had you waited until the 23rd April to make the payment, you wouldn't have ended up in the situation you now find yourself in.

No-one "put me up" to post anything, if you think I've an ulterior motive somewhere that honestly says more about you than about me.

Not buying this. Even if I waited until the 23rd ** the payment would have been allocated to the purchases first as they've were carried earlier on 20 April before the cash transaction....Had you waited until the 23rd April to make the payment, you wouldn't have ended up in the situation you now find yourself in.

I think you mean, Waited until the 23rd, then made a payment to cover the previous statement balance, all the purchases up to 20th and the cash transaction.

It would be good if there is a breakdown of balance (similar to the one in post#10) through internet banking so the customer can see how his payment(s) are allocated before he/she receives the statement (as it is, this is when he/she become aware of the allocation).

** - note that there was nothing on these forums to suggest that we should wait until the cash transaction is posted (as opposed to hitting the account). Only now you guys have started to shout it from the roof tops.0 -

I think your post offers the best explanation. (I'm basing this on content, without looking at the 'likes')Payment allocation should happen immediately. The point is that there was nothing to allocate most of your payment to, since it was posted on the 20th before your cash withdrawal was posted on the 23rd. So it created a credit balance, which was mopped up by the transactions on the 23rd. It seems the purchases were posted before the cash withdrawal, so these mopped up the credit balance first.

So:- Statement of £10

- Purchase of £20 (19th April)

- Payment of £154.14 (20th)

- This would have paid off the £30 balance, leaving a credit of £124.14

- Purchase of £85 (23rd)

- Purchase of £30 (23rd)

- Balance now credit of £9.14

- Cash withdrawal of £156.50 (23rd)

- Leaving balance of £147.36 of cash advance, so accruing interest

- Purchase of £5.41 (30th)

- Balance now £147.36 cash and £5.41 purchases

- Payment of £2.36 (8th May)

- Allocated to cash as per rules, as you now have a cash balance. Balance now £145 cash and £5.41 purchases

- Statement on 16th May:

- Interest calculated on cash: (147.36 x 15 + 145 x 9) x 0.01456*12/365 = £1.68

- Balance now £146.68 cash (with interest added) and £5.41 purchases

I believe this is because I carried out the two purchases on the morning of 20 April before carrying out the cash withdrawal in the afternoon.It seems the purchases were posted before the cash withdrawal, so these mopped up the credit balance first.

Otherwise, it would have been a bit sneaky to arbitrarily/randomly post them ahead of the cash transaction.

I paid off the full statement balance of £152.09 yesterday through online banking. (It's posted on to the clarity account same day)So you need to make a payment of £146.68 asap and that will clear the cash, and you'll pay 7p interest a day until you pay it.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards