We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Why is 'Timing' the market bad ?

Comments

-

There's also the old rule "if you don't need the return don't take the risk". Somebody whose investments are required to grow to achieve some total that would then underwrite some cherished plan would be rash to leave money in the markets after that target had been achieved.Free the dunston one next time too.0

-

How do you know in advance when its 'a good time to invest?

at the bottom of the market in 2008 a lot of people were saying its 'the wrong cycle of the financial market to invest'.

vast majority of people are telling you that we are in the wrong cycle of the financial market to invest then it is not sensible to invest at this time of the market.

To come back to the thread title 'Why is timing the market bad' I think the answer is because you are predicting the future, which is notoriously difficult.

Markets are increasingly moved by politics, and the big investors who can hire 'Self Employed' Members of Parliament with inside knowledge have the advantage over us.“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” --Upton Sinclair0 -

How can you tell when it is at a peak? Are we at a peak now? Did you think we were at a peak last year? How about the year before that? What should you do with your money while you are waiting for the crash? If you have already waited several years, should you continue to wait even longer?Similar to buy property, it is not sensible to buy it when they are at peak like the one in 2000.0 -

........

Similar to buy property, it is not sensible to buy it when they are at peak like the one in 2000. You might still be making a gain in "time in the market" buying property when they are at peak. But People who bought their property when the credit crunch hit in 2008-2009 and the forget it (the combination of the two) will make the highest gain.

.......

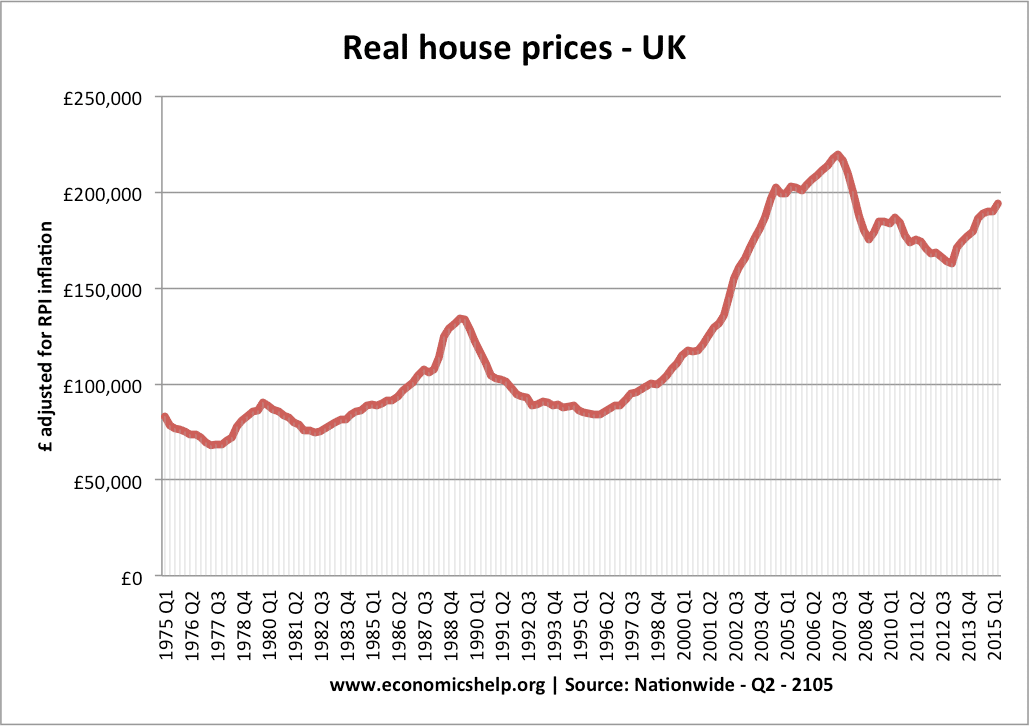

This is a good example of why timing the market is so difficult and often counter productive...

See graph

Why you chose 2000 I am not sure, but prices reached a new peak around 2001/Q2. Only with hindsight can you see that it wasnt a maximum. If you had decided not to buy then you would either have bought later at a higher price or still be out of the market.

Conversely if you had been luck enough to hit the low in 2008 you would still be down some 5 years later.0 -

Nice post, thanks. I still regard myself as a newbie investor although I've been getting more active in the last couple of years as I approach retirement (I had an initial FA review but then decided to manage my own investments). Like many newbies I was getting attracted to the passive, index funds approach and of course the VLS funds. The lower costs were appealing.BrockStoker wrote: »For anyone else out there reading this who might be new to investing, now is definitely NOT the time to sell, and probably not the time to buy yet either. If this turns into long drawn out correction as I suspect it might, the next few weeks could be just the start. Of course there are no guarantees, and buying sooner rather than later may make more sense depending on your particular situation and what is happening in the world.

...........

Apologies for the lengthy post, but I would rather be long winded than vague!

However, I've decided to hold off for now after reading so much information on here. I am a safety first investor and am wary of a correction because the IMO market is closer to a peak than a trough and there are a lot of uncertainties on the short term horizon. So I'm holding a big chunk of my portfolio in cash because I am retiring next year. I decided not to switch into things like VLS because a) I'll be buying at a high price and b) like many people have said, they have not been tested through a market correction. So I'm keeping my current investments (which are mostly in active funds) as they are, not switching to VLS or similar. The only new fund I am adding now is the new Woodford income fund (because I like the investment strategy of that fund).

Once I am into retirement I can see myself shifting in 2 to 3 years time into more longer term, lower cost passive funds. Hopefully we will have seen what direction the markets are taking by then, but of course we still won't know for sure what the future holds.0 -

You might want to discuss your timing strategy with one of the people behind the Monevator blog. They thought the same thing about not buying property in 2000 because it was overvalued although they could have done so. 17 years later they were still renting because they can no longer afford to buy.Similar to buy property, it is not sensible to buy it when they are at peak like the one in 2000. You might still be making a gain in "time in the market" buying property when they are at peak. But People who bought their property when the credit crunch hit in 2008-2009 and the forget it (the combination of the two) will make the highest gain.Remember the saying: if it looks too good to be true it almost certainly is.0 -

AnotherJoe wrote: »Which economies shares would that panic affect?

What would such a panic do to the Pound?

How would that affect the prices of non UK shares priced in foreign currencies?

Indeed what would it do to the prices of UK shares whose trading is mostly outside the UK? (clue, look at what happened to FTSE100 in the aftermath of the vote panic)

1. Value could fall

2. This is really quite embarrassing but I had to get pencil and paper to work out this out. And i'm still not sure I'm right...

A weak/low £ exchange rate is good for buyers of shares in the currency it's fallen against. Bad for sellers.

A high/strong £ exchange rate is good for sellers of the shares in the currency the £ has risen against. Bad for buyers.

I hope this is the right way around...:o

So if the £ dropped it wouldn't directly affect the prices of non-UK shares not listed in £. But a falling £ would mean that anyone holding such stock has an investment that is now not worth as much in £.

3. I *think* these share prices may rise exports will be cheaper for the purchasing countries when the £ is 'low'.0 -

OldMusicGuy wrote: »Nice post, thanks. I still regard myself as a newbie investor although I've been getting more active in the last couple of years as I approach retirement (I had an initial FA review but then decided to manage my own investments). Like many newbies I was getting attracted to the passive, index funds approach and of course the VLS funds. The lower costs were appealing.

However, I've decided to hold off for now after reading so much information on here. I am a safety first investor and am wary of a correction because the IMO market is closer to a peak than a trough and there are a lot of uncertainties on the short term horizon. So I'm holding a big chunk of my portfolio in cash because I am retiring next year. I decided not to switch into things like VLS because a) I'll be buying at a high price and b) like many people have said, they have not been tested through a market correction. So I'm keeping my current investments (which are mostly in active funds) as they are, not switching to VLS or similar. The only new fund I am adding now is the new Woodford income fund (because I like the investment strategy of that fund).

Once I am into retirement I can see myself shifting in 2 to 3 years time into more longer term, lower cost passive funds. Hopefully we will have seen what direction the markets are taking by then, but of course we still won't know for sure what the future holds.

I am minded to think similarly. In the meantime I will bung cash into tax wrappers in anticipation of a correction, whether Brexit-led or not, then buy when things are lower.0 -

You might want to discuss your timing strategy with one of the people behind the Monevator blog. They thought the same thing about not buying property in 2000 because it was overvalued although they could have done so. 17 years later they were still renting because they can no longer afford to buy.

Renting for 17 years, woow ?????. The money from the rent itself probably probably already cover a fractional of the value of the house or multiple value of the deposit.

What I could say is that the people who waited until 17 years to buy a house when they already needed it are the people who do not intend to buy in the first instance, do not have enough deposit, just a desire. There have never been in the history about boom and bust in the property market taking so long.

You do not need to be on the peak and people are right when saying that people do not know whether we are at the peak. But what is needed imo is to be in the right cycle. To be in the right cycle there are a few years time to make decision, not just one year. The people who bought property when the credit crunch cycle hit was the clear winner. People have a few years at that time to make decision not just short period of less than one year. But most people who read the news know that we were in the credit crunch at that time. At most people know that we are not in the credit crunch anymore now.0 -

So, you'd suggest that since we are nearly 10 years from the credit crunch, people would be best off waiting for the next event that will cause property to tumble? What if it turns out to be 10 years away?The people who bought property when the credit crunch cycle hit was the clear winner. People have a few years at that time to make decision not just short period of less than one year. But most people who read the news know that we were in the credit crunch at that time. At most people know that we are not in the credit crunch anymore now.0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards