We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

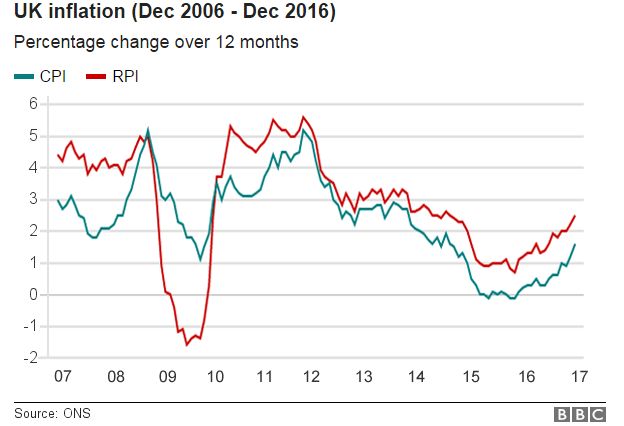

UK Inflation Rate

Comments

-

Graham_Devon wrote: »Rules on that have changed now.

It's all about Brexit now. Keep up!

Funny thing is, when it was back at 5%, how many times was I told this wasn't high, it's not a problem?

Now, after Brexit, 1.6% seems to be a massive problem, poor won't eat, people will lose jobs etc etc! Where was the worry for the poor when inflation was nearly 3 times higher?!?!

Its the same for tariffs. Apparently (according to remainers) a 10% tariff on exports to the EU would be a catastrophe, whereas a 10% tariff added on now would mean that UK exports to the EU would still be cheaper than they were on June 22nd, when apparently everything was fine.0 -

I worry, inflation is so much higher than it has ever been since interest rates have been at 0.5%...not.

As in 2010-13, inflating away personal and national debt is economically beneficial to the uk.

It's only unanticipated inflation that does that. Anticipated inflation simply causes nominal interest rates to rise to compensate lenders and so just moves the burden of repayment from tomorrow to today as interest is paid today and principle is mostly paid tomorrow.

I don't think that the coming bout of inflation can reasonably be described as unexpected.0 -

Graham_Devon wrote: »Now, after Brexit, 1.6% seems to be a massive problem

Does it? Did anyone say 1.6% is a massive problem?Don't blame me, I voted Remain.0 -

Have been noticing diesel drifting above £1.20 lately.

After 6 months of grind we've managed to get price increases through to our biggest customers (c10%). Not what we 'needed' but it seems retailers are starting to cease the King Canute impersonations.

It's now up to the consumer to decide which is as it should be. They shouldn't be shielded from their own decisions.0 -

Really - I haven't seen personal borrowing costs and gilt yields rising as much as inflation expectations thus real rates are lower = inflating away debtdavomcdave wrote: »It's only unanticipated inflation that does that. Anticipated inflation simply causes nominal interest rates to rise to compensate lenders and so just moves the burden of repayment from tomorrow to today as interest is paid today and principle is mostly paid tomorrow.

I don't think that the coming bout of inflation can reasonably be described as unexpected.I think....0 -

So once again savers get screwed and the reckless borrowers are rewarded. I am in the process of buying a house and I currently have a six figure sum in the bank earning 1.05%, yet inflation is actually 1.6% (at the moment, I am sure it will go higher) So I am losing 0.55% a year.

Sainsburys are currently lending money at 2.8%, so with inflation at 1.6% the real cost is only 1.2%

Just wait until Mark Carney decides to lower interest rates again, I still don't think negative rates are out of the question, after all got to keep house prices rising to protect his massive BTL empire.

Personally I think holding any sort of money in the bank these days is silly, you need to put it into assets to protect it and make money. The government are just going to keep printing lots of money through QE so inflation can only go higher and money in the bank will lose more and more value.

It ensures asset prices increase and the debt is eroded by inflation, a win/win for the government inventing money out of thin air.0 -

PeterPanic wrote: »So once again savers get screwed and the reckless borrowers are rewarded. I am in the process of buying a house and I currently have a six figure sum in the bank earning 1.05%, yet inflation is actually 1.6% (at the moment, I am sure it will go higher) So I am losing 0.55% a year.a win/win for the government inventing money out of thin air.

What sort of return do you think you should get for taking absolutely no risk with your £100k? If it's split across two accounts then it's fully protected and if your bank(s) go bust you'll be delighted when the taxpayer borrows some money to ensure you stay wealthy.0 -

PeterPanic wrote: »So once again savers get screwed and the reckless borrowers are rewarded. I am in the process of buying a house and I currently have a six figure sum in the bank earning 1.05%, yet inflation is actually 1.6% (at the moment, I am sure it will go higher) So I am losing 0.55% a year.

Sainsburys are currently lending money at 2.8%, so with inflation at 1.6% the real cost is only 1.2%

Just wait until Mark Carney decides to lower interest rates again, I still don't think negative rates are out of the question, after all got to keep house prices rising to protect his massive BTL empire.

Personally I think holding any sort of money in the bank these days is silly, you need to put it into assets to protect it and make money. The government are just going to keep printing lots of money through QE so inflation can only go higher and money in the bank will lose more and more value.

It ensures asset prices increase and the debt is eroded by inflation, a win/win for the government inventing money out of thin air.

then stop complaining and put your money elsewhere!0 -

I have been noticing the increased price of crude oil - which is now hovering around the mid-$50's.Have been noticing diesel drifting above £1.20 lately.

So little wonder diesel is up.

Still, when this voluntary production limit proves itself to be ineffective the price will again reduce, at least a little.0 -

PeterPanic wrote: »So once again savers get screwed and the reckless borrowers are rewarded. I am in the process of buying a house and I currently have a six figure sum in the bank earning 1.05%, yet inflation is actually 1.6% (at the moment, I am sure it will go higher) So I am losing 0.55% a year.

Along with (older) pensioners you are in the other group (soon to buy a house) that I feel sorry for, because you more or less have to stay in cash, as it would be foolish to risk the short term volatility of equities. Whereas others with distant horizons can invest in the stock market, and receive decent dividend income, which is also tax free for a lot of people.

Although I personally don't believe that there are that many 'reckless borrowers'. I enjoy low margin tracker mortgages, but I am a net investor/saver, not a borrower, but those who have stretched their finances to buy a home aren't usually being reckless.Chuck Norris can kill two stones with one birdThe only time Chuck Norris was wrong was when he thought he had made a mistakeChuck Norris puts the "laughter" in "manslaughter".I've started running again, after several injuries had forced me to stop0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards