We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How long will your savings last?

Comments

-

With many equity markets now at highs the method currently indicates a reduced holding in equities.

And an increased holding in ...I am not a financial adviser and neither do I play one on television. I might occasionally give bad advice but at least it's free.

Like all religions, the Faith of the Invisible Pink Unicorns is based upon both logic and faith. We have faith that they are pink; we logically know that they are invisible because we can't see them.0 -

gadgetmind wrote: »And an increased holding in ...

I'm going for peer 2 peer.0 -

P2P.gadgetmind wrote: »And an increased holding in ...

It's a switch I've been writing about for a year or so now and it's still going on, with something over 75% of my investable money going to be in P2P by the time I'm finished.

Not based on Guyton's recent work but based in part on the underlying study of cyclically adjusted P/E and the current opportunities in P2P. Same general conclusion behind it, though, and I'll happily go back heavily into equities when conditions seem favourable for that move.0 -

Not so easy when the bulk of your investments are in pensions and ISAs.I am not a financial adviser and neither do I play one on television. I might occasionally give bad advice but at least it's free.

Like all religions, the Faith of the Invisible Pink Unicorns is based upon both logic and faith. We have faith that they are pink; we logically know that they are invisible because we can't see them.0 -

That's where the bulk of mine are.

If you have at least £200k in pensions you can use something like the EvolutionSIPP via SIPPclub. It's not cheap but it is worthwhile if you have sufficient money to invest.

For ISAs you can use a flexible ISA that allows withdrawing and redepositing past year money. Transfer from S&S to flexible (if the S&S isn't flexible already) then withdraw and invest in P2P that allows an easy exit via resale. Sell close to end of year to preserve the ISA allowance and repeat. Until there are IF ISAs around that are of interest, which will eventually happen. Until then flexible ISA is the workaround. I'm using the Skipton easy access ISA for this.0 -

I have plenty enough in one SIPP to make this worthwhile, but between exposure to infrastructure, bonds, and commercial property, I'd need to pretty good incentive to move it, particularly if fees are high.

However, the bulk of my pension is a GPP with Friends Life, and they say they won't allow partial transfers out while leaving scheme running.

For ISAs, it's taken us decades to build them up, and I'd hate to blow this by messing up timing!I am not a financial adviser and neither do I play one on television. I might occasionally give bad advice but at least it's free.

Like all religions, the Faith of the Invisible Pink Unicorns is based upon both logic and faith. We have faith that they are pink; we logically know that they are invisible because we can't see them.0 -

James I'm aware of the equity gilt study and referenced it earlier in the thread.

The issue is how accurate the cash element of the analysis is. Most pointedly do you think the average person, let alone those aware enough to shop around, earned -0.2% return on cash on the last decade?

The returns available on cash will almost certainly be better than those quoted but to what extent I don't k ow and don't know a reasonable source, though there may well be one for the last few decades.

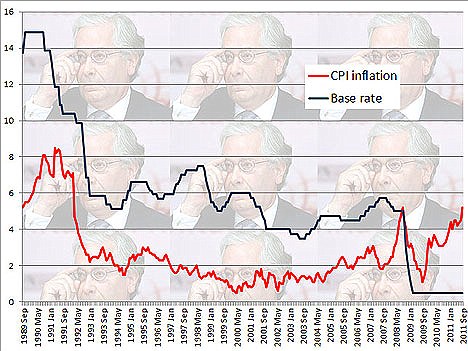

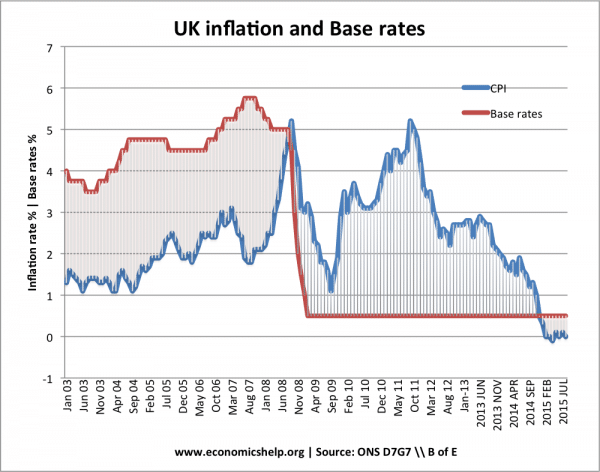

As we know the link between inflation and base rates was broken around 2008 after the financial crash.

This may have caused cash savers to search for other alternatives in recent years.

http://3.bp.blogspot.com/-8U3p91Pd3Q0/Tp5yZ4sbUgI/AAAAAAAACxE/ZMj0QWe7shg/s1600/Inflation%2Bvs%2Bbase%2Brate.jpg

http://www.economicshelp.org/wp-content/uploads/2015/03/inflation-interest-rates-600x472.png

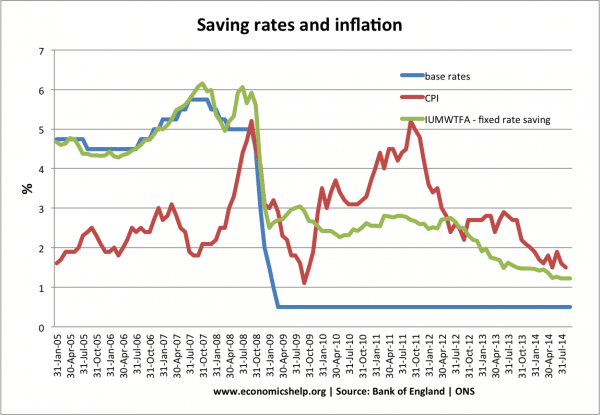

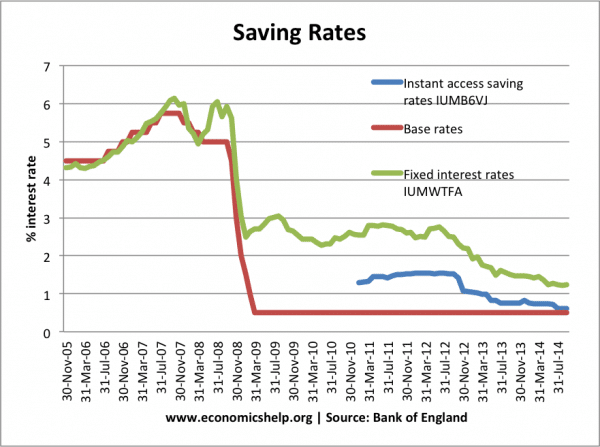

Fixed rate savings bonds and even some ordinary accounts have still paid more than the base rate since 2008.

http://www.economicshelp.org/wp-content/uploads/2014/10/saving-rates-inflation-since-05-600x415.png

http://www.economicshelp.org/wp-content/uploads/2014/10/saving-rates-base-fixed-instant-600x447.png

I can't imagine it being difficult to get a yearly fix rate bond at base rate plus 1% over the years from a building society...I've had plenty myself.

http://www.bankofengland.co.uk/boeapps/iadb/Repo.asp

I've managed to find the latest study for 2016..

http://www.courtiers.co.uk/news/barclays-equity-gilt-study-2016

http://www.courtiers.co.uk/LiteratureRetrieve.aspx?ID=140090

Decent link going back to 1960..

http://www.swanlowpark.co.uk/savingsinterestannual.jsp0 -

Interesting, well certainly that last link.

Those rates look better than I would have expected for the last half century, though the seventies would have been a tough time and I would guess that savers would have lost money in real terms for some of those years.

I guess you can't necessarily trust the independence of any analysis absolutely, and the specific data is key, but it appears that the Barclays study is poor with respect to giving accurate returns on cash in comparison with other asset classes.0 -

That's where the bulk of mine are.

If you have at least £200k in pensions you can use something like the EvolutionSIPP via SIPPclub. It's not cheap but it is worthwhile if you have sufficient money to invest.

I am eligible for sippclub, I crunched the sippclub numbers last year and given my circumstances found it wouldn't be worthwhile unless I had £140k in p2p which for me means a portfolio of about £1.4m, which I do not have. And that's for basically breaking even with the fee. And with the innovative ISA soon, probably even more. So IF you have 75% of your portfolio in p2p then yes about £200k of portfolio is the start point of considering it. But how many people put 75% in p2p?0 -

It's a flat rate fee rather than percentage-based so it's probably not actually high for the sort of sums likely to be involved. Definitely not the cheapest but then the cheapest don't allow the range of investments.gadgetmind wrote: »I have plenty enough in one SIPP to make this worthwhile, but between exposure to infrastructure, bonds, and commercial property, I'd need to pretty good incentive to move it, particularly if fees are high.

That's the standard SL line as well but they will negotiate to allow it at scheme level and did for my workplace one when asked. Don't know whether FL would do the same or whether it's be viable to stop, transfer and restart as a workaround at your place. Would be something to ask those responsible for the pension scheme to pay attention to with the next terms negotiation, though.gadgetmind wrote: »However, the bulk of my pension is a GPP with Friends Life, and they say they won't allow partial transfers out while leaving scheme running.

SIPPClub isn't limited to just P2P. It's a pretty full-featured SIPP that also supports the standard ranges of investments. I doubt that most would go 75% into P2P but there are plenty of other choices in shares and funds and such that can be held within it. Still, I assume that you considered this and found that it still wouldn't be worthwhile for you.TheTracker wrote: »I am eligible for sippclub, I crunched the sippclub numbers last year and given my circumstances found it wouldn't be worthwhile unless I had £140k in p2p which for me means a portfolio of about £1.4m, which I do not have. And that's for basically breaking even with the fee. And with the innovative ISA soon, probably even more. So IF you have 75% of your portfolio in p2p then yes about £200k of portfolio is the start point of considering it. But how many people put 75% in p2p?0

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards