We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is there really a housing shortage?

Comments

-

23million homes, but a lot of them aren't available to live in. Apart from the abandoned/shabby ones, think about all the holiday cottages for hire and the privately owned 2nd homes. All those people you see on the telly with a home in the country and a pied-a-terre in the town.

So there's probably 15million homes when you take that lot out.

In some parts of Cornwall 75% of houses are 2nd homes.

Then there are student houses. They've all got a home elsewhere. So remove student houses from equation too.0 -

PasturesNew wrote: »23million homes, but a lot of them aren't available to live in. Apart from the abandoned/shabby ones, think about all the holiday cottages for hire and the privately owned 2nd homes. All those people you see on the telly with a home in the country and a pied-a-terre in the town.

So there's probably 15million homes when you take that lot out.

.

Your numbers are way, way off.

There are only about 335,000 households in England who own a second home in the UK.

There are only 670,000 households who own a second home anywhere at all, but for around half of them, that second home is overseas.

Source: https://www.gov.uk/government/statistical-data-sets/owner-occupiers-recent-first-time-buyers-and-second-homes“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0 -

It is ridiculous to suggest that cheap credit plays no part in the upward pressure on house prices. Even during your so called ideal years of 2000-2007 when lending was at it's easiest, prices were increasing.

I have not said it plays no part, clearly the cheaper credit is, the greater affordability becomes for higher prices, but the primary causation runs from the shortage/prices to credit and not the other way around and I'm not the only person to think so.

Here's an excerpt from a report by the BBC economics editor discussing a BOE research paper that makes those same claims.

http://www.bbc.co.uk/news/business-17398014the median loan-to-value ratio on a new mortgage didn't go up during the "boom" years - in fact, for most of the 1990s and noughties it was falling.

That's consistent with the idea that rising house prices caused bigger mortgages - not the other way around.

In 2007 at the previous peak base rates were almost 6%, so you can't blame 'cheap credit' for that, and as for your observation around 'easy credit' it remains an indisputable fact that more people were able to buy and more houses were getting built between 2000 - 2007 than is the case today or at any time since.

My assertion, and there is plenty of evidence to back this up, is twofold:

1. You cannot cure high prices, that are primarily caused by a housing shortage, via rationing credit.

Credit has been significantly rationed since 2007, mortgage numbers fell by half and remain at only two thirds the long term average, and new building is at around 100 year lows causing the housing shortage to worsen significantly.

2. As a result of (1) average prices have now recovered to new peak levels, despite credit issuance in terms of mortgage volumes remaining lower than both the peak and the long term average.

Prices are always, and only ever, set by supply and demand.

The availability and price of credit are a component of effective demand.

But throttling effective demand via reducing the availability of credit will not sustainably reduce house prices where a shortage exists.

The last 8 years are all the evidence you need to see that.“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0 -

This might help in the discussion.. http://www.neighbourhood.statistics.gov.uk/HTMLDocs/dvc134_c/index.html0

-

ringo_24601 wrote: »This might help in the discussion.. http://www.neighbourhood.statistics.gov.uk/HTMLDocs/dvc134_c/index.html

The interactive feature on that map is actually interesting.

Huge parts of England, and almost all of Wales and Scotland, have very, very low population density, below 100 people per sq Km.

Most of England has low population density, ie, under 300 people per sq km, including a surprising number of places in the South East.

The stats really are skewed by a handful of cities with very high population density, like central London at over 14,000 people per sq Km.“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0 -

HAMISH_MCTAVISH wrote: »I have not said it plays no part, clearly the cheaper credit is, the greater affordability becomes for higher prices, but the primary causation runs from the shortage/prices to credit and not the other way around and I'm not the only person to think so.

Here's an excerpt from a report by the BBC economics editor discussing a BOE research paper that makes those same claims.

http://www.bbc.co.uk/news/business-17398014

In 2007 at the previous peak base rates were almost 6%, so you can't blame 'cheap credit' for that, and as for your observation around 'easy credit' it remains an indisputable fact that more people were able to buy and more houses were getting built between 2000 - 2007 than is the case today or at any time since.

My assertion, and there is plenty of evidence to back this up, is twofold:

1. You cannot cure high prices, that are primarily caused by a housing shortage, via rationing credit.

Credit has been significantly rationed since 2007, mortgage numbers fell by half and remain at only two thirds the long term average, and new building is at around 100 year lows causing the housing shortage to worsen significantly.

2. As a result of (1) average prices have now recovered to new peak levels, despite credit issuance in terms of mortgage volumes remaining lower than both the peak and the long term average.

Prices are always, and only ever, set by supply and demand.

The availability and price of credit are a component of effective demand.

But throttling effective demand via reducing the availability of credit will not sustainably reduce house prices where a shortage exists.

The last 8 years are all the evidence you need to see that.

I'll be waiting for the rental graphs from 1970s for a while I suspect. Rent increases will show very clearly the supply demand dynamics because credit play no (or negligible) part in rent prices. I suspect what you'll see is a largely linear graph, such as this one from the FT:

But extending back through multiple decades.

But the house price graph looks very different, it grows exponentially as credit costs lower and term lengths extend, over decades. The trend for mortgage rates has been a multi decade downward trend and the effect has been a multi decade divergence of house prices from rents.

I agree very much with you that this applies only in areas where there is sufficient demand. You can throw as much credit as you like at a market but if people simply don't want to buy, it won't have an effect. Such as in areas where fewer people buy in the UK, prices remain relatively low.0 -

one of the problems is our views of housing size and quality

when people say I cant afford a house or house prices are too high they actually mean, I cant afford a 100 sqm house that is kitted out nicely and in a good location.

It is all good and well for people to want a nice big house in a good location with high spec finish but what happens to the other 70% of homes do we knock them down or leave them empty? the fact of life is that in the UK housing market the median family needs to settle for the median house and the median house is not that desirable but is at least quite affordable in the majority of towns and cities.

if you look up land registry data for the average terrace its very affordable in most places for the median full time working couple on the median local wage some places the cost is below 1 x joint income.

For the 'house prices are too high' crowd to be happy the UK needs to overbuild homes and most the new builds need to be large high spec properties. What remains, the older smaller existing stock can then fall below build cost and they can buy a terrace for 2 shillings. But of course they would then complain that the large new homes should be 2 shillings0 -

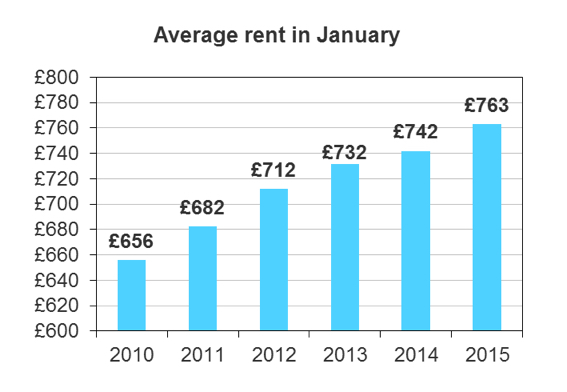

HAMISH_MCTAVISH wrote: »Rents:

FWIW, £656 in 2010 in 2015 money is £758 so the increase in real rents (assuming the above is nominal rents) is £5 or 0.65% in total or about 0.1% a year.

Of course if the above is real rents rather than nominal then I'm talking rubbish.:)0 -

I'll be waiting for the rental graphs from 1970s for a while I suspect. Rent increases will show very clearly the supply demand dynamics because credit play no (or negligible) part in rent prices. I suspect what you'll see is a largely linear graph, such as this one from the FT:

But extending back through multiple decades.

But the house price graph looks very different, it grows exponentially as credit costs lower and term lengths extend, over decades. The trend for mortgage rates has been a multi decade downward trend and the effect has been a multi decade divergence of house prices from rents.

I agree very much with you that this applies only in areas where there is sufficient demand. You can throw as much credit as you like at a market but if people simply don't want to buy, it won't have an effect. Such as in areas where fewer people buy in the UK, prices remain relatively low.

don you think you are totally contradicting yourself?

you say, credit plays no part where supply is good

you also say credit is the root cause of the high prices..... in effect only where supply is not good

so what you are saying is that supply sets prices but trying very hard to hold onto pet theory 1.0 at least unlike a lot of the crash wishers half your brain wants you to see the truth0 -

I'll be waiting for the rental graphs from 1970s for a while I suspect.

I'm not aware of any that exist, and regardless, since 1970 we've had numerous periods of housing surplus as well as periods of housing shortage.Rent increases will show very clearly the supply demand dynamics because credit play no (or negligible) part in rent prices.

This argument has been addressed a number of times on here in previous years, and ICBA rehashing it all now, but to summarise:

You rightly note that rents are not driven by credit.

However rents are driven by supply and demand, and effective demand in this case is limited by income and levels of employment.

Since the crash, rents have soared by far more than both income and inflation. Despite unemployment being high for most of those years. And a material swing in the balance of supply away from O/O and towards rented.

That simply wouldn't happen without a shortage.I suspect what you'll see is a largely linear graph, such as this one from the FT:

I'm not entirely disagreeing with you, albeit I believe as per the BOE report referenced in my earlier post that the causal factor is a shortage of houses driving up prices and that lending follows, not leads this.

But as an FYI that graph uses the flawed ONS rent survey data.

It's flawed because it includes old existing tenancies as well as new tenancies.

Which would be like producing a house price index using sale prices from several years ago as well as current sale prices.I agree very much with you that this applies only in areas where there is sufficient demand. You can throw as much credit as you like at a market but if people simply don't want to buy, it won't have an effect. Such as in areas where fewer people buy in the UK, prices remain relatively low.

Agreed.

Credit availability is pretty much identical across the UK.

Yet a 3 bed Victorian Terrace 'Oop North' can be had for 60K, while a near identical 3 bed Victorian Terrace in London costs over a million.

Supply and demand is the only reason for that differential.“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards