We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is it possible to become a millionaire (or near to) through investments?

Comments

-

Three things to consider:

1. National debt.

2. Deficit.

3. Inflation.

What happens to the real value of the national debt if the deficit is less than the national debt minus the effect of inflation on the real value of the national debt? Answer: it goes down. So long as inflation effect on the national debt is greater than the deficit the national debt is actually decreasing in real terms.

Just like a mortgage, where the real value of the capital falls over time due to inflation until what was a higher debt can become not very significant at all.

Next things to consider:

4. Recession.

5. Stimulous.

6. Economic cycle.

7. Benefits bills in response to a recession.

Cost of benefits naturally increases during a recession as people lose their jobs and the jobs don't all return immediately, there is a many year lag. One desirable thing to do during a recession is to increase spending by the public sector to try to undo some of the harm of the recession affecting private sector spending. This also naturally increases a deficit. It doesn't matter much so long as the external effects on credit rating aren't onerous, particularly in relation to borrowing costs, and so long as growth and inflation can get things back to a sensible level in a reasonable time. Private sector debt tends to decrease during and after a recession so total debt of a nation doesn't increase as rapidly as public sector debt. That increases the ability of future governments to repay by increasing taxes on the less indebted population that can now more easily afford the cost.

The UK has extremely low borrowing costs and a far higher proportion of borrowing that doesn't come due for many decades than is usual. This greatly reduces the risk of running a deficit because there is much reduced prospect of a huge proportion of the debt becoming due rapidly.

For those who don't know it, one of the trends in countries with untrusted debt is that they can't refinance debt they already have for long terms and end up in a spiral of ever more costly debt at ever shorter terms until eventually they are issuing one month or even one week debt at unaffordable interest rates. Which is why a usual part of rescues is long term lower interest rate lending to reduce or eliminate the "you have to pay tomorrow" crisis moments as the shorter term debts for large proportions of the national debt fall due.0 -

BananaRepublic wrote: »

I was familiar with the broad outline of the pie chart spending, (although would prefer to see welfare split into the larger categories of housing benefit, unemployment, disability etc in the actual chart for clarity), and obviously pensions are a problem.

But the thing that threw me was this "other spending" in the list of 106 bn for national and local government, fair enough we have waste management in there etc etc. But in another "other spending" list more than 50 bn of this is "accounting adjustments". This appears to be more than total interest payments and more than the current budget deficit. What on earth are "accounting adjustments" and are they just some bunch of assumptions on this huge amount - maybe PFI or similar?0 -

Three things to consider:

1. National debt.

2. Deficit.

3. Inflation.

What happens to the real value of the national debt if the deficit is less than the national debt minus the effect of inflation on the real value of the national debt? Answer: it goes down. So long as inflation effect on the national debt is greater than the deficit the national debt is actually decreasing in real terms.

Just like a mortgage, where the real value of the capital falls over time due to inflation until what was a higher debt can become not very significant at all.

What about economic growth?

Like inflation it erodes the burden of the debt pile.

To use your mortgage analogy, people find it much easier to service their mortgage as their career progresses and their earning power increases. The difference with an economy is the borrowed money can be invested into things which bring about economic return.0 -

BananaRepublic wrote: »Under the last government the deficit (difference between spending and income) ballooned:

http://www.debtbombshell.com/britains-budget-deficit.htm

The above graph shows the deficit as a % of GDP which is a reasonable measure. A couple more graphs:

http://www.rightsandwrongs.co.uk/qui%20%20ck-links/136-politics-britain/24747-i-promise-to-pay-the-bearer-much-less

the most informative of those graphs is debt-to-GDP ratio. that shows a sudden rise, entirely due to the financial crisis. in fact, the ratio even fell slightly under labour before the financial crisis hit (i.e. 1997-2007).

that labour government is certainly to blame, for its "light touch" regulation of the banks, which allowed the financial crisis to happen. of course, the tories were egging them on at the time, and even said there was still too much regulation.

but that was the problem. nothing to do with overspending on public services, or not raising enough in tax.

and the banks are still not regulated properly. so there is a big risk of another financial crisis.The problem with such a high deficit is that the national debt increases dramatically, and then we end up spending a huge amount of money each year in the form of debt interest. In other words this is money that is not doing anything productive. Pay off the debt,

for a start: pay it off how?

would you like to slash spending on public services now, so that you can raise it higher later, after the debt's been paid off? even if if that were a viable plan (which it isn't - see below), why would you even want to do that?and we then have that money to spend on healthcare etc. This might explain that:

http://www.ukpublicspending.co.uk/uk_budget_pie_chart

It suggests that 6% of government spending is simply to pay the interest on the debt.

that is the nominal amount of interest. paying interest does not increase the debt-to-GDP ratio, unless the nominal interest rate paid is greater than the nominal growth in GDP.

but could the money be used for something more worthwhile?

no. because the UK is not working with a finite quantity of money. the State creates money. the cash we use as money came into existence from past UK governments spending more than they raised in taxes. paying interest on gilts has no direct affect on how much can be spent on public services.

the UK is only limited by real resources, not by quantity of money. if we want to spend on more health and education, the money to pay them can always be created. but if we want more ppl to work in those areas, they can't be working in other sectors at the same time. however, when a lot of ppl are unemployed or under-employed to start with - as they are now! - then cuts in other sectors may not be needed at all.

in the situation where you do need to free up resources from some sectors, then

a) if that's in the public sector, you just cut the spending;

b) if that's in the private sector, you raise taxes sufficiently to put ppl or businesses off from spending - but note that this doesn't usually require eliminating the deficit.It is equivalent to the entire defence budget and half the education budget. It would be nice to increase education spending by 50% instead.

as above: it doesn't work like that. paying interest on gilts uses minimal real resources (i.e. a few officials in the BoE, to process the payments, and so on).(But we will get a Labour government who will find more 'effective' ways to use the money, before creating a new deficit.)

you are rather obsessively anti-labour. the problem has been failure to regulate the banks, by both parties.0 -

I have something in the region of £50k of unsecured credit that is nicely boosting my income at the moment. Even consumers can borrow to improve their economic return.* It's making me something over 10% after any tax liabilities, before cost of borrowing. Net of borrowing costs might be over 10% also, haven't worked it out exactly.To use your mortgage analogy, people find it much easier to service their mortgage as their career progresses and their earning power increases. The difference with an economy is the borrowed money can be invested into things which bring about economic return.

*Provided their investment risk tolerance and capacity for loss are suitable for what they are doing, of course.0 -

The UK has extremely low borrowing costs and a far higher proportion of borrowing that doesn't come due for many decades than is usual. This greatly reduces the risk of running a deficit because there is much reduced prospect of a huge proportion of the debt becoming due rapidly.

For those who don't know it, one of the trends in countries with untrusted debt is that they can't refinance debt they already have for long terms and end up in a spiral of ever more costly debt at ever shorter terms until eventually they are issuing one month or even one week debt at unaffordable interest rates. Which is why a usual part of rescues is long term lower interest rate lending to reduce or eliminate the "you have to pay tomorrow" crisis moments as the shorter term debts for large proportions of the national debt fall due.

those problems relate to countries borrowing in a currency they don't control. e.g. many third-world countries have borrowed in US dollars. and of course, any country who uses the euro doesn't control their own currency.

when you have your own currency, as the UK does, the process of issuing gilts may look like the government is relying on the private sector to fund its deficits, but that is misleading. the BoE and the treasury are actually in control of the process.

for a start, although the usual practice is to issue gilts matching the deficit, they don't have to do it that way. they could always create bank reserves instead - i.e. if the treasury wants to spend £X (e.g. to pay a private sector contractor who is doing work for the State), the BoE could simply increase the reserves of the commercial bank where the contractor has a bank account by £X, and instruct them to credit £X to the contractor's account.

in fact, they go about it in a more roundabout way. very roughly: the BoE auctions £X of new gilts, probably to a commercial bank, who pays for the gilts by having their reserves reduced by £X; and then they increase those reserves by £X again, in order to allow the contractor to be paid. (there is also a lot of accounting covering transactions between the BoE and the treasury, which is IMHO better ignored, since both of them are fully owned by the UK, so discussing what 1 of them owes the other is pretty much meaningless.)

so you can fund a deficit by increasing bank reserves, or by increasing issued gilts, or a combination of the 2. (and the BoE can also swap bank reserves for gilts, or vice versa - e.g. QE was a process of creating £375bn or bank reserves, and eliminating £375bn of gilts.) but the BoE/treasury are in control of this process - it does not rely on the whim of the private sector.0 -

It can also happen where you control your own currency but there you have a not so secret weapon: you can deliberately increase inflation to deflate away the debt. Which is one part of what issuing more gilts does.grey_gym_sock wrote: »those problems relate to countries borrowing in a currency they don't control. e.g. many third-world countries have borrowed in US dollars. and of course, any country who uses the euro doesn't control their own currency.

There are limits to how far you can take this, as Zimbabwe discovered a couple of years back when they did a rerun of inter-war German inflation rates courtesy of massive money "printing".0 -

grey_gym_sock wrote: »the most informative of those graphs is debt-to-GDP ratio. that shows a sudden rise, entirely due to the financial crisis. in fact, the ratio even fell slightly under labour before the financial crisis hit (i.e. 1997-2007).

that labour government is certainly to blame, for its "light touch" regulation of the banks, which allowed the financial crisis to happen. of course, the tories were egging them on at the time, and even said there was still too much regulation.

but that was the problem. nothing to do with overspending on public services, or not raising enough in tax.

and the banks are still not regulated properly. so there is a big risk of another financial crisis.

for a start: pay it off how?

would you like to slash spending on public services now, so that you can raise it higher later, after the debt's been paid off? even if if that were a viable plan (which it isn't - see below), why would you even want to do that?

that is the nominal amount of interest. paying interest does not increase the debt-to-GDP ratio, unless the nominal interest rate paid is greater than the nominal growth in GDP.

but could the money be used for something more worthwhile?

no. because the UK is not working with a finite quantity of money. the State creates money. the cash we use as money came into existence from past UK governments spending more than they raised in taxes. paying interest on gilts has no direct affect on how much can be spent on public services.

the UK is only limited by real resources, not by quantity of money. if we want to spend on more health and education, the money to pay them can always be created. but if we want more ppl to work in those areas, they can't be working in other sectors at the same time. however, when a lot of ppl are unemployed or under-employed to start with - as they are now! - then cuts in other sectors may not be needed at all.

in the situation where you do need to free up resources from some sectors, then

a) if that's in the public sector, you just cut the spending;

b) if that's in the private sector, you raise taxes sufficiently to put ppl or businesses off from spending - but note that this doesn't usually require eliminating the deficit.

as above: it doesn't work like that. paying interest on gilts uses minimal real resources (i.e. a few officials in the BoE, to process the payments, and so on).

you are rather obsessively anti-labour. the problem has been failure to regulate the banks, by both parties.

Firstly I am not 'rather obsessively anti-labour.' There have been a stream of anti-Tory posts in this forum (including petty personal abuse directed at Tory politicians) which prompted my earlier post. You are right that the Tories were for some time egging on the Labour deregulation of banks.

Secondly it is well documented from first hand sources that during the Blair regime, Gordon Brown did his best to limit Blair by severely restricting spending. Once Brown took control, he unleashed public spending.

When you use phrase such as "if we want to spend on more health and education, the money to pay them can always be created." it makes me worry. We were on the way to having our credit status downgraded, which would have meant even higher debt repayment costs. That is why they 'slashed' spending, to use your emotive term. Ask yourself why the Liberal coalition partners were in agreement with the deficit reduction. It was not sustainable. I am sure an earlier post used the term 'investment'. The government uses that term to avoid saying spending. Balls et al orignally talked about 'investing' our way out of the deficit. They eventually agreed that the deficit had to be cut dramatically.0 -

What about economic growth?

Like inflation it erodes the burden of the debt pile.

To use your mortgage analogy, people find it much easier to service their mortgage as their career progresses and their earning power increases. The difference with an economy is the borrowed money can be invested into things which bring about economic return.

Your analogy bears no relation to the reality since 'investment' in government speak means spending, and the public spending is largely for services such as healthcare, policing and pensions. Clearly services such as education do bring about an economic return, but over a very long time period, and it remans to be shown what result a 5% increase in spending would bring as an 'economic return'. Clearly it has a social return, but that was not the point made in your post.0 -

BananaRepublic wrote: »Firstly I am not 'rather obsessively anti-labour.' There have been a stream of anti-Tory posts in this forum (including petty personal abuse directed at Tory politicians) which prompted my earlier post. You are right that the Tories were for some time egging on the Labour deregulation of banks.

Secondly it is well documented from first hand sources that during the Blair regime, Gordon Brown did his best to limit Blair by severely restricting spending. Once Brown took control, he unleashed public spending.

When you use phrase such as "if we want to spend on more health and education, the money to pay them can always be created." it makes me worry. We were on the way to having our credit status downgraded, which would have meant even higher debt repayment costs. That is why they 'slashed' spending, to use your emotive term. Ask yourself why the Liberal coalition partners were in agreement with the deficit reduction. It was not sustainable. I am sure an earlier post used the term 'investment'. The government uses that term to avoid saying spending. Balls et al orignally talked about 'investing' our way out of the deficit. They eventually agreed that the deficit had to be cut dramatically.

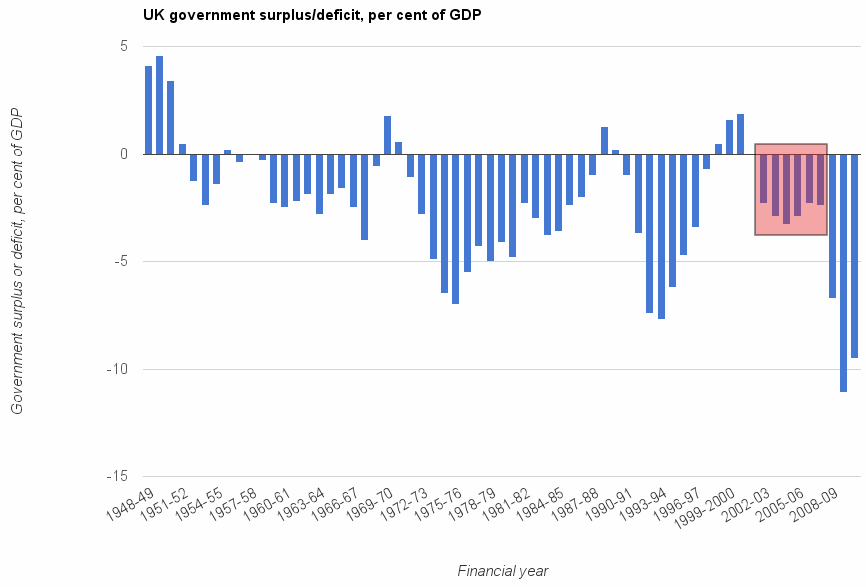

Looking at the following links the public finances wouldn't have been any different today whoever had been in power 10 years ago.

In 2007 just months before the financial crash the Tories were backing Labours spending plans despite Labour running a budget deficit in a growing economy.

http://conservativehome.blogs.com/torydiary/2007/09/tories-will-mat.html

http://news.bbc.co.uk/1/hi/uk_politics/6975536.stm

The area highlighted in red represents Labour borrowing around £150-£180Bn during a period where they could have ran a balanced budget.

http://3.bp.blogspot.com/-u_6bLBEcvus/VIL2bc4et6I/AAAAAAAAB70/hmWudWtqETU/s1600/Deficit,48-.png

On this link it shows there's hardly been a balanced budget since the early 1970's.

Even when the Tories had been in power from 1978 things turned against them in the early 1990's and the budget deficit climbed again.

Their forecasts in 2010 highlighted in green again have been way out as the downturn has proved difficult.

https://www.flickr.com/photos/hmtreasury/5260056945/0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards