We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Investments and Returns - Example

Comments

-

Of course this is true insofar as the AMC/TER/OCF has come down for OEICs, but of course there are lots of costs not included in those charge figures. Pre-RDR, I seem to recall the total cost of funds being estimated at around 5%, when things like portfolio churn were taken into account, but it is quite difficult to obtain the required information to establish these hidden costs for OEICs, whereas ITs generally have greater transparency in what they report to the market regarding expenses.Historically one of the main reasons to buy investment trusts has been the lower cost but since RDR (and before that fund supermarket discounts) this has largely disappeared and there is little if any difference and some are now higher than the equivalent OEIC.0 -

I think it was clear in the OP that JJ did not pick this fund in hindsight - this is an actual investment chosen many years ago. However, it's worth pointing out that picking a single fund with a narrow investment objective is a high risk strategy for the reason you illustrate. I'm fairly sure none of those funds got a mention here 5 years ago as ones people were investing in, so hopefully nobody held any of those funds.

Interesting that some replies suggest I picked a fund that's done too well and others that it's done badly. Overall probably indicates it's a reasonable choice. Only reason I chose this investment was the report came through most recently and I thought the numbers looked like they'd be useful to others seeking income.Remember the saying: if it looks too good to be true it almost certainly is.0 -

It is certainly a post we can give a link to when coming across those needing income but afraid of investing anything and keeping 100% in cash.

AS it illustrates the point very well that as the fund itself goes up and down, the income it pays continues rising. And if only drawing income, this is the most important point.0 -

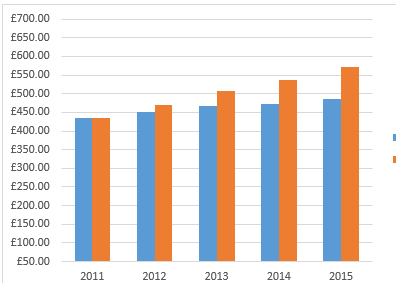

Just to put the dividend re-investment into context vs taking the income as cash;

With dividends re-invested;

Total income: £2,524.80

No. of shares at end: 1,788

End of period stock value: £12,605.40

With dividends paid out;

Total income: £1,825.58

No. of shares at end: 1,515

End of period stock value: £10,680.75

Orange = Dividends re-invested

Blue = Dividends taken as cash"If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” Warren Buffett

Save £12k in 2025 - #024 £1,450 / £15,000 (9%)0 -

This article reminded me of the thing that I find frustrating after investing in a number of accumulation unit -Investment funds. I do like to monitor my investments and thought I would get an annual statemnet showing income re-invested but discovered that , not only did this not happen, but it was pretty impossible to calculate. With Investment funds, the re-invested income does not buy new shares or units but is just reflecetd in the value of each unit which is then subject to the normal ups and downs of the market. Although I opted for funds, I wish there was a similar way to track returns and the effect of re-invested income clearly shown by the additional number of shares in a trust.0

-

Funnily enough I have the same issue.0

-

It's a great post, but how do you choose your investment trust? How do you know you are making a good choice when you do? How would these figures compare to a world stock market ETF?

Eg. Vanguard FTSE All World USD, VWRL, +40.5% since inception on Jun 1st 2012.

£10000 invested then would be worth £14053 now, more if dividends reinvested0 -

I think these are the essential questions every investor has to be sure about before they go for active ITs ahead of passive index funds.It's a great post, but how do you choose your investment trust? How do you know you are making a good choice when you do? How would these figures compare to a world stock market ETF?

The ITs performance can only be as good as the expertise of the manager - stock selection, timing, borrowing decisions, view on certain sectors etc.

I suppose we all like to believe we can select the best manager(s), just as the managers of the ITs believe they can regularly outperform their respective benchmarks - some do but many do not so at the end of the day its a bit of a lottery.

In reality however, the markets are very efficient. All the empirical evidence over decades shows that beating the market consistently after costs through skill or judgement is very difficult. The fund managers who can do this are rare and are very difficult to identify in advance.

This is why I now prefer globally diversified index funds, particularly the Vanguard LifeStrategy range.We have a climate emergency and need to re-think investing strategies to avoid sectors that are part of the problem such as oil & gas and embrace climate-friendly options such as renewable energy.0 -

I think these are the essential questions every investor has to be sure about before they go for active ITs ahead of passive index funds.

The ITs performance can only be as good as the expertise of the manager - stock selection, timing, borrowing decisions, view on certain sectors etc.

I suppose we all like to believe we can select the best manager(s), just as the managers of the ITs believe they can regularly outperform their respective benchmarks - some do but many do not so at the end of the day its a bit of a lottery.

In reality however, the markets are very efficient. All the empirical evidence over decades shows that beating the market consistently after costs through skill or judgement is very difficult. The fund managers who can do this are rare and are very difficult to identify in advance.

This is why I now prefer globally diversified index funds, particularly the Vanguard LifeStrategy range.

The way I see it, it's not only about fund managers try to/do pick great stocks (positive stock screening) but it's also that they can avoid certain stocks (negative stock screening).

Looking at what's happened over the past 12 months, natural resources/commodities/oil stocks have had a torrid time. The index trackers are stuck with these stocks (look at the ftse 100's heavy weighting to miners), any half decent IT manager would not be holding these commodity stocks.

I'd be interested to see what the performance of FTSE 100 (ex miners and oil companies) would look like."If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” Warren Buffett

Save £12k in 2025 - #024 £1,450 / £15,000 (9%)0 -

homerhotspur wrote: »This article reminded me of the thing that I find frustrating after investing in a number of accumulation unit -Investment funds. I do like to monitor my investments and thought I would get an annual statemnet showing income re-invested but discovered that , not only did this not happen, but it was pretty impossible to calculate. With Investment funds, the re-invested income does not buy new shares or units but is just reflecetd in the value of each unit which is then subject to the normal ups and downs of the market. Although I opted for funds, I wish there was a similar way to track returns and the effect of re-invested income clearly shown by the additional number of shares in a trust.

If you choose INC units and reinvest then you will see the income used to buy more units in the fund and your holding increases. Acc units will increase fund value without you knowing how much by.Remember the saying: if it looks too good to be true it almost certainly is.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards