We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

What do you think of my asset allocation?

Comments

-

Having read threads started by people determined to get rich by backing their stock-picking skills (aka luck)

As Malkiel himself says: "It's called the Efficient Market Hypothesis; not the Efficient Market Truth"

As an investor, you can choose the level of risk/volatility you want to expose yourself to, and this will tend to dictate the level of returns

http://en.wikipedia.org/wiki/The_Superinvestors_of_Graham-and-Doddsville0 -

bowlhead99

- thanks for your detailed comments. On the subject of currency exchange rate risk, you've given me a new perspective that I hadn't thought about.

Ryan Futuristics

- thanks for your comments. I'm planning to drip-feed my contributions into my ISA on a monthly basis. Your per-region small caps comment is interesting, but I'm not sure I can find suitable funds on the platform I'm using (or even on any platform). Also, the ammount I have to invest is such that if I choose much more than the 7 funds I've already mentioned then I'd be in danger of not being able to meet the minimum monthly contribution per fund. I could follow another posters advice given to me on a different thread where they suggested investing in different funds on alternate months. That would take more effort though, since I'd have to manually make regular lump sum investments rather than just setting up an automatic monthly direct debit (or I could auto direct debit into cash within my ISA and then manually transfer to funds as/when appropriate).

Re: your comment about Europe, I had noticed that some countries within Europe have quite high CAPE whilst others not so high. As with the regional small caps thing, I'm not sure I could find separate funds or would have high enough contributions to be investing in multiple funds within Europe in addition to the other regions.

Re: value stocks, do you have any particular funds in mind? I noticed that in my copy of "Smarter Investing, Third Edition" by Tim Hale (page 172) it lists the following fund as "Global developed equity (value)":Legal & General Global 100 Index TrustHowever, when I looked up the details for this fund, it apparently tracks "the performance of the S&P Global 100 Index, converted into Sterling". When I then looked up the S&P Global 100 Index, it appears to track 100 large cap companies. I'm not sure where the "value" comes in?

I thought that "value stocks" were shares in companies whose share price has been excessively reduced as a result of some event (e.g. profit warning or change in business environment), such that some investors perceived a buying opportunity based around the belief that the shares were now under-priced and therefore a bargain. The top 10 holding (approx 32 percent of the fund) are made up of companies that I imagine would be included in the S&P500 tracker that I listed in my original post (Fidelity Index US Fund P-Acc).

The "Smarter Investing" book also listed the following fund as being "UK equity (value)":iShares FTSE UK Dividend PlusThe nearest I could find to this on my platform is:iShares UK Dividend UCITS ETFThis looks like a "high yield" fund. I'm certainly not an expert, but whenever I've looked at high yield funds, it seemed like over the long term they don't perform any better than a broader market index fund (e.g. FTSE All-Share or S&P500). Then I remember a quote I heard somewhere:"Chasing yield is like picking up pennies in front of a steam roller!".With the above in mind, I'm not convinced it's worth the extra complexity of adding in "value stocks" funds. If you've got any particular fund in mind, I'd be interested to hear about it although I'm not sure it would change my mind.

By the way, I'm not criticising the "Smarter Investing" (by Tim Hale) book. I really enjoyed reading it and I still think it's an excellent book.

Re: Your comment:"Consider diversifying by investment style as well as region ... Growth and value stocks perform differently over lengthy periods ... As does active and passive management"I see your point, and I chose the "Vanguard Global Small-Cap Index Acc" fund as a step in that direction. However, I've struggled to find many funds in the areas of small cap and value stocks, and I'm very much a believer in passive tracker funds that have low charges, as opposed to the (usually) more expensive managed funds.

Thanks.

Disclaimer: I am not an expert. My comments are my opinions only and should not be taken as advice. Any information I post may or may not be correct, and should therefore not be relied upon as fact. If you act on anything I post here you do so entirely at your own risk. I do not accept any liability.0 -

Well I think the idea of keeping it to 7 funds is probably sensible

Personally I avoid ETFs when we're talking ISA-level contributions, as dealing charges and bid-spreads can add quite a bit of friction (especially when rebalancing) ... So I think OEICs generally make a lot of sense in ISAs

And yeah, the idea is dividends can be a reasonable assessor of value (as they tend to go up as share prices go down); but they also go up when a company's in trouble ... I've got Vanguard's UK Equity Income tracker, and it's done quite a bit better than the All Share index over the period I've held it ... But my main reason for preferring dividend stocks is that interest rates have a way to rise before we can get back to 'normality', so bonds may be out of favour for a while (especially after the Fed hikes the rates, presumably this summer) ... So that should keep demand for dividend stocks high for years

I'm not familiar with that global value fund, but value stocks *may* merely track broader indexes at the moment - QE has meant virtually no automated strategy or approach has outperformed since 2009 - but for me, value is one area where a more flexible, active management approach may deliver

What I often like to do to assess value is go to MorningStar, look up the fund, then in the Portfolio section, look at whether the P/E ratio is below the combined value of Forecast Growth and Dividend ... It's a crude ratio that works reasonably well (called a PEG or PEGD ratio)

My personal preference would be to choose passive where it's more likely to deliver, and choose active where it's got a better shot (with the bonus that you should get more exposure to small and medium companies, as well as value stocks if you select carefully)

In the US and Japan, there seem to be fewer reasons to use active funds - almost nothing's outperformed the S&P500 in years ... But in Europe, Asia and Emerging Markets (where you get wildly different valuations across regions, and a lot of possible divergence between regions and sectors) active has often been a smarter move

Good paper analysing active vs passive in Emerging Markets

http://www.robeco.com/images/on-the-performance-of-active-versus-passive-emerging-marke.pdf

For Europe I like Argonaut European Alpha, Neptune European Opportunities, and Sanditon European, but comparing their P/E and Growth forecasts on Morningstar vs the passive option may be wise ... Or you may just prefer to go passive ... I'd say there's a 50:50 of funds like Neptune outperforming (based on whether QE benefits central or peripheral Europe more), but if they do, there's a lot of potential scope for outperformance

Interestingly that Vanguard Small Cap fund doesn't look great on simple valuation

http://www.morningstar.co.uk/uk/funds/snapshot/snapshot.aspx?id=F00000UDXU&tab=3

Presumably because of the high allocation to US shares ... It's not *impossible* that US shares could just continue to rise diagonally forever though - if the central bank's going to keep pumping the money in whenever they start to drop

But I wouldn't bet the house on it ... It's also not impossible that much of the European QE money could wind up inflating US shares further - if investors still aren't keen to invest in Europe

But I think what most literature tells us is these kind of predictions always lead to us over or underestimating risk, and harms returns - so I always bring it back to value

http://www.starcapital.de/research/stockmarketvaluation?SortBy=Shiller_PE

This would be personal bias, but I'd probably replace Asia, Europe and Emerging with cheap, Silver or Gold-rated actives (take care of the small and medium cap exposure too), and perhaps go 50:50 on a FTSE All Share tracker and Woodford Equity Income (which I think is almost guaranteed outperformance, if only because so many fund managers and investors copy what Woodford does now)0 -

Ryan_Futuristics wrote: »PROS:

- Good allocation to Emerging Markets ... They represent over 50% of the world's GDP, and population, while developed world growth slows and population ages

CONS:

With the real risks being political, corporate governance and liquidity.

Sometimes boring and defensive is the proven way to invest over the long haul.0 -

Thrugelmir wrote: »CONS:

With the real risks being political, corporate governance and liquidity.

Sometimes boring and defensive is the proven way to invest over the long haul.

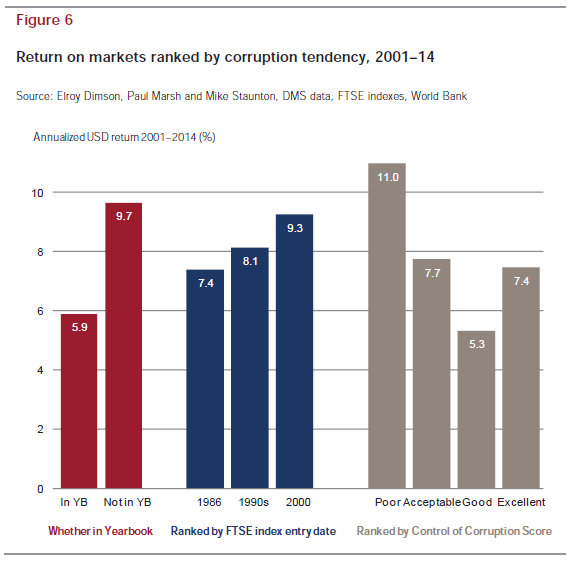

If you've read your Graham and Doddsville: the biggest risk is always high valuations

And interestingly, areas with higher corruption and less governance have in fact tended to return higher (again, most likely due to higher valuations where people deem there to be lower risk) 0

0 -

Even if you haven't read a single issue, it's common sense that buying something that turned out to have been expensive will not have been as good as buying the same thing less expensively.Ryan_Futuristics wrote: »If you've read your Graham and Doddsville: the biggest risk is always high valuations

If you buy something and then a risk event happens (the company implodes, a world war starts, a rival invents the cure for cancer before you do) you can always say you paid too high a value relative to all the things that could go wrong, and if you bought at a better valuation (i.e. less money than you did) then you would have been at least partially insulated from the problem.

So, you can say that individually Thrugelmir's risks of poor governance, politics and an undeveloped illiquid market are not as important as the arbitrary construct that is 'valuation'. It does get tiresome to hear the same drum being beaten day after day though, as there are only two things to making money - what you pay for it and what you get from it. To hear someone constantly banging on about how if you simply ensure that you don't pay a lot for what you expect to get from it, you'll be successful, sure gets tiring. My 103-year-old grandmother could come up with that without even knowing what an equity portfolio is, much less a Doddsville.

Sure, you can go for these trailblazingly corrupt and shaky areas and make money, because if you are not one of the unfortunate ones who loses all your money to state confiscation, or to a rival who bribes your industry regulator, then you could make an absolute fortune. You will spin that as 'safe' areas are overvalued and 'up and coming' areas are cheap and therefore it is a "valuation play" to go to the up and coming areas.And interestingly, areas with higher corruption and less governance have in fact tended to return higher

However it is simple risk and reward. If you can stomach the losses, then sure, take more risks and get in bed with the terrorists and the thieves and the companies that don't know what an independent non-exec director is supposed to do other than smile and take the cash. If you get away with it, then when it pays off it really pays off.

Because the risk is high, and nobody wants it, it is cheap. If you hold for the long term to ride out the peaks and troughs, there can be good returns. But I don't really read that type of investment as 'buying value for money'. It's simply a hop along the risk scale to a different type of investment.

If you can get similar risk and similar returns to a mainstream investment for less pounds, you are getting value. Whereas if you want to walk where others fear to tread then by allocating your cash to the dodgiest companies using a "corruption perceptions index" you might be able to buy many many companies for less pounds with huge risks but it doesn't strike me as something we should all strive for.

If you take your cues from Buffet he is going to tell you to buy quality for low money if you can, but not be afraid to pay good money for a quality company. Whereas allocating your money to the dodgy locations because they historically did better than the safe markets is not a value play (lots of dividends per pound invested) it is a high risk play (lots of dividends if the company still exists in a year and isn't a front for a drugs racket)

In putting together a graph of "returns from corruption", and thinking, ooh, interestingly... you have to consider to what extent it's correlation rather than causation.

Interestingly I was on a plane the other day and every time the captain switched on the seatbelt sign it got bumpy. On the way back I'm going to ask him not to switch the seatbelt sign on so we can have a smooth ride.0 -

Thrugelmir wrote: »CONS:

With the real risks being political, corporate governance and liquidity.

Sometimes boring and defensive is the proven way to invest over the long haul.

My view is that these are not so much Cons as facts, and these facts represent risks that affect equity prices, and that people tend to value the risks as a discount, and investing in this discount for the long term represents a return premium. As a side effect and bleeding obvious, value metrics are low as a result of overestimated (in the long term) risks and underestimated growth. Of course studies of EM show a value premium but in my opinion saying one should invest in EM for the value factor confuses cause and effect and dilutes discussion of the value premiums in developed markets.

OP, there are no great Value trackers around. I hold (not just "like")- Vanguard FTSE UK Equity Income Index (VVUEIN) OCF 0.22%, initial fee 0.4%

- Vanguard FTSE All World High Dividend Yield ETF (VHYL) OCF 0.29%

I hope better trackers come about but these will do me for now.0 -

@bowlhead: This is why I prefer data and strict investing rules ...

We can speculate all day over issues like risk and corruption (bearing in mind most of you UK passive investors are holding HSBC, which is currently being fined for gross corporate corruption), and all the evidence tells us you're probably harming your returns doing so

Our biases and perceptions are always off - we pile into growth sectors, ignoring fundamentals, while the news ensures we price in every macroeconomic risk factor as if the worst case scenario's already happened

This is why markets are constantly over and undershooting, and needing to 'correct' periodically

What Buffett and co. make clear is that we tend to have it backwards ... The real risk of being in the markets plays out in US stocks just as often as anywhere else; the difference is that risk is much better priced into emerging regions at the moment - we've had the corrections the US market should've been getting (if it weren't plumped up with magic money)

And I'm not talking about buying shares in Al Quaeda; emerging markets cover companies like Samsung, Taiwanese Semiconductor Manufacturing, Baidu ... These are in my top 10 holdings; HSBC isn't0 -

I'm not sure that's the case. Risk is better priced in is a blanket statement. The fact there has been some corrections in some EMs (after they had a bigger run up than developed markets) doesn't mean that now all of a sudden they are at a fair price and US is at an unfair price.Ryan_Futuristics wrote: »the difference is that risk is much better priced into emerging regions at the moment - we've had the corrections the US market should've been getting (if it weren't plumped up with magic money)

You can't seriously think that the 'plumping up with magic money' is not deeply embedded in the price of EM stocks today. Since the pre-credit crunch highs seven or eight years ago, the proportion of domestic EM bonds in foreign ownership has probably doubled for example, and the overall market caps in EMs have grown massively over what they were a couple of decades back, thanks partially to a decade long commodity boom which no longer exists and partially due to Western risk seeking. As your corruption chart showed, people 'piled in' to those newer entrants and less developed markets (ignoring the fundamental risk factors such as corruption and the immaturity of the markets), taking great returns from them.

Huge swathes of easy money have flowed from developed to developing markets which has financed infrastructure, corporate investment, consumerism. When the taps get turned off we see who's swimming naked (a mangled Buffett-ism), and certainly the finance houses who were keen to risk seek in EM when everything was rosy in the USA will not be doing it to the same extent when things are not rosy in the USA. There is a bit of a stay of execution while US taps get turned off if Japan taps are still on and Europe taps start opening but EM is not 'better priced'. It is simply, more cheaply priced if you look at current earnings, and there is a reason for it ; the pricing is not happening without any kind of nod to reality - it is driven by reality.

If you were an American with the free money being turned off and the prospect of a relatively strengthening currency it would not be at all a no brainer to go and invest it in the part of the world where markets are less mature and have been propped up by your countrymen who now want their dollars back.

Back on topic to the OP - it is right that 'value' funds in terms of value vs growth tend to be the ones that are paying out dividends. The argument being with a value tilt you are getting nice income streams for your money while with a growth tilt you are not seeing the income come through and you're relying on some future wealth creation that you can't see yet but hope continues. So, it's not surprising that Hale describes a high div fund or a fund made of the largest 100 rather than the smallest 100 in an index, as 'value' versus high growth.

'High yield' is something that can mean something a bit different, e.g. in the bond world it can refer to junk bonds that have to pay out high yields to get people to invest in them as they re fundamentally more risky than 'investment grade' corporate bonds. High yielding bond funds are therefore perceived as riskier than 'normal' corporate bond funds or government debt funds. While equity funds that pay higher yields by contrast are thought of as a bit more defensive because there is reliable income coming in.

It is hard to have reliable 'value' trackers because it is hard for a computer screening tool working off a formula to say whether a company is great value ; it might think a company meets the criteria because its share price is now only 10x its last dividend instead of the 30x it used to be, but needs to consider whether the dividends are sustainable and whether the company is simply priced cheaply because it's going bust rather than because it represents good vfm. It is quite hard for trackers to do that, one would think. But they are certainly more sophisticated than they used to be.0 -

Feb 24:Ryan_Futuristics wrote: »And I'm not talking about buying shares in Al Quaeda; emerging markets cover companies like Samsung, Taiwanese Semiconductor Manufacturing, Baidu ... These are in my top 10 holdings; HSBC isn't

Feb 23:Ryan_Futuristics wrote:I've got Vanguard's UK Equity Income tracker

Vanguard UK Equity Income's top holding is 4.9%. HSBC is 4.7% of the fund.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards