We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

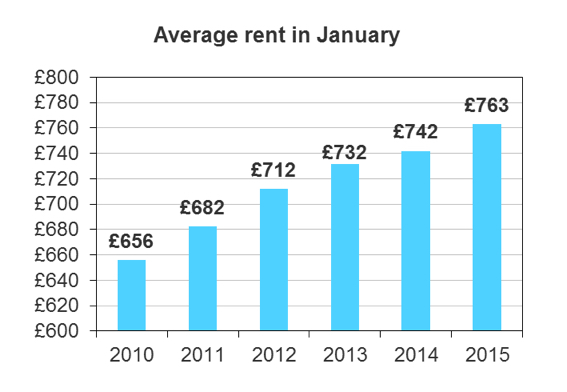

If house prices fall rents will rise. Why don't crashtrolls get this?

Comments

-

HAMISH_MCTAVISH wrote: »

Just for reference, average mortgage repayments were about £666 in Feb 2014...Research by the Centre for Economic and Business Research (CEBR) found that average mortgage payments across the UK could rise from their current monthly levels of £666 per month to £687 a month in the most likely scenario. This would add an extra £21 a month to payments, or £252 a year.

I assume that includes capital repayment.0 -

Loughton_Monkey wrote: »Blimey! Not many would fall for this argument, although it does smack of a better excuse than "I simply can't afford a house or can't be bothered to save a deposit....."

Do the maths.

An excuse for not buying? This is a weird attitude, its up to the individual whether they buy or not, you don't actually have to you know!!!!! No-one is under any obligation to buy!!! :rotfl:

Take the must buy blinkers off, theres a whole world out there, whats right for some is not right for others. I did the maths, Im happy with my choices. Ease of moving for work was the key for me, I made more than a house would.

Very narrow minded view you have, why don't you leave people alone who make their own decisions and are happy with them?

I wonder about some of you people sometimes on forums trying to tell everyone over and over and over how happy you are you did something as pedestrian as buy a house. Woop de fking doo. Are you looking for approval or what?

Different people have different situations and what is right for one isn't necessary right for another. I accept both renting and buying is valid depending on circumstances, why don't some of you? Buyers remorse? The more I read people desperately seeking approval for buying the more suspicious I get about how happy they actually are with their choices. Aren't you supposed to be "getting on with your life" by now?

You can rent first and buy later too, its not one or the other for life. Weird thing to argue about with such bitterness, with such a mocking tone. I wonder why some of you are so angry and use up such energy on this? Im perfectly happy! Am I daring not to conform to your housing plan? How dare I. And be better off doing it too! What cheek!

Chill out, you've got your precious house. Have a peanut.0 -

westernpromise wrote: »My point, re the bold above, is that this market-set upper limit is often assumed to be static, as though that were self-evident, and hence a reason why rents cannot rise. In fact, it's anything but static.

I agree, and I addressed that when I said

"I agree the costs are not fixed in either case but the bounds within which they can suddenly move and indeed the suddenness of that movement is very different when comparing renting to buying, where renting plainly is the better circumstance."westernpromise wrote: »So over time rental yields have clearly fallen. This happens because homeowning (which offers capital gain) is more attractive than renting (which doesn't).

I believe it is more about lower mortgage rates, you can borrow more when rates are lower so can pay more for the same house. Capital gain is an assumption, depends on area and in what time period, many landlords have seen little capital gain for years away from london.westernpromise wrote: »If you were on £10k a year in, say, 1970, you could have afforded a £30k house. Today your £10k salary would equate to about £250k, and that would buy you a £750k house on the same salary multiple.

The £30k house of 1970 cannot today be bought for £750k. It would be more like £2 million.

Interest rates again, and when they go up the amount that can be borrowed goes down, so houses will sell for less. If you look to the past for guidance remember that now we have buy to let which is relatively new. A lot more rental property now, they all want tenants in a downturn… I agree thatwesternpromise wrote: »if needs must people will settle for less

There are lots of rental properties now and lots of empty rooms back at boomer mum and dads house.

I am not as confident as you about your predictions of higher rents but we will all find out in time.0 -

Higher rents.....:rotfl::rotfl::rotfl:0

-

Crashy_Time wrote: »Higher rents.....:rotfl::rotfl::rotfl:

I've just had a look at Citylets and it definitely looks like I'll be able to charge my next set of tenants more rent :beer:0 -

-

Crashy_Time wrote: »Lost the last lot already?

Nope, but presumably they will eventually move out.0 -

Crashy_Time wrote: »Higher rents.....:rotfl::rotfl::rotfl:

The converse has already been observed. You've observed it yourself; house prices in your area have risen, but your rent has not.

I hope you don't think rents can only stay the same or go down.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards