We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

If house prices fall rents will rise. Why don't crashtrolls get this?

Comments

-

Crashy_Time wrote: »I said I am paying £50 p.m more for a similar flat than I was 15 years ago.

This kind of anecdata completely supports the original contention in the top post.

Over time, if the capital value of property goes up, the cost of renting proportionately falls. This is because the tenant's alternative to renting is the much more economically attractive route of buying, and seeing some capital gains. So they do that instead, and so rental demand is suppressed.

So we have one side of the coin: rising capital values = falling or stagnating rental yields.

The other side of the coin, as we observed in the early 90s, is that falling capital values means rising rents.

The tenant in such a market has no bargaining position. It's either pay up what the landlord wants, or quit renting and become an owner instead. At this point, the tenant takes on all the exposures the landlord has.

Crashtrolls who've hopelessly misjudged the property situation these last 20 years, and who hope desperately for a house price crash that will finally prove them right, need to get real. Any such crash will send their rent through the roof as lots more people pile into renting (more demand) and bid rents up to escape the risk of capital falls.

If you've been saving, kiss it goodbye; your landlord's getting it.

The idea that, as landlords exit, crashtrolls will snap up a bargain, and a home-owning nirvana will thereby return, simply doesn't hold water. Crashtrolls are afraid of buying at any level. They have been holding back from buying, and insisting property prices were about to crash, for about 20 years now - since the end of the last crash.

Are these people going to pile in and start buying as soon as prices decline? No, they'll insist houses are still overvalued and have further to fall no matter how far they have just fallen.

In 1996 what happened was that crashtrolls stayed away from buying and bid rents up; landlords then piled in, bought cheap houses and let them out at an instant profit to crashtrolls. Something similar is the likeliest outcome of any price correction (not that I expect one).

It's a huge mistake to pay any attention to any crashtroll.0 -

Jack_Johnson_the_acorn wrote: »I'll be mortgage free before I'm 40.... Whilst you in your genius renting plan would still be in a Hmo sharing a bog..... On the outskirts of Edinburgh. It's understandable why you're so bitter, I'm looking forward to having that extra £600pcm in my back pocket for the rest of my life... where as you'll be paying another happy LL's mortgage off at this point. I've also got considerable savings and a public service fs pension.... You seem to think that only renters can save, where as in the real world, if renters could save, they would have a deposit saved by now and be looking for their perfect home.

:rotfl: Only Hamish coming out and saying Aberdeen will never crash could be funnier than that!0 -

-

westernpromise wrote: »Your typical crash troll seems to imagine that by renting he'll avoid all risks and his housing cost will stay the same. Not true.

A cost is paid for housing in either case but they the two options have pros and cons. You cannot rationally argue that one is better than the other without taking a persons circumstances and ambitions into account. Every situation is different.

You don't avoid all risks when renting, and you have some new ones versus buying. And vice versa.

The differences are obvious, ease of moving for work or to get away from a problem neighbour or new development etc, insecurity of an AST, being exposed to the property market in a leveraged fashion good or bad you decide, being exposed to maintenance risk or not, lease complications, updating your home if you want, blah blah. It goes on.

Pros and cons. If you want to talk about financials in isolation then the ease to move for work is also a determining factor, not just what the property market or interest rates do.

As to the main point quoted above about exposure to higher housing costs when renting as well as buying, well the total amount that can be charged by a landlord is the total amount that can be paid, affected by local employment, cost of living in other areas, all of that. The market sets the upper limit. When borrowing with a mortgage you take a long term bet on house values and interest rates, if these move against you, you have some money to find whether you can afford it or not, and you can't easily get out of that situation like a renter can if a proposed, note proposed, rent increase is attempted. I agree the costs are not fixed in either case but the bounds within which they can suddenly move and indeed the suddenness of that movement is very different when comparing renting to buying, where renting plainly is the better circumstance.

This renting versus buying talk is over simplified, it all depends.0 -

allthingsmustpass wrote: »A cost is paid for housing in either case but they the two options have pros and cons. You cannot rationally argue that one is better than the other without taking a persons circumstances and ambitions into account. Every situation is different.

You don't avoid all risks when renting, and you have some new ones versus buying. And vice versa.

The differences are obvious, ease of moving for work or to get away from a problem neighbour or new development etc, insecurity of an AST, being exposed to the property market in a leveraged fashion good or bad you decide, being exposed to maintenance risk or not, lease complications, updating your home if you want, blah blah. It goes on.

Pros and cons. If you want to talk about financials in isolation then the ease to move for work is also a determining factor, not just what the property market or interest rates do.

As to the main point quoted above about exposure to higher housing costs when renting as well as buying, well the total amount that can be charged by a landlord is the total amount that can be paid, affected by local employment, cost of living in other areas, all of that. The market sets the upper limit. When borrowing with a mortgage you take a long term bet on house values and interest rates, if these move against you, you have some money to find whether you can afford it or not, and you can't easily get out of that situation like a renter can if a proposed, note proposed, rent increase is attempted. I agree the costs are not fixed in either case but the bounds within which they can suddenly move and indeed the suddenness of that movement is very different when comparing renting to buying, where renting plainly is the better circumstance.

This renting versus buying talk is over simplified, it all depends.

Great post, very refreshing compared to the usual Buy Buy Buy drivel.0 -

allthingsmustpass wrote: »A cost is paid for housing in either case but they the two options have pros and cons. You cannot rationally argue that one is better than the other without taking a persons circumstances and ambitions into account. Every situation is different.

You don't avoid all risks when renting, and you have some new ones versus buying. And vice versa.

The differences are obvious, ease of moving for work or to get away from a problem neighbour or new development etc, insecurity of an AST, being exposed to the property market in a leveraged fashion good or bad you decide, being exposed to maintenance risk or not, lease complications, updating your home if you want, blah blah. It goes on.

Pros and cons. If you want to talk about financials in isolation then the ease to move for work is also a determining factor, not just what the property market or interest rates do.

As to the main point quoted above about exposure to higher housing costs when renting as well as buying, well the total amount that can be charged by a landlord is the total amount that can be paid, affected by local employment, cost of living in other areas, all of that. The market sets the upper limit. When borrowing with a mortgage you take a long term bet on house values and interest rates, if these move against you, you have some money to find whether you can afford it or not, and you can't easily get out of that situation like a renter can if a proposed, note proposed, rent increase is attempted. I agree the costs are not fixed in either case but the bounds within which they can suddenly move and indeed the suddenness of that movement is very different when comparing renting to buying, where renting plainly is the better circumstance.

This renting versus buying talk is over simplified, it all depends.

My point, re the bold above, is that this market-set upper limit is often assumed to be static, as though that were self-evident, and hence a reason why rents cannot rise. In fact, it's anything but static.

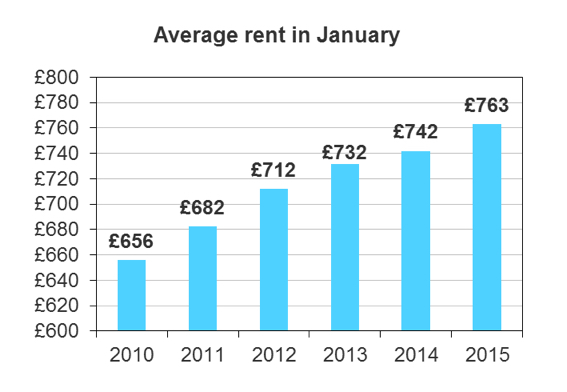

Rents have moved little over the last 10 to 15 years relative to capital values. The flat I rented for £1400 in 1999 I now own, and it lets for £2600 a month. The rent has not doubled, but the value has more than tripled. We also have Crashy Troll in this thread observing that his / her rental housing cost in Scotland is about the same now as in 1998. So, higher house prices, but rents the same or higher by less.

So over time rental yields have clearly fallen. This happens because homeowning (which offers capital gain) is more attractive than renting (which doesn't). And this holds down rents. The upper limit on what people would pay has been falling.

In a falling house price market, demand to buy has already collapsed. The number of people hasn't changed, so this demand has nowhere to go except towards renting. Consequently, the price of renting rises.

If someone has £1,000 a month to spend on rent, they'll still have £1,000 a month to spend on rent in this scenario. The problem is that the highest bid to live in their 2-bedroom flat won't be £1,000 any more. It'll be £1,500, from someone who's been displaced from a 3-bed where the rent demand has just gone up to £2,000. and so on.

That someone will still spend £1,000 a month on rent, they'll just get less for the same money.

If you doubt this, consider that this is precisely what has happened in the owned market.

If you were on £10k a year in, say, 1970, you could have afforded a £30k house. Today your £10k salary would equate to about £250k, and that would buy you a £750k house on the same salary multiple.

The £30k house of 1970 cannot today be bought for £750k. It would be more like £2 million.

In your model of fixed demand that outcome shouldn't be possible. What you're overlooking is that if needs must people will settle for less. If I am only prepared to borrow 3x my salary I am going to get less house.

Same will happen with rents, exactly like last time.0 -

allthingsmustpass wrote: »A cost is paid for housing in either case but they the two options have pros and cons. You cannot rationally argue that one is better than the other without taking a persons circumstances and ambitions into account. Every situation is different..........

...........

This renting versus buying talk is over simplified, it all depends.

Blimey! Not many would fall for this argument, although it does smack of a better excuse than "I simply can't afford a house or can't be bothered to save a deposit....."

Do the maths. Put in a few 'googleys' from time to time to factor in the cost of moving if you need to move for your job...and you will never make a convincing argument.

Put in the cost of a 25 year mortgage. Interest and repayments of the fixed sum. Now put in the cost of renting for 55 years. Inflating. Ignore the value of the house. Assume it crashes to zero the day before you die. And it's still better to buy.

You sound like someone who would put £10 a week into a shoe box in the wardrobe as your 'pension' rather than allow your employer to 'match' your own 5% contribution into a proper pension fund. Your argument might go like this.....

1. OK, I lose 5% from my employer but I don't have to choose funds or sign a piece of paper.

2. OK, I lose 20% tax relief as well, but I don't have to look up my pension value on the Internet, or read annual statements. I can go to the wardrobe any day and count my money.

3. OK, I lose the average 7% growth, but my employer wouldn't allow me to miss one month, and double it up the next month.0 -

Here's a thought, one in five properties in the UK are owned by buy to let landlords.

The economy was very fragile in 2008, house prices crashed somewhat but government policies ensured they didn't properly.

They also ensured that very few of these buy to let businesses went bust, which seems quite wrong as it's surely only right that those who are over leveraged the most, should suffer the biggest consequences?

Now they've all benefited from a period of extremely low interest rates, which must have made many very rich, especially as rents haven't come down much have they?

http://www.telegraph.co.uk/finance/personalfinance/investing/buy-to-let/11179073/Buy-to-let-boom-one-in-five-homes-now-owned-by-landlords.html0 -

“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0 -

HAMISH_MCTAVISH wrote: »

Yeah, it was more meant sarcastically though so I do agree. :-) Rents haven't come down, they've gone up. What is the source there though?

That 1 in 5 figure above by the way is from 2014. This figure has increased by quite a bit since 2008, infact the vast majority of new builds for example in the last 10 years or so I think have been bought by buy to let landlords.

Don't forget too the funding for lending scheme - which is a government scheme designed to help banks lend out to small businesses at cheap rates, to the cost of tens of billions of pounds. A lot of those small businesses are buy to let. The scheme has even been extended recently. Go figure...0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards