We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Young hit hardest in recession

Comments

-

HAMISH_MCTAVISH wrote: »Well they could always try building more houses....:cool:

Give them a chance!")

I suspect they will be more focussed on planning to disgrace this country by withdrawing from the Human Rights Convention. Not my view but the former Attorney General's it seems.

http://www.bbc.co.uk/news/uk-politics-28315517

Now who will that disadvantage most, I wonder.Few people are capable of expressing with equanimity opinions which differ from the prejudices of their social environment. Most people are incapable of forming such opinions.0 -

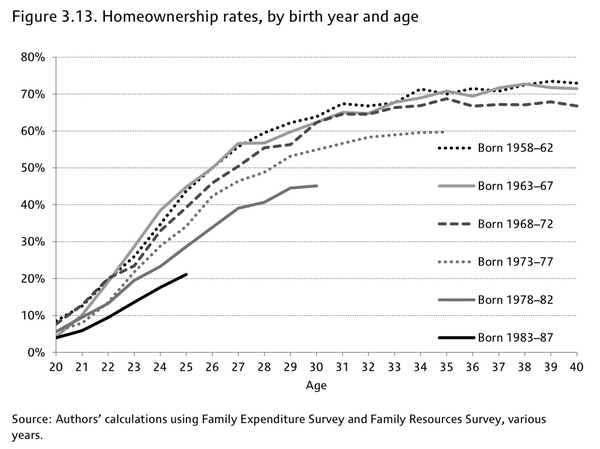

Only 21% of people born in the 1980s had bought their own house by the age of 25, compared with 34% of those born in the 70s and 45% of those born in the 60s.

That's a great stat which blows apart the old 'it was tough in my day too' canard.

Given bank of mum and dad lending of deposits has increased too the 'natural' rate is probably even lower.0 -

I really can't understand why the young seem to be against cuts (UK Uncut etc), they are the ones that will have to pay for all the extra debt.0

-

I really can't understand why the young seem to be against cuts (UK Uncut etc), they are the ones that will have to pay for all the extra debt.

I'm not sure they are against cuts per se.

But it does seem madness to me for example to be cutting job centres, citizens advice etc etc while continuing to provide money for bus passes, winter fuel payments to all and so on.I don't really understand the free school meal thing either when cutting much needed services elsewhere. Cuts to housing benefits have specifically targetted the young while older couples rattling around in 3 bed homes are offered the change to buy it for a discount.

Younger familes have been targetted when looking at re-housing, yet anyone over 60 was removed from this scheme and left well alone.

The whole pension thing was a bit strange too, this annuity thing. None of the young will be able to access it, but they will be paying for it both in terms of finances (accoring to independent experts this will cost the taxpayer more due to the age of the likely applicants) and also have to work longer for their own pensions.

Seems to me the cuts seem stacked towards the young, but also, the more vulnerable. Maybe there are just more services for thise people to be cut in the first place, I don't know. But some of the things the council are cutting seem to be directly hurting the young and younger families with younger children and in some cases, such as housing, anyone over 60 is ring fenced.0 -

Maybe that's because people were well placed to use Right to Buy in the mid-80s.

Also, young people are going to Uni that would have left school at 16 or perhaps 18 in the 1980s. If you leave school at 16 for a trade that means that you reach peak earning potential pretty early on in your career you can reasonably expect to buy early. If you go to Uni until you're 22 and then have a gap year you're not likely to be in a position to buy a house! I don't really see this as a huge problem: people are living and working longer so it makes sense for me to drag these things out a bit.

The people I worry for are all these poor suckers born in the 1960s that actually think that working for 30 years and paying little or nothing in to a pension is going to provide for a rich, well paid retirement for a further 30+ years. Generation X already outnumbers the Boomers. Once Generation Y start voting in serious numbers, the Boomers are likely to find the plug pulled on all their unlikely perks.0 -

Maybe that's because people were well placed to use Right to Buy in the mid-80s.

Also, young people are going to Uni that would have left school at 16 or perhaps 18 in the 1980s. If you leave school at 16 for a trade that means that you reach peak earning potential pretty early on in your career you can reasonably expect to buy early. If you go to Uni until you're 22 and then have a gap year you're not likely to be in a position to buy a house! I don't really see this as a huge problem: people are living and working longer so it makes sense for me to drag these things out a bit.

...

i should think that both of those two explanations are somewhat good at explaining the difference [45% ownership at aged 25 vs 34% at the same age] between the 60s-born cohort & the 70s-born cohort, but much less the slightly bigger difference [34% vs 21%] between the 70s & 80s cohort. and even if this explanation was key it wouldn't detract from the basic idea that it was harder for the 80s cohort to buy for reasons that had nothing to do with its choices and that didn't go hand hand with compensatory benefits [e.g. the choice to go to uni or whatever].

Higher education participation had pretty much reached its current very high level by time people born in the mid 70s got to apply, similarly RTB was not a huge deal for the 70s cohort in the same way as for earlier ones.

i struggle with the idea that noughties HPI & BTL/debt boom played anything other than a huge role in explaining the 70s vs 80s difference.FACT.0 -

iphones and coffee0

-

-

FACT.0

FACT.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards