We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Official: BASEL 3 liquidity rules eased

Comments

-

What are the yields? At 65% LTV (which makes it 'safe RMBS) I can borrow at 2.79% for 5 years. Given the originating bank wants to make a profit it can package this up and sell it on at what - 2% or less - is this really a lot better than 5 year gilts but at higher risk?HAMISH_MCTAVISH wrote: »The reality is that UK RMBS are a relatively safe asset class with healthy yields. All RMBS currently suffer a bit of a PR problem after being tarred with the same brush as the American sub prime ones, but that wont last much longer.I think....0

-

What are the yields? At 65% LTV (which makes it 'safe RMBS) I can borrow at 2.79% for 5 years. Given the originating bank wants to make a profit it can package this up and sell it on at what - 2% or less - is this really a lot better than 5 year gilts but at higher risk?

Why 65%?

Any borrower currently getting a mortgage from a mainstream bank in the UK is a prime borrower.

I'd go so far as to say super-prime in fact, as banks have ramped up credit scoring to shrink the pool of otherwise perfectly creditworthy applicants, as they must ration limited funding.

All UK lending today, at any LTV, is beyond what would traditionally have been considered prime and safe.

So net yields on safe RMBS would be more like 3% on average, (50% higher than gilts) and thats after the bank has taken its cut.“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0 -

What are the yields? At 65% LTV (which makes it 'safe RMBS) I can borrow at 2.79% for 5 years. Given the originating bank wants to make a profit it can package this up and sell it on at what - 2% or less - is this really a lot better than 5 year gilts but at higher risk?

5 year Gilts are yielding about 1% so you are borrowing at almost 3x the risk free rate and you are highlighting the very best deal on the market. There presumably aren't unlimited funds available at that rate. A quick squizz seems to suggest that a decent (but not market best) 5 year fixed rate is well north of 3% and most are substantially above 3.75%. That is a lot more than 1%.HAMISH_MCTAVISH wrote: »So net yields on safe RMBS would be more like 3% on average, (50% higher than gilts) and thats after the bank has taken its cut.

Currently UK variable rate RMBS sell at something less than 150bps (1.5%) over LIBOR. Co-op sold £650,000,000 of variable rate RMBS at 135bps over LIBOR 6 months ago. 1 month LIBOR is under 0.25% and 3 month is about 0.3% at the moment so the current rate on that RMBS is 1.6-1.65% (I CBA to look up the term sheet to see which LIBOR they use but it's most likely one of those two).

This, of course, is part of the point of QE/financial repression. The BoE is trying to force people to hold riskier assets and chase yield.0 -

HAMISH_MCTAVISH wrote: »... a tsunami of global liquidity will come crashing down on these shores...

:T.

super stuff. i can't wait.FACT.0 -

Just noticed Ben B will be gone within 12 months. Thats a real potential cliff, put in Lacker

http://www.telegraph.co.uk/finance/comment/jeremy-warner/9791795/Central-banks-must-switch-off-the-printing-presses-before-its-too-late.html0 -

Hamish, when will you understand the next time the BOE suspect there is to be a housing boom, they are going to slap mortgage controls and maximum lending limits on the banks. HPI as a result of over exuberant lending is dead.HAMISH_MCTAVISH wrote: »http://www.bbc.co.uk/news/business-20928354

A number of posters claimed that complying with the new rules would effectively prevent lending from growing for the foreseeable future.

That no longer appears to be the case.

(And congrats to Generali for predicting this some time ago.)

More interestingly, Residential Mortgage Backed Securities have returned to the list of acceptable assets to hold as part of the liquidity buffer.

And that will likely be something of a game changer.;)0 -

“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0 -

HAMISH_MCTAVISH wrote: »Thats not why we had HPI.

we've been through this, oh, a gazillion times are so, but both credit [price, supply] and population/building are important, as you well know.

looking at Halifax & ONS data for the last 10 years:

mid 2002 to mid 2007: pop growth +3.9%, HPI 78%.

mid 2007 to mid 2012: pop growth +4.1%, HPI -19%.

says it all really. whilst no-one would ever seriously argue that population/building don't matter, whatever absurd point it is that you're trying to make about credit [i.e. that it doesn't matter either] is very, very, very [etc] wrong. with tight lending i should think that we could sustain a huge population increase with very slow HPI. similarly with very loose lending, double digit annual inflation is easily possible.FACT.0 -

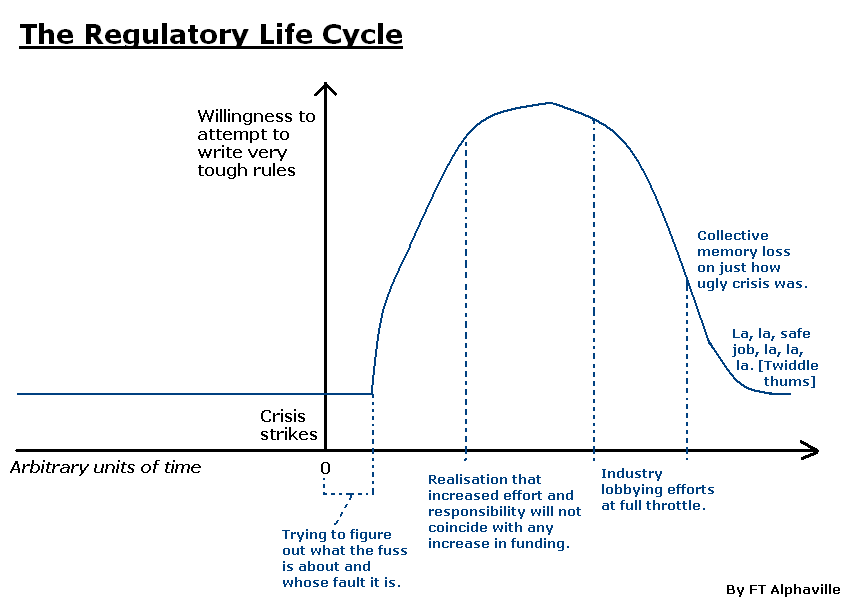

From FT Alphaville:

0

0 -

the_flying_pig wrote: »whilst no-one would ever seriously argue that population/building don't matter, .

Oh good.

As you well know, 70% of lending has been withdrawn from the market, yet prices remain just 10% below peak.

And that 10% price fall has only been created by preventing a million or more people from buying houses, thanks to mortgage rationing.

So yes, of course, credit does matter, and when you remove 70% of mortgage funding from any market, prices will fall.

But excessively loose credit was not the primary cause of UK HPI.“The great enemy of the truth is very often not the lie – deliberate, contrived, and dishonest – but the myth, persistent, persuasive, and unrealistic.

Belief in myths allows the comfort of opinion without the discomfort of thought.”

-- President John F. Kennedy”0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards