We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Is there a 6 month limit to getting the Financial Ombudsman involved?

Comments

-

Dunstonh, i see what you mean and i have only posted what has been relayed to me. The letters have said that they buy the units anyway, the phone conversations said that does not happen.

Jamesd, thank you so very very much. It's advice like that which makes laypeople such as me so grateful for forums such as this and helpful people such as you!!

Thanks to you i now have a plan of action, which i will complete.

I did email the FOS earlier in the week to inform them that the email was notification of my complaint and that i would fill out the complaint details form this weekend. Hopefully that email will act as the official start of my complaint.

I will send the SAR off this weekend with the ammendments.

Please can i ask do i send the £10 cheque as i have with the banks?

And isn't it 40 days to respond, as is with the banks?Not yet a total moneysaving expert...but im trying!!0 -

Please can i ask do i send the £10 cheque as i have with the banks?

And isn't it 40 days to respond, as is with the banks?Not yet a total moneysaving expert...but im trying!!0 -

It's 40 days and I've corrected my post. If you don't send a fee and one is required they get more time to ask you to send payment. Easier to send a cheque and let them return it to you if no fee is required.

Do note that unlike dunstonh I'm also a lay person. I've just been around and learning for a while.0 -

Ok, i'm just about to send the complaint form off the FOS. In the meantime, i have written to SW asking why, on my friend's annual statement it shows three months of contributions missing if they 'buy the units regardless of whether' my employer makes the contributions on time. Surely if that were the case then the contributions would be showing on the annual statement??

So, am i right in saying that not only could/would the unit price have changed from, say, June 2011 (supposed to have been bought) and September 2011 (when they were actually bought)?

And surely an investment bought in, say, June 2011 could have grown more than one bought in September 2011? If so, then my friend is losing twice over?Not yet a total moneysaving expert...but im trying!!0 -

Yes.So, am i right in saying that not only could/would the unit price have changed from, say, June 2011 (supposed to have been bought) and September 2011 (when they were actually bought)?

Could have is correct. Did is not so likely.And surely an investment bought in, say, June 2011 could have grown more than one bought in September 2011? If so, then my friend is losing twice over?

Depends on the investment. If it was say a FTSE All Share Index tracker fund there was a drop in the markets of about 12% in early August. That meant that buying that investment in September would have bought the units significantly more cheaply. The price has largely recovered since then back to the original level, leaving him with a potential profit of perhaps 10-15% depending on exact timing. Solely due to the delay, which will have worked to his benefit in this case.

See the chart and change the period from yearly to monthly and set to 12 months and you can see what happened.0 -

Thank you so much. Unfortunately im not on a computer so cant check the chart but i certainly will later.

The months i gave were an example only, i will check the relevant dates.

However, this may be a bit tricky as the annual statement from SW only showed which months weren't on there and when i questioned them as to WHEN these actual months were finally bought/paid they come back with the line 'All contributions are up to date. Units are bought regardless of when contributions are received so therefore there is no loss to yourself', which is contrary to what the annual statements show AND what the customer services people have been telling me. In fact one of them told me the dates that were missing and the dates my employer made the 'lump sum' catch-up payments.Not yet a total moneysaving expert...but im trying!!0 -

Thank you so much. Unfortunately im not on a computer so cant check the chart but i certainly will later.

The months i gave were an example only, i will check the relevant dates.

However, this may be a bit tricky as the annual statement from SW only showed which months weren't on there and when i questioned them as to WHEN these actual months were finally bought/paid they come back with the line 'All contributions are up to date. Units are bought regardless of when contributions are received so therefore there is no loss to yourself', which is contrary to what the annual statements show AND what the customer services people have been telling me. In fact one of them told me the dates that were missing and the dates my employer made the 'lump sum' catch-up payments.Not yet a total moneysaving expert...but im trying!!0 -

-

Apolgies, Jamesd,

I was paraphrasing, here is how SW phrased it:

'Your policy is classed as a 'due date' policy, irrespective of when we receive payments from your employer the premiums are applied to your policy using the unit price applicable on the 28th of each month'

and

'However, in this case, we have an agreement with your employer to use a set date. We purchase the units and they pay us for them at a later date. As everything gets backdated to when it should be, there really is no concern for you. In other words, i think you can rest easy as i believe this is a secure and robust methodolgy they are employing. To be clear; it makes no difference when they actually send us the funds.This helps you keep track of what is going on and also reassures you, in the case they are late.'Not yet a total moneysaving expert...but im trying!!0 -

Ok, i hope this is ok but i really would like your opinions on these statements, Jamesd and Dunstonh (or anybody, for that matter):

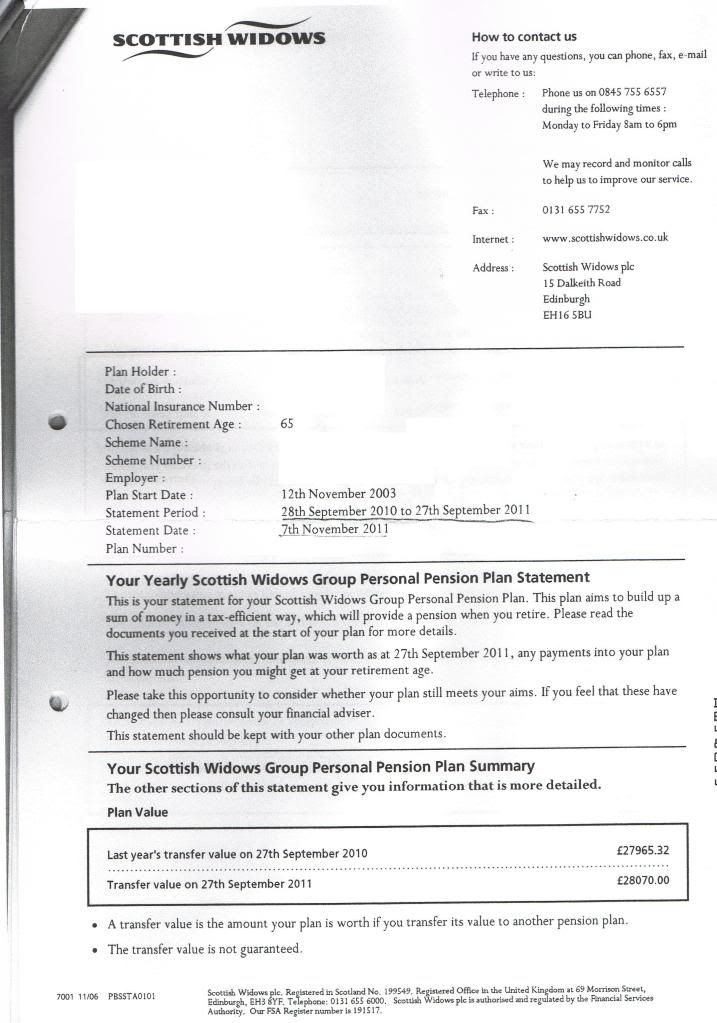

Here is my friend's annual statement that he received in September 2011 showing a statement of September 2010 to September 2011, showing a transfer value of £27858.56:

http://i199.photobucket.com/albums/aa214/craigten/1sept.jpg

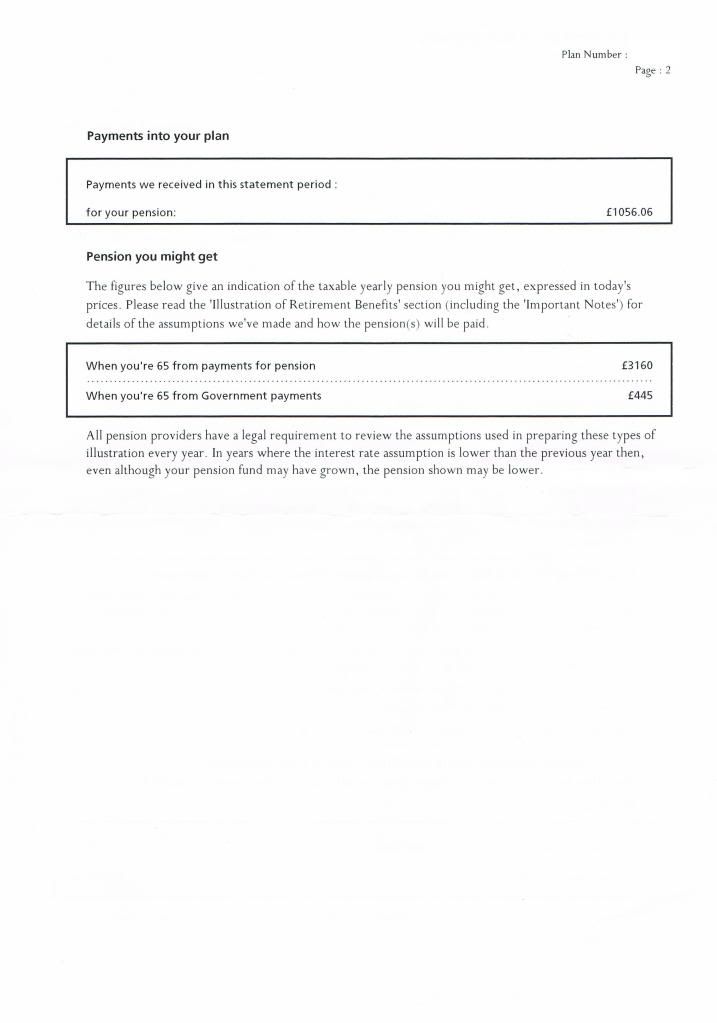

Here is the second page of that statement showing the total payments they received for the 12 month period was £1056.06:

http://i199.photobucket.com/albums/aa214/craigten/1asept.jpg

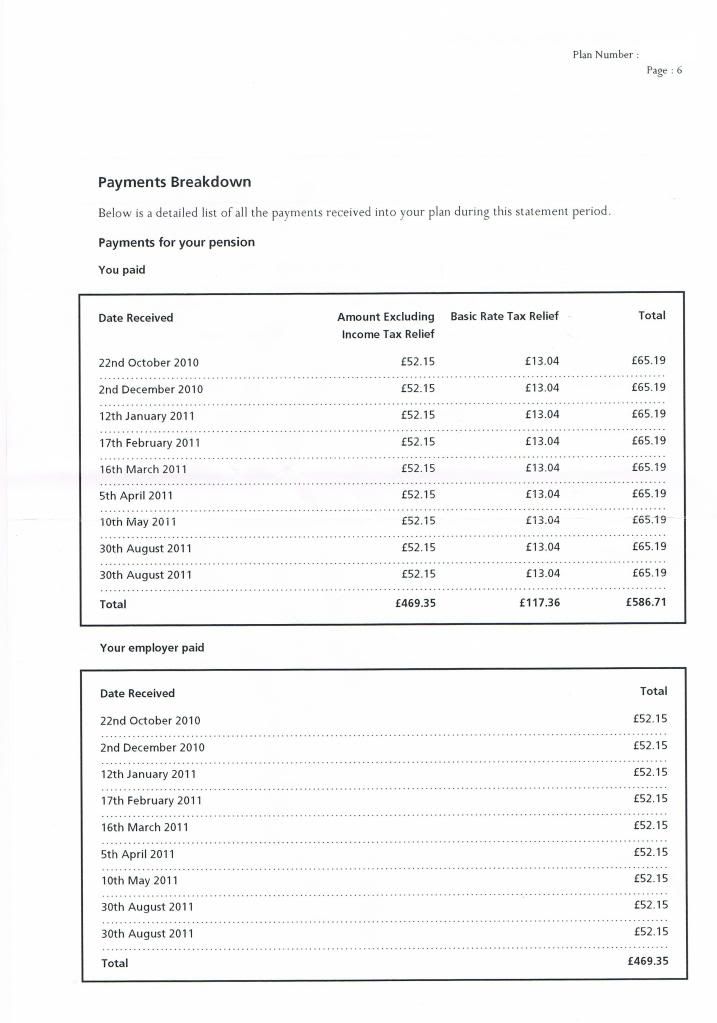

Here is the third page of the statement showing missing payments of September 2010, June 2011 and July 2011:

http://i199.photobucket.com/albums/aa214/craigten/2sept.jpg

Here is the fourth page showing the monthly contribution amount:

http://i199.photobucket.com/albums/aa214/craigten/2asept.jpg

Here is the fifth page that is called a History of payments' that shows that all contributions were paid (SW wont explain to me the contradiction between this and the annual statement):

http://i199.photobucket.com/albums/aa214/craigten/4sept.jpg

Now, here is my friend's annual statement that he received in November 2011 showing the same statement period of September 2010 to September 2011, but this time showing a transfer value of £28070.00:

http://i199.photobucket.com/albums/aa214/craigten/1.jpg

Here is the second page of this statement showing the same months of September 2010, June 2011 and July 2011 still missing:

http://i199.photobucket.com/albums/aa214/craigten/2.jpg

So you can now see why my friend (and I) are so frustrated at SW stating that 'all payments are up to date' when they might very well be up to date but they were not made on the dates that they were supposed to have been made, thus potentially causing my friend to lose out financially?Not yet a total moneysaving expert...but im trying!!0

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards