We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early-retirement wannabe

Comments

-

Returning to real life has been fine. For me it was the third time returning to work after a year or so away travelling, but it was the first time for my wife. It was all very easy to slot back into the old routines, especially for me as I returned to the same sort of things I was doing before leaving whereas my wife took a new role.How has returning to 'real life' after travelling worked? Seems you are very adaptable as I suspect many would struggle to return to the norm after such an amazing trip.

The hardest thing was probably returning to our house, which we had lived in for 12 years before travelling. After 18 months rented out, it took a while before it felt like our house again and that was a bit disconcerting.

I think it definitely helps that we were only ever coming back for a short period or 1-2 years. If I was back and looking at another 10 years then I would want to be doing something different.

I do have family there, and it the region I grew up in, but that is a very minor consideration.Any reason for the NW England location choice, are there family commitments as otherwise you could probably chose somewhere with better weather!

I don't want to be anywhere in the south of England, partly due to the volume of people and traffic, and partly because of house prices - we can get what we want anywhere in the country, so happy to go to areas with fewer people and cheaper house prices and lower cost of living in general. Despite being able to afford it, I have an intense dislike of spending insane amounts on a meal out. I think this is in part due to travel - I've eaten out at great places in countries such as Argentina for under £10 per person, so just don't see the value in spending £50+ on a meal that isn't as good in the UK. Lower cost of living helps with that resentment!

There is also proximity to a big city. I certainly don't want that to be London, so the obvious choices after that are Birmingham and Manchester. The northwest is convenient for both of those, as well as great transport connections whether that is road or rail, or even air from Manchester (airports were a bit of a consideration when we were thinking about living deeper into north Wales).

We also plan to have two snow dogs, probably an Alaskan Malamute and a husky. For those animals, the colder and more miserable the weather, the better! I find the summers in London a little too warm for my liking, so happy with north-west weather.

Not really.Do you have any fears regarding potential government curve balls for example on access to pension dates or even the TFLS?

Almost all of our pensions have protected minimum pension age, and there is next to no chance of those being retrospectively removed. Our DC pension is £283K in total, of which £232K is mine, so even a lower cap on TFLS is unlikely to hurt unless it is slashed from £268,275 to under about £75,000 which seems unlikely in the next 9 years.

The biggest risk would probably be around State Pension, mainly as that is over 20 years away for us, so plenty of scope for tinkering with a long lead in time. But there are no signs of that under the current Govt. yet, so that should fall to 15 years under the next administration - still a bit too long to be comfortable, but feels a little safer.Is there nothing you can do to better balance your pension provision between the pre and post DB dates as at the moment if you go large on the house you are looking at quite a big jump in income at 55?

It should mostly look after itself. The figures increase very rapidly, as we spend less than than even the c£45K we would have if we were to buy a house and quit work today. So we are 'saving' some of that available income, plus all of our earnings, and every day the 8 year period the funds have to cover is decreasing. Add in returns from investments, and the figures increase rapidly.

Also, I am conservative in estimates about things like what I will sell our current house for. So as the process proceeds, additional funds should be realised as actual figures are better than the estimates.

Nonetheless, I still plan to get an offset mortgage, so that if we were to want to spend more pre-55 we could do so. In practice, that would be just before age 55 as other funds ran out, and even borrowing at, say, 6% p/a, would be an excellent deal to repay it from pension income which has benefited from a 42% increase when putting it into a pension (40% relief on way in, 15% tax on way out). So I plan for this year to put all my wife's higher rate income into a pension, and I will take a view late in the tax year on whether I do the same for me. The benefits are less clear cut for me, as I could struggle to extract all my DC pension without paying higher rate, and am more vulnerable to political change. However, if come March 2025 we are buying or have bought a house with an offset mortgage, then I would dump all my higher rate income into a pension anyhow, as the return is too great to ignore. That means having a lower pre-55 income on paper is actually beneficial, as long as I have the option to borrow and repay from pension income.

I am told the NW is becoming the area of choice for younger retirees, replacing coastal towns which are now regarded as being heavily populated by what have now become very old pensioners after years of being a popular retirement place.george_jetson said:I have always thought NW England would be an ideal region to retire - easy access to major cities and countryside, and Merseyrail meaning you needn’t be reliant on a car. Somewhere on the Wirral near a railway station and a beach would be perfect I think.

I haven't entirely discounted the Wirral peninsula, perhaps just to the east of Bromborough near a country park. But to date I haven't seen a property I particularly like and my target areas are quite limited so I don't expect to end up there. The area is blighted by Birkenhead at the north-end of the peninsula which is a place to avoid, but the areas on the west of the peninsula are very nice too.

2 -

Perhaps rent initially, if moving to a new area?hugheskevi said:

I am told the NW is becoming the area of choice for younger retirees, replacing coastal towns which are now regarded as being heavily populated by what have now become very old pensioners after years of being a popular retirement place.

I haven't entirely discounted the Wirral peninsula, perhaps just to the east of Bromborough near a country park. But to date I haven't seen a property I particularly like and my target areas are quite limited so I don't expect to end up there. The area is blighted by Birkenhead at the north-end of the peninsula which is a place to avoid, but the areas on the west of the peninsula are very nice too.

It's quite a different prospect to live in a new place, and I've found that renting allowed us to refine our location once we'd found our feet.

Wirral is OK. There are some nice parts of Birkenhead, but I'd avoid.

My family are around Bromborough, so I know the area quite well.

I'd be looking perhaps at somewhere towards Neston / Parkgate ideally, or just the other side of Chester.

You are very close to Wales / Wrexham / Buckley.

One thing on the property prices - I'd guess that the stamp duty differential has become / will become baked into the relative property prices along the border - ie an equivalent house just inside Wales will be c£15,000 cheaper than that on the England side.

For me, the ideal would be something perhaps a little closer to Mold / the Berwyns. Not far from civilisation, with lovely views, walks and hamlets.1 -

One small point - although the stamp duty is higher in Wales, the cost of the houses is lower. We were recently looking at houses around the Wrexham area on both sides of the border - it seemed to me that the additional stamp duty was offset by the lower house price - it was noticeable for example that in Farndon / Holt, just crossing the bridge made a significant difference to house prices.hugheskevi said:It finally feels like we've started the beginning of the end on the route to conventional early retirement, albeit early retirement at what will be a relatively young age of 47.

Everything in our lives will change, as we relocate to a new area, get a new car, dispose of most of our things, purchase new stuff, and finally quit work. We will get two rescue dogs and set up a whole new life in a new area as we move away from London.

Since April I have been researching where we will move to within north-east Wales and north-west England. The best places for us tend to be the outskirts of a town, where we have immediate access to a large green space for dogs and running, but where there will also be a leisure centre for gym, classes, and swimming, and also a running club. Proximity (about 1-hour drive) to a major city is also desirable. The places we are most likely to move, with links to the property I like the most in each area, are Congleton, Whitchurch, Wrexham, or Buckley.

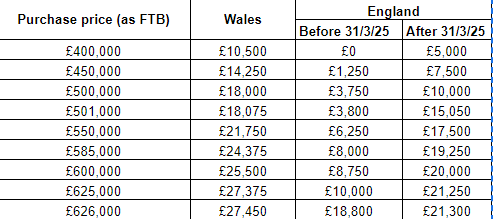

I suspect however that we won't move to Wales. A key reason for this is the Welsh government. We would have to pay a large premium in Stamp Duty (Land Transaction Tax in Wales), which is very hard to justify. There is also the way Welsh govt. handled COVID, the 20mph debacle, and the First Minister mess which makes it less attractive, especially as the direction any future variation to things like income tax rates would go seems clear. We would have to pay an additional £16,375 of Stamp Duty to live in Wales, compared to an equally priced house in England, which is less than 5 miles away from both Buckley and Wrexham. I struggle to justify that.

Sadly my hopes to extract my DC pension tax-free via a future transfer to the LGPS won't work. But on the positive side, we may well be able to take advantage of my wife being a first-time buyer to get a Stamp Duty discount in England. To do that, we would need to sell our current house (which is solely in my name) before we could buy somewhere as otherwise she would be ineligible due to having an interest in a property, then my wife could buy our next property solely in her name as a first time buyer. That would all need to be done by 31st March 2025. The difference in Stamp Duty is considerable, saving around £12,000.

The table below shows the Stamp Duty (Land Transaction Tax in Wales) due on properties in the range we expect to spend, based on being a First Time Buyer. There are an alarming amount of cliff-edges to avoid falling foul of, more well-designed fiscal policies!

We plan to wait until the Budget at the end of October and then immediately view properties, so the financial landscape should be clear when we view and consider making offers. I have almost finished moving all our cash ISAs to flexible ISAs, and could raise about £200,000 in cash almost immediately, or a bit over £500,000 if I also included stocks and shares ISAs (transferred to flexible cash ISA before withdrawing as our current SSISA is not flexible). That would enable my wife to buy somewhere, probably with a modest offset-mortgage separate to selling our house - although I would have to sell our house before buying somewhere for her to be a first time buyer.

Taking into account selling the current house, paying off all debt, buying a car costing £20,000 (probably a newish MG5), spending £20,000 on new furnishings, and all costs of moving (incl. Stamp Duty), the position based on immediately retiring and buying a new property today would be: (based on moving to Wales, as that is the worst-case scenario from a financial perspective)

I plan to market our property on Boxing Day, subject to any Budget changes. That is a bit earlier than I had planned, but with all the Stamp Duty cliff edges I expect that if there are no changes at Budget there will be huge property market activity to get sales through for changes due for implementation on 31st March 2025. If it doesn't all come together in time, it just means a bit of extra tax, which isn't much in the great scheme of things.

We intend to keep working until after we have moved into our new house, and give notice at that point (3 months). That will derisk everything, as we can carry on working if we wish (eg if costs are higher than expected). It is more about keeping all options open rather than managing risk though, as everything looks very comfortable. Therefore I expect to leave work sometime between June and December 2025, as working Jan-Mar 2026 would have nil Bank Holidays and all be taxed at higher rate, so I can't see myself wanting to work beyond Christmas at the latest just to have to pay a lot of salary in tax.

At age 55 our pensions will give us an annual net income of just over £70,000 p/a for the rest of our lives, initially from DB and DC pensions. From State Pension age, our State Pension and Defined Benefit pensions will provide a minimum of (in today's price terms):

For now, life is rather mundane, as I work my way through a list of things to do in my existing house to get the exterior and interior into shape - nothing very much, just minor DIY work over the next couple of months to be ready for whatever comes out of Budget. Then everything should get a lot more interesting and start moving fast.2 -

Thanks, that is useful to know, and is consistent with what I have seen as well. Either houses in Wales seem to be sold for a cheaper price, or they are marketed at a similar price to what I would expect to see in England but don't get sold.Pat38493 said:

One small point - although the stamp duty is higher in Wales, the cost of the houses is lower. We were recently looking at houses around the Wrexham area on both sides of the border - it seemed to me that the additional stamp duty was offset by the lower house price - it was noticeable for example that in Farndon / Holt, just crossing the bridge made a significant difference to house prices.hugheskevi said:It finally feels like we've started the beginning of the end on the route to conventional early retirement, albeit early retirement at what will be a relatively young age of 47.

Everything in our lives will change, as we relocate to a new area, get a new car, dispose of most of our things, purchase new stuff, and finally quit work. We will get two rescue dogs and set up a whole new life in a new area as we move away from London.

Since April I have been researching where we will move to within north-east Wales and north-west England. The best places for us tend to be the outskirts of a town, where we have immediate access to a large green space for dogs and running, but where there will also be a leisure centre for gym, classes, and swimming, and also a running club. Proximity (about 1-hour drive) to a major city is also desirable. The places we are most likely to move, with links to the property I like the most in each area, are Congleton, Whitchurch, Wrexham, or Buckley.

I suspect however that we won't move to Wales. A key reason for this is the Welsh government. We would have to pay a large premium in Stamp Duty (Land Transaction Tax in Wales), which is very hard to justify. There is also the way Welsh govt. handled COVID, the 20mph debacle, and the First Minister mess which makes it less attractive, especially as the direction any future variation to things like income tax rates would go seems clear. We would have to pay an additional £16,375 of Stamp Duty to live in Wales, compared to an equally priced house in England, which is less than 5 miles away from both Buckley and Wrexham. I struggle to justify that.

Sadly my hopes to extract my DC pension tax-free via a future transfer to the LGPS won't work. But on the positive side, we may well be able to take advantage of my wife being a first-time buyer to get a Stamp Duty discount in England. To do that, we would need to sell our current house (which is solely in my name) before we could buy somewhere as otherwise she would be ineligible due to having an interest in a property, then my wife could buy our next property solely in her name as a first time buyer. That would all need to be done by 31st March 2025. The difference in Stamp Duty is considerable, saving around £12,000.

The table below shows the Stamp Duty (Land Transaction Tax in Wales) due on properties in the range we expect to spend, based on being a First Time Buyer. There are an alarming amount of cliff-edges to avoid falling foul of, more well-designed fiscal policies!

We plan to wait until the Budget at the end of October and then immediately view properties, so the financial landscape should be clear when we view and consider making offers. I have almost finished moving all our cash ISAs to flexible ISAs, and could raise about £200,000 in cash almost immediately, or a bit over £500,000 if I also included stocks and shares ISAs (transferred to flexible cash ISA before withdrawing as our current SSISA is not flexible). That would enable my wife to buy somewhere, probably with a modest offset-mortgage separate to selling our house - although I would have to sell our house before buying somewhere for her to be a first time buyer.

Taking into account selling the current house, paying off all debt, buying a car costing £20,000 (probably a newish MG5), spending £20,000 on new furnishings, and all costs of moving (incl. Stamp Duty), the position based on immediately retiring and buying a new property today would be: (based on moving to Wales, as that is the worst-case scenario from a financial perspective)

I plan to market our property on Boxing Day, subject to any Budget changes. That is a bit earlier than I had planned, but with all the Stamp Duty cliff edges I expect that if there are no changes at Budget there will be huge property market activity to get sales through for changes due for implementation on 31st March 2025. If it doesn't all come together in time, it just means a bit of extra tax, which isn't much in the great scheme of things.

We intend to keep working until after we have moved into our new house, and give notice at that point (3 months). That will derisk everything, as we can carry on working if we wish (eg if costs are higher than expected). It is more about keeping all options open rather than managing risk though, as everything looks very comfortable. Therefore I expect to leave work sometime between June and December 2025, as working Jan-Mar 2026 would have nil Bank Holidays and all be taxed at higher rate, so I can't see myself wanting to work beyond Christmas at the latest just to have to pay a lot of salary in tax.

At age 55 our pensions will give us an annual net income of just over £70,000 p/a for the rest of our lives, initially from DB and DC pensions. From State Pension age, our State Pension and Defined Benefit pensions will provide a minimum of (in today's price terms):

For now, life is rather mundane, as I work my way through a list of things to do in my existing house to get the exterior and interior into shape - nothing very much, just minor DIY work over the next couple of months to be ready for whatever comes out of Budget. Then everything should get a lot more interesting and start moving fast.

Buying in Wales would also remove the incentive/pressure to complete before 31 March 2025 (which even if I didn't care about too much, it is likely whomever purchases my house in London might well care about given the reduction in price thresholds from £625K to £500K).

I thought about renting, but really don't want the extended period of upheaval. I've put a lot of effort into researching our preferred areas and houses, and we went out to visit several back in February of this year. We will go and visit the areas again in October, and I'm confident that we have a very clear idea of what we want.ex-pat_scot said:

Perhaps rent initially, if moving to a new area?hugheskevi said:

I am told the NW is becoming the area of choice for younger retirees, replacing coastal towns which are now regarded as being heavily populated by what have now become very old pensioners after years of being a popular retirement place.

I haven't entirely discounted the Wirral peninsula, perhaps just to the east of Bromborough near a country park. But to date I haven't seen a property I particularly like and my target areas are quite limited so I don't expect to end up there. The area is blighted by Birkenhead at the north-end of the peninsula which is a place to avoid, but the areas on the west of the peninsula are very nice too.

It's quite a different prospect to live in a new place, and I've found that renting allowed us to refine our location once we'd found our feet.

Particularly after spending 18 months away travelling recently, I really wouldn't like 2025 to involve a couple of moves. In other circumstances renting initially would be attractive though.2 -

Great update @hugheskevi - what I love most is your approach to researching and making decisions, very little pontificating, and not being swayed in your resolve. I think it’s absolutely how you have to be , to both have the adventures you have enjoyed, and implement the life changes you are determined to make - chapeau to you and the family for the sheer boldness involved!2

-

As if by magic, an MG5 for under 20k brand newhugheskevi said:It finally feels like we've started the beginning of the end on the route to conventional early retirement, albeit early retirement at what will be a relatively young age of 47.

Everything in our lives will change, as we relocate to a new area, get a new car, dispose of most of our things, purchase new stuff, and finally quit work. We will get two rescue dogs and set up a whole new life in a new area as we move away from London.

Since April I have been researching where we will move to within north-east Wales and north-west England. The best places for us tend to be the outskirts of a town, where we have immediate access to a large green space for dogs and running, but where there will also be a leisure centre for gym, classes, and swimming, and also a running club. Proximity (about 1-hour drive) to a major city is also desirable. The places we are most likely to move, with links to the property I like the most in each area, are Congleton, Whitchurch, Wrexham, or Buckley.

I suspect however that we won't move to Wales. A key reason for this is the Welsh government. We would have to pay a large premium in Stamp Duty (Land Transaction Tax in Wales), which is very hard to justify. There is also the way Welsh govt. handled COVID, the 20mph debacle, and the First Minister mess which makes it less attractive, especially as the direction any future variation to things like income tax rates would go seems clear. We would have to pay an additional £16,375 of Stamp Duty to live in Wales, compared to an equally priced house in England, which is less than 5 miles away from both Buckley and Wrexham. I struggle to justify that.

Sadly my hopes to extract my DC pension tax-free via a future transfer to the LGPS won't work. But on the positive side, we may well be able to take advantage of my wife being a first-time buyer to get a Stamp Duty discount in England. To do that, we would need to sell our current house (which is solely in my name) before we could buy somewhere as otherwise she would be ineligible due to having an interest in a property, then my wife could buy our next property solely in her name as a first time buyer. That would all need to be done by 31st March 2025. The difference in Stamp Duty is considerable, saving around £12,000.

The table below shows the Stamp Duty (Land Transaction Tax in Wales) due on properties in the range we expect to spend, based on being a First Time Buyer. There are an alarming amount of cliff-edges to avoid falling foul of, more well-designed fiscal policies!

We plan to wait until the Budget at the end of October and then immediately view properties, so the financial landscape should be clear when we view and consider making offers. I have almost finished moving all our cash ISAs to flexible ISAs, and could raise about £200,000 in cash almost immediately, or a bit over £500,000 if I also included stocks and shares ISAs (transferred to flexible cash ISA before withdrawing as our current SSISA is not flexible). That would enable my wife to buy somewhere, probably with a modest offset-mortgage separate to selling our house - although I would have to sell our house before buying somewhere for her to be a first time buyer.

Taking into account selling the current house, paying off all debt, buying a car costing £20,000 (probably a newish MG5), spending £20,000 on new furnishings, and all costs of moving (incl. Stamp Duty), the position based on immediately retiring and buying a new property today would be: (based on moving to Wales, as that is the worst-case scenario from a financial perspective)

I plan to market our property on Boxing Day, subject to any Budget changes. That is a bit earlier than I had planned, but with all the Stamp Duty cliff edges I expect that if there are no changes at Budget there will be huge property market activity to get sales through for changes due for implementation on 31st March 2025. If it doesn't all come together in time, it just means a bit of extra tax, which isn't much in the great scheme of things.

We intend to keep working until after we have moved into our new house, and give notice at that point (3 months). That will derisk everything, as we can carry on working if we wish (eg if costs are higher than expected). It is more about keeping all options open rather than managing risk though, as everything looks very comfortable. Therefore I expect to leave work sometime between June and December 2025, as working Jan-Mar 2026 would have nil Bank Holidays and all be taxed at higher rate, so I can't see myself wanting to work beyond Christmas at the latest just to have to pay a lot of salary in tax.

At age 55 our pensions will give us an annual net income of just over £70,000 p/a for the rest of our lives, initially from DB and DC pensions. From State Pension age, our State Pension and Defined Benefit pensions will provide a minimum of (in today's price terms):

For now, life is rather mundane, as I work my way through a list of things to do in my existing house to get the exterior and interior into shape - nothing very much, just minor DIY work over the next couple of months to be ready for whatever comes out of Budget. Then everything should get a lot more interesting and start moving fast.

Affordable MG MG5 EV 61kWh Long Range SE at Baylis MG, Colchester - £19995 | hotukdeals

I think....1 -

Hi all,

I'm really loving this thread, I feel less alone in my spreadsheet/countdown madness! Since discovering this MSE forum I have (as a single mother, small business owner, independent musician with no outside support)

1. Saved up a deposit for a small flat in a wonderful friendly part of London where I have a great community.

2. Paid cash for an extension, balcony build and complete remodel of flat.

3. 8 years ago took the plunge, found a 'wealth adviser' and started bunging all my 40per cent tax bracket in high risk equities.

4. Lived strictly within the under £52k tax band even though I earn way more, to not let my lifestyle become too swanky. Packed lunches, cycle everywhere, etc etc BUT long haul travel and lots of music fun.

5. chucked £500 a month to overpay mortgage (which is big and terrifies me)

6. Really looked after my health and make sure I have a lot of fun with my son and friends/family.

I am planning to semi retire early 5 months before my 60th birthday, by keep overpaying mortgage, and using TFLS to pay off the remainder in 68 months. That'll be my mortgage paid off 8 years early.

Because I absolutely love my job, and only do 20 hours a week, I will keep going because I want to (but without the fear of being made homeless) and keep funding my SIPP. I will have an extra £30k a year that isn't being used for mortgage, mortgage overpayments and various self employed earnings insurance.

I plan to travel, gig, whatever.

Then part 2 comes when I'm 67 and could retire with about £20k coming in, or just the £10k state pension, and keep working....my options will be open.

Im also interested in buying something in the South of France perhaps one day. Lots of family there, Potential for letting out......

THANK YOU for helping me and inspiring me for the last 10 years to get my head out of the sand.

Edit... It is actually my 10 year anniversary here today! Just got the badge!

It's never too late! I started being financially smart/brave when I was 42, with property and 45 with my pension.

I was a late starter, music college at 24 as a mature student (had no qualifications), arrived in London penniless in 1999 and lived at the YMCA while studying a postgrad that I'd received a scholarship for. I've never stopped fighting for my freedom and autonomy while maintaining a good lifestyle. I constantly reassess what I value and what really gives me meaning. I've known poverty and homelessness as a child and never want to be vulnerable like that again.

I welcome your comments!

14 -

Sounds great, I’m so glad I really knuckled down and sorted my pension arrangements, I’ve got a DB one but really want to retire early so I’ve loaded up a SIPP.Springfield1970 said:Hi all,

I'm really loving this thread, I feel less alone in my spreadsheet/countdown madness! Since discovering this MSE forum I have (as a single mother, small business owner, independent musician with no outside support)

1. Saved up a deposit for a small flat in a wonderful friendly part of London where I have a great community.

2. Paid cash for an extension, balcony build and complete remodel of flat.

3. 8 years ago took the plunge, found a 'wealth adviser' and started bunging all my 40per cent tax bracket in high risk equities.

4. Lived strictly within the under £52k tax band even though I earn way more, to not let my lifestyle become too swanky. Packed lunches, cycle everywhere, etc etc BUT long haul travel and lots of music fun.

5. chucked £500 a month to overpay mortgage (which is big and terrifies me)

6. Really looked after my health and make sure I have a lot of fun with my son and friends/family.

I am planning to semi retire early 5 months before my 60th birthday, by keep overpaying mortgage, and using TFLS to pay off the remainder in 68 months. That'll be my mortgage paid off 8 years early.

Because I absolutely love my job, and only do 20 hours a week, I will keep going because I want to (but without the fear of being made homeless) and keep funding my SIPP. I will have an extra £30k a year that isn't being used for mortgage, mortgage overpayments and various self employed earnings insurance.

I plan to travel, gig, whatever.

Then part 2 comes when I'm 67 and could retire with about £20k coming in, or just the £10k state pension, and keep working....my options will be open.

Im also interested in buying something in the South of France perhaps one day. Lots of family there, Potential for letting out......

THANK YOU for helping me and inspiring me for the last 10 years to get my head out of the sand.

It's never too late! I started being financially smart/brave when I was 42, with property and 45 with my pension.

I was a late starter, music college at 24 as a mature student (had no qualifications), arrived in London penniless in 1999 and lived at the YMCA while studying a postgrad that I'd received a scholarship for. I've never stopped fighting for my freedom and autonomy while maintaining a good lifestyle. I constantly reassess what I value and what really gives me meaning. I've known poverty and homelessness as a child and never want to be vulnerable like that again.

I welcome your comments!

also, you love your job? That’s great, I wish I could say the same!1 -

Yes! Though it took me years to really make my mind up and go for it. And I spent decades living on the bread line. It's only the last 12-15 years that its paid off really. I really encourage young people nowadays to take their time to mess around, have fun, work, realise how hard 'working life' is and then follow their passion. And not take handouts!pterri said:

Sounds great, I’m so glad I really knuckled down and sorted my pension arrangements, I’ve got a DB one but really want to retire early so I’ve loaded up a SIPP.Springfield1970 said:Hi all,

I'm really loving this thread, I feel less alone in my spreadsheet/countdown madness! Since discovering this MSE forum I have (as a single mother, small business owner, independent musician with no outside support)

1. Saved up a deposit for a small flat in a wonderful friendly part of London where I have a great community.

2. Paid cash for an extension, balcony build and complete remodel of flat.

3. 8 years ago took the plunge, found a 'wealth adviser' and started bunging all my 40per cent tax bracket in high risk equities.

4. Lived strictly within the under £52k tax band even though I earn way more, to not let my lifestyle become too swanky. Packed lunches, cycle everywhere, etc etc BUT long haul travel and lots of music fun.

5. chucked £500 a month to overpay mortgage (which is big and terrifies me)

6. Really looked after my health and make sure I have a lot of fun with my son and friends/family.

I am planning to semi retire early 5 months before my 60th birthday, by keep overpaying mortgage, and using TFLS to pay off the remainder in 68 months. That'll be my mortgage paid off 8 years early.

Because I absolutely love my job, and only do 20 hours a week, I will keep going because I want to (but without the fear of being made homeless) and keep funding my SIPP. I will have an extra £30k a year that isn't being used for mortgage, mortgage overpayments and various self employed earnings insurance.

I plan to travel, gig, whatever.

Then part 2 comes when I'm 67 and could retire with about £20k coming in, or just the £10k state pension, and keep working....my options will be open.

Im also interested in buying something in the South of France perhaps one day. Lots of family there, Potential for letting out......

THANK YOU for helping me and inspiring me for the last 10 years to get my head out of the sand.

It's never too late! I started being financially smart/brave when I was 42, with property and 45 with my pension.

I was a late starter, music college at 24 as a mature student (had no qualifications), arrived in London penniless in 1999 and lived at the YMCA while studying a postgrad that I'd received a scholarship for. I've never stopped fighting for my freedom and autonomy while maintaining a good lifestyle. I constantly reassess what I value and what really gives me meaning. I've known poverty and homelessness as a child and never want to be vulnerable like that again.

I welcome your comments!

also, you love your job? That’s great, I wish I could say the same!

It's never too late to combine your passion with making money.

Good for you putting that money away. Its really putting 'freedom' and 'choice' and 'power' tokens away isn't it?2 -

hugheskevi said:

Returning to real life has been fine. For me it was the third time returning to work after a year or so away travelling, but it was the first time for my wife. It was all very easy to slot back into the old routines, especially for me as I returned to the same sort of things I was doing before leaving whereas my wife took a new role.How has returning to 'real life' after travelling worked? Seems you are very adaptable as I suspect many would struggle to return to the norm after such an amazing trip.

The hardest thing was probably returning to our house, which we had lived in for 12 years before travelling. After 18 months rented out, it took a while before it felt like our house again and that was a bit disconcerting.

I think it definitely helps that we were only ever coming back for a short period or 1-2 years. If I was back and looking at another 10 years then I would want to be doing something different.

I do have family there, and it the region I grew up in, but that is a very minor consideration.Any reason for the NW England location choice, are there family commitments as otherwise you could probably chose somewhere with better weather!

I don't want to be anywhere in the south of England, partly due to the volume of people and traffic, and partly because of house prices - we can get what we want anywhere in the country, so happy to go to areas with fewer people and cheaper house prices and lower cost of living in general. Despite being able to afford it, I have an intense dislike of spending insane amounts on a meal out. I think this is in part due to travel - I've eaten out at great places in countries such as Argentina for under £10 per person, so just don't see the value in spending £50+ on a meal that isn't as good in the UK. Lower cost of living helps with that resentment!

There is also proximity to a big city. I certainly don't want that to be London, so the obvious choices after that are Birmingham and Manchester. The northwest is convenient for both of those, as well as great transport connections whether that is road or rail, or even air from Manchester (airports were a bit of a consideration when we were thinking about living deeper into north Wales).

We also plan to have two snow dogs, probably an Alaskan Malamute and a husky. For those animals, the colder and more miserable the weather, the better! I find the summers in London a little too warm for my liking, so happy with north-west weather.

Not really.Do you have any fears regarding potential government curve balls for example on access to pension dates or even the TFLS?

Almost all of our pensions have protected minimum pension age, and there is next to no chance of those being retrospectively removed. Our DC pension is £283K in total, of which £232K is mine, so even a lower cap on TFLS is unlikely to hurt unless it is slashed from £268,275 to under about £75,000 which seems unlikely in the next 9 years.

The biggest risk would probably be around State Pension, mainly as that is over 20 years away for us, so plenty of scope for tinkering with a long lead in time. But there are no signs of that under the current Govt. yet, so that should fall to 15 years under the next administration - still a bit too long to be comfortable, but feels a little safer.Is there nothing you can do to better balance your pension provision between the pre and post DB dates as at the moment if you go large on the house you are looking at quite a big jump in income at 55?

It should mostly look after itself. The figures increase very rapidly, as we spend less than than even the c£45K we would have if we were to buy a house and quit work today. So we are 'saving' some of that available income, plus all of our earnings, and every day the 8 year period the funds have to cover is decreasing. Add in returns from investments, and the figures increase rapidly.

Also, I am conservative in estimates about things like what I will sell our current house for. So as the process proceeds, additional funds should be realised as actual figures are better than the estimates.

Nonetheless, I still plan to get an offset mortgage, so that if we were to want to spend more pre-55 we could do so. In practice, that would be just before age 55 as other funds ran out, and even borrowing at, say, 6% p/a, would be an excellent deal to repay it from pension income which has benefited from a 42% increase when putting it into a pension (40% relief on way in, 15% tax on way out). So I plan for this year to put all my wife's higher rate income into a pension, and I will take a view late in the tax year on whether I do the same for me. The benefits are less clear cut for me, as I could struggle to extract all my DC pension without paying higher rate, and am more vulnerable to political change. However, if come March 2025 we are buying or have bought a house with an offset mortgage, then I would dump all my higher rate income into a pension anyhow, as the return is too great to ignore. That means having a lower pre-55 income on paper is actually beneficial, as long as I have the option to borrow and repay from pension income.

I am told the NW is becoming the area of choice for younger retirees, replacing coastal towns which are now regarded as being heavily populated by what have now become very old pensioners after years of being a popular retirement place.george_jetson said:I have always thought NW England would be an ideal region to retire - easy access to major cities and countryside, and Merseyrail meaning you needn’t be reliant on a car. Somewhere on the Wirral near a railway station and a beach would be perfect I think.

I haven't entirely discounted the Wirral peninsula, perhaps just to the east of Bromborough near a country park. But to date I haven't seen a property I particularly like and my target areas are quite limited so I don't expect to end up there. The area is blighted by Birkenhead at the north-end of the peninsula which is a place to avoid, but the areas on the west of the peninsula are very nice too.

@hugheskevi My thoughts regarding living in the north west. It truly would be an excellent choice. I live in the north west and have family scattered around too.

My thoughts - there are some very nice areas on the Wirral (a good choice but avoid the areas where there are mosquitoes due to the marshlands).

Manchester - south Manchester and some areas of Cheshire would be a wonderful choice (and very near to the airport and the Peak District for walks with your dogs). Also well placed for the culture of Manchester and the excellent hospitals.

Frodsham - a beautiful place and just going to throw that in there as somewhere to consider but not as well connected as you may want to have.

North Wales - I can't comment too much on north Wales however do consider how near you are to a well respected hospital. As you get older, you will realise the benefit of this.

Best wishes with your house hunting.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards