We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early-retirement wannabe

Comments

-

If this wasn't Nadine Dorries then why on earth not?Nebulous2 said:

There is a town on a prominent route for us, where I often used to stop for food, or occasionally overnight, when journeying. They elected a politician who was one of my favourite hate figures, and I boycotted the whole town for a long time.

I consider this similarly to when people on the banking board ask about "ethical" mainstream banks. Or is Co-op more ethical than HSBC? Dig beyond the surface puff and they are all about the same, as they share a common factor - the employees are humans, full of human desires, greed, generosity & selfishness.1 -

Anything less than a 4 star hotel is definitely a red line for me.Nebulous2 said:

We all have our own red lines of what is and isn't acceptable to us, and our decisions are our own, regardless of whether other people agree or not.robatwork said:

Isn't that a bit exhausting and problematic, working out which governments fit your criteria of "clean hands"? I only mention as form your map it looks like you have visited China, and lots of places in Africa and Asia where the regimes are at best bonkers, and at worst cruel and inhumane? (Sorry for the OTness)hugheskevi said:

Japan is a country I won't visit on principle, due to the way their Govt. is responsible for the abuse of whales and dolphins. I very much doubt I will ever visit there.eastcorkram said:Any plans for Japan?4 -

My values are very flexible, there isn't much I particularly care about. Off the top of my head, it would only be Japan and the Faroe Islands I would not visit on principle, due to their flagrant animal rights abuses and criminal activities under international law. Not that other countries are much better, but at least most have the decency to put up a pretense, eg the largely unenforced and unenforceable UK fox-hunting legislation, the alleged science behind badger culls, the mass shootings of raptors in certain areas that coincidentally have extensive grouse moors where measures such as brood-management rather than enforcement are employed, etc.robatwork said:

Isn't that a bit exhausting and problematic, working out which governments fit your criteria of "clean hands"? I only mention as form your map it looks like you have visited China, and lots of places in Africa and Asia where the regimes are at best bonkers, and at worst cruel and inhumane? (Sorry for the OTness)hugheskevi said:

Japan is a country I won't visit on principle, due to the way their Govt. is responsible for the abuse of whales and dolphins. I very much doubt I will ever visit there.eastcorkram said:Any plans for Japan?

I'll also try to avoid activities associated with extremely negative environmental impact, eg, I am near Ushuaia in South America now but don't plan to take a boat to Antartica due to the impact on that sensitive region of tourism. I did take a cruise in Alaska and also around Norway in the past, but in general would try to avoid that type of tourism due to the impact of large cruise liners. I'll also try to avoid flying unnecessarily - at the age of 46 I've only taken 22 inter-continental flights despite traveling outside of Europe for 4.5 years in total. I suspect that is quite a lot more inter-continental flights than most, but even so, someone going out of Europe every year for a fortnight of holiday would rack up that many flights in just 11 years, for a total of only 22 weeks of travel. I also won't fly any class other than economy, as I can't justify the greater impact on the environment just for my own comfort for a short time, given I have no health issues, am not especially old, etc.

I don't have any values around human-rights abuses in terms of travel (just my personal values, I respect those that do), the only moral question I have pondered whilst traveling is the extent to which one should abide by local conventions. Usually that isn't an issue, but in countries such as Iran where local conventions are rather strict and perhaps unreasonable, perhaps there is a moral argument that openly exhibiting more liberal attitudes (eg in dressing) could be justified. Although that is often more of an issue for females than males around the world in my experience.

6 -

A refreshingly normal annual update, given the amount of upheaval in the last few years...

My wife and I returned from 16 months of traveling overland from Alaska to Ushuaia (then a bit more of South America) in January this year. If anyone is interested in the trip, I made a detailed post about it on this separate thread, on 13th January 2024, the trip map is below.

One of the most striking details about the trip was that for both of us combined, the annualised cost was £42,000 and that covered everything, including flights, vaccinations, insurance, etc. Once the rent income received is also taken into account that was less than I would spend simply living in London. We both saved up annual leave in advance of the trip, and used as much as possible in advance when we returned from unpaid leave. The combination of rental income, paid leave from work, PAYE refunds, and a few bonuses paid after we left more than covered the entire cost of the 16 month trip.

We are now back living in our London house and both working full-time, preparing for a more conventional early retirement next year. I didn't really want to come back to the UK and immediately have to set about selling our house, so decided to have a year back in London settling back into UK life before then embarking upon house sale. My thoughts are therefore very much about ensuring there are no oversights in my financial planning, and wealth preservation rather than maximisation.

Having just updated my spreadsheets for the new financial year, our position is (now both 46 years old):

I have been building up a decent cash buffer as the most risky period of our retirement will be the period between age 48-54, before pensions are paid. The Investment ISA is cautiously invested as that plus cash will be covering this period. The personal pensions will cover the period 55-68 so are invested in higher risk assets, but still only multi-asset as I prefer to limit the downside rather than maximise return.Non pension assets

House - £542,000 (no mortgage)

Investment ISA - £327,000

Cash (mostly Cash ISAs and Premium Bonds) less all debts - £124,000

Total £995,000

Private pensions (most have protected minimum pension age)

Personal pensions - £269,000 (available at age 55)

DB pensions (pre tax) - £58,400 p/a from age 55 and a further £800 p/a from age 57

(DB pensions are revalued and uprated by uncapped CPI, these figures do not include our State Pensions)

Our assets are mostly evenly divided between us, so we should both be basic rate taxpayers in retirement (£42K p/a and £39K p/a pre-tax including all DB and State Pension) but fiscal drag might change that once State Pension becomes payable. Our DC assets are skewed heavily in my favour, but I should still be able to extract all of them paying only basic rate income tax on withdrawals. I haven't entirely discounted the idea of taking a very part-time job in a local authority so as to be able to transfer pensions and take advantage of the LGPS' integrated AVC scheme - it would be worth around £30,000 of tax relief for me. The sort of jobs that might work would be a 5 hour a week dinner monitor at a local school - I could do that for one term after which a pension transfer would be sorted, maybe something for the future!

We plan to move house and retire in Summer 2025. I expect to buy a house for around £400,000 and incur around £20,000 of moving costs, most of which will be land tax (we might be living in Wales or England, figure is based on Welsh taxation which is higher). I've assumed that the sale of our current house will cover all moving costs, furnishing and decoration, any house maintenance needed, and a new car with nothing left over, although in practice I would expect to have money left over at the end of the move.

Our current position would give us after tax:£53,300 p/a - between aged 46 and 55

Due to traveling, I do not have records of recent expenditure to calculate annual needs, but looking at old records and adjusting for inflation, I'd expect us to spend £35-£40,000 p/a. The Pension Commission in 2004 found that a replacement rate of 50% was sufficient above a particular income, based on our current income (excluding investments and interest) that figure would be 54% (gross) and 68% (net) so that all looks fine. I don't pay much attention to current gross and net income anyhow for retirement purposes, as our income changes considerably depending on things such as travel, unpaid leave, pension contributions, and additional consultancy work.

£70,200 p/a - from age 55

I've been doing some scenario analysis against various metrics to test resilience in certain circumstances. These showed:Total pension for wife if I die (after tax) - £44,700 p/a

Those are reductions to our net income as a couple of about 64-65%. Using common Equivalisation Scales, the survivor income should be £40,700 to £46,800 so that all looks fine. This is based on our long-term position, which would be dying after the age of 68. Earlier death would probably leave a more advantageous position, due to payment of death lump sums from the DB schemes and inheritance of 100% of DC which would then only be supporting one person.

Total pension for me if wife dies (after tax) - £45,800 p/a

To perfectly smooth our income, we need a further £143,000 of cash and £50,000 of DC pension (assuming for calculation convenience that investment returns inclusive of charges equal CPI), which takes into account the cost of voluntary Class 3 contributions in the future to ensure we both have full State Pensions. So we should have plenty already, and a further year or so of work should mean we end up with a bit over £70,000 p/a after tax in all future years. With no mortgage, debts or children and most of the resources being linked to uncapped CPI or better, that should be more than enough in all plausible scenarios.

I'm not sure whether or not I will put higher rate tax income into a pension this year or not. If I do, it will be into DC pension. I'll keep options open until close to the end of the 24/25 financial year and see what the position looks like then. I expect that if at that point we are still expecting to work well into the 2025/26 tax year I will make the pension contribution. It will also be much more attractive to contribute to my wife's DC scheme as she has a lot more higher-rate headroom than I do.

Key risks and management- Investment - mitigated by cautious investment

- Inflation - most assets are protected by uncapped CPI increases

- Care costs (parents) - we still have 2 parents alive. We do not plan on any inheritance, but there is a risk that we will need to contribute to their well-being

- Care costs (us) - hopefully a long way off. We plan to move to an appropriately sized property around age 75-80 which will release equity. We should also have a lot of ISA saving at that point too.

8 -

Good idea not to be in a chain. Reddit is full of horror stories about gazundering. For an offset, does that involve liquidating some ISA and/or PB holdings?1

-

The plan would be to have all our cash ISA holdings in a flexible ISA by the time of purchase, so that I could use them for a deposit and then replenish them with the sale of my current house. We currently have £63K in Premium Bonds, so with ISA flexibility plus Premium Bonds plus other bits and pieces that should add up to whatever we need.Askfirst said:Good idea not to be in a chain. Reddit is full of horror stories about gazundering. For an offset, does that involve liquidating some ISA and/or PB holdings?0 -

Thanks, helpful.

Some of our numbers for comparison/thoughts:

1) Joint gross steady income post retirement about 60k (55k net as unfortunately very skewed to one earner) - aim for survivor to only lose equivalent on 1 state pension, will do this by taking reduced pension as soon as available and allocating enough to DW that she will get the sae pension as me on my death.

2) One way of protecting fund for the 'bridging' periods to DB and then state pension is an index linked gilts ladder, this removes all market and inflation risk at the cost of any possible growth, given current linker prices the cost from a isa/dc pot is basically the number of years times the current value.I think....2 -

It finally feels like we've started the beginning of the end on the route to conventional early retirement, albeit early retirement at what will be a relatively young age of 47.

Everything in our lives will change, as we relocate to a new area, get a new car, dispose of most of our things, purchase new stuff, and finally quit work. We will get two rescue dogs and set up a whole new life in a new area as we move away from London.

Since April I have been researching where we will move to within north-east Wales and north-west England. The best places for us tend to be the outskirts of a town, where we have immediate access to a large green space for dogs and running, but where there will also be a leisure centre for gym, classes, and swimming, and also a running club. Proximity (about 1-hour drive) to a major city is also desirable. The places we are most likely to move, with links to the property I like the most in each area, are Congleton, Whitchurch, Wrexham, or Buckley.

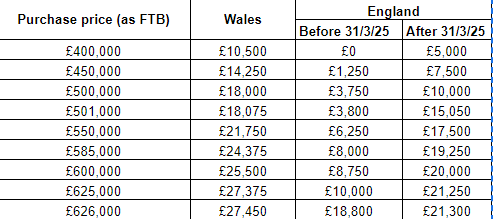

I suspect however that we won't move to Wales. A key reason for this is the Welsh government. We would have to pay a large premium in Stamp Duty (Land Transaction Tax in Wales), which is very hard to justify. There is also the way Welsh govt. handled COVID, the 20mph debacle, and the First Minister mess which makes it less attractive, especially as the direction any future variation to things like income tax rates would go seems clear. We would have to pay an additional £16,375 of Stamp Duty to live in Wales, compared to an equally priced house in England, which is less than 5 miles away from both Buckley and Wrexham. I struggle to justify that.

Sadly my hopes to extract my DC pension tax-free via a future transfer to the LGPS won't work. But on the positive side, we may well be able to take advantage of my wife being a first-time buyer to get a Stamp Duty discount in England. To do that, we would need to sell our current house (which is solely in my name) before we could buy somewhere as otherwise she would be ineligible due to having an interest in a property, then my wife could buy our next property solely in her name as a first time buyer. That would all need to be done by 31st March 2025. The difference in Stamp Duty is considerable, saving around £12,000.

The table below shows the Stamp Duty (Land Transaction Tax in Wales) due on properties in the range we expect to spend, based on being a First Time Buyer. There are an alarming amount of cliff-edges to avoid falling foul of, more well-designed fiscal policies!

We plan to wait until the Budget at the end of October and then immediately view properties, so the financial landscape should be clear when we view and consider making offers. I have almost finished moving all our cash ISAs to flexible ISAs, and could raise about £200,000 in cash almost immediately, or a bit over £500,000 if I also included stocks and shares ISAs (transferred to flexible cash ISA before withdrawing as our current SSISA is not flexible). That would enable my wife to buy somewhere, probably with a modest offset-mortgage separate to selling our house - although I would have to sell our house before buying somewhere for her to be a first time buyer.

Taking into account selling the current house, paying off all debt, buying a car costing £20,000 (probably a newish MG5), spending £20,000 on new furnishings, and all costs of moving (incl. Stamp Duty), the position based on immediately retiring and buying a new property today would be: (based on moving to Wales, as that is the worst-case scenario from a financial perspective)

I plan to market our property on Boxing Day, subject to any Budget changes. That is a bit earlier than I had planned, but with all the Stamp Duty cliff edges I expect that if there are no changes at Budget there will be huge property market activity to get sales through for changes due for implementation on 31st March 2025. If it doesn't all come together in time, it just means a bit of extra tax, which isn't much in the great scheme of things.

We intend to keep working until after we have moved into our new house, and give notice at that point (3 months). That will derisk everything, as we can carry on working if we wish (eg if costs are higher than expected). It is more about keeping all options open rather than managing risk though, as everything looks very comfortable. Therefore I expect to leave work sometime between June and December 2025, as working Jan-Mar 2026 would have nil Bank Holidays and all be taxed at higher rate, so I can't see myself wanting to work beyond Christmas at the latest just to have to pay a lot of salary in tax.

At age 55 our pensions will give us an annual net income of just over £70,000 p/a for the rest of our lives, initially from DB and DC pensions. From State Pension age, our State Pension and Defined Benefit pensions will provide a minimum of (in today's price terms):

For now, life is rather mundane, as I work my way through a list of things to do in my existing house to get the exterior and interior into shape - nothing very much, just minor DIY work over the next couple of months to be ready for whatever comes out of Budget. Then everything should get a lot more interesting and start moving fast.11 -

Informative update as usual.

How has returning to 'real life' after travelling worked? Seems you are very adaptable as I suspect many would struggle to return to the norm after such an amazing trip.

Any reason for the NW England location choice, are there family commitments as otherwise you could probably chose somewhere with better weather!

Do you have any fears regarding potential government curve balls for example on access to pension dates or even the TFLS? Is there nothing you can do to better balance your pension provision between the pre and post DB dates as at the moment if you go large on the house you are looking at quite a big jump in income at 55?I think....2 -

I have always thought NW England would be an ideal region to retire - easy access to major cities and countryside, and Merseyrail meaning you needn’t be reliant on a car. Somewhere on the Wirral near a railway station and a beach would be perfect I think.However the prospect of free public transport in London from age 60 (plus all the free museums and galleries etc) is a major argument for staying put here…MFW Challenge: Mortgage free in 2008! ACHIEVED!

2

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 248K Work, Benefits & Business

- 605.2K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards