We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Northern Rock PPI Refund - CCA now valid?

Comments

-

Someone has kindly offered to help, so this should be up shortly.

LBM - Jan'10

LBM - Jan'10

DMP Start - 01st March 2010 - Debt £31,614

Debts at Highest - £36k Mid Jan 2010

Debt Free Date 22nd December 2015!

DMP - Just do it, don't hesitate.0 -

Sorry for the delay, your PM didnt show up :P

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock1.jpg

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock2.jpg

http://i892.photobucket.com/albums/ac126/nonnynonny123/nrock3.jpgAlthough no trees were harmed during the creation of this post, a large number of electrons were greatly inconvenienced.

There are two ways of constructing a software design: One way is to make it so simple that there are obviously no deficiencies, and the other way is to make it so complicated that there are no obvious deficiencies0 -

I have absolutely no experience of enforceability of loan agreements etc, but I have just read your uploaded letters and the section on prescribed terms (kindly linked to by Dark Convict) and my personal thoughts are (not in any logical order mind you:o)

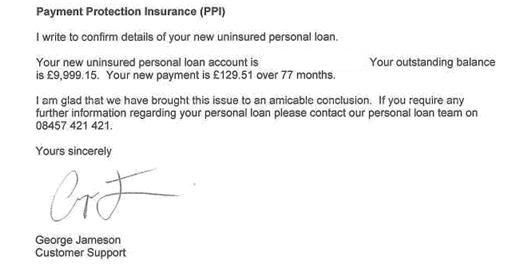

- The wording 'This is the balance we will transfer to a new, uninsured loan means (to me) that they closed the first loan and gave you a complete new loan.

- The new loan had different monthly payments from the first loan.

- They clearly set up a new loan account and this is confirmed by the new account number.

- The paperwork does not state that the terms and conditions of the initial loan will continue to remain in force for the remainder of the new loan.

- The paperwork does not detail, nor ask for signature for any new terms and conditions for the new loan.

- The paperwork does not detail any APR for the new loan

- There is no breakdown given of loan value and amount of interest anywhere.

- There is no start /end date information, ie 77 monthly payments of XXX.XX commencing xx/xx/xx

- Based on the above I think the CCA for the first loan would be null and void and not applicable to the new loan - as mentioned above they clearly settled the first loan and opened up a new acount.

- In one document they quote a monthly repayment of £128.51 and in another they quote £129.51 - very confusing.

- In one document they mention the balance as just over £10k and in another it is just under £10k.

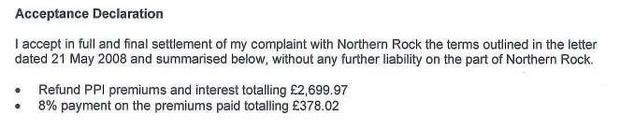

- The acceptance declaration you signed doesn't state anything about terms and conditions for a new loan - rather it just refers to settlement of the PPI and interest

However, I am sure someone with far more experience and knowledge of this sort of thing will be along to give far better advice. These really are just my thoughts:beer:NR [STRIKE]£5542[/STRIKE]£2771 BC [STRIKE]£7987[/STRIKE]£7700 BC [STRIKE]£3000[/STRIKE]£5100 Cat1 Pd Cat2 Pd Ulstr [STRIKE]£3400[/STRIKE]£3070 TSB [STRIKE]£4851[/STRIKE]£4400 MBNA [STRIKE]£7700[/STRIKE]£3887 NWst [STRIKE]£950[/STRIKE] £700 Hfx [STRIKE]£10097[/STRIKE]£10050 Asda [STRIKE]£398[/STRIKE] £315 HFX1 Pd Hfx2 [STRIKE]£3133[/STRIKE] £3000

LBM 15/1/10 £47,728 now £40,993 14.11% pd

Snowball at LBM [STRIKE]1050[/STRIKE] 871 days left (745 days to Olympics 2012)

£365/365 - £388 (that's for DH & me!)0 -

Hello planning ahead,

I am glad the members here can now read the documents,

everything you mention above is exactly my reasoning for posting these here - hope some other people will offer an opinion and then i can see what is best to do.

It mentions in the letter 'we will not ask your client to sign a new credit agreement' (i used a third party company for the PPI claim).

Surely they must have a credit agreement to continue the loan, and if i CCA them, what exactly will they produce do you think?LBM - Jan'10

DMP Start - 01st March 2010 - Debt £31,614

Debts at Highest - £36k Mid Jan 2010

Debt Free Date 22nd December 2015!

DMP - Just do it, don't hesitate.0 -

nonnynonny wrote: »It mentions in the letter 'we will not ask your client to sign a new credit agreement' (i used a third party company for the PPI claim).

Surely they must have a credit agreement to continue the loan, and if i CCA them, what exactly will they produce do you think?

I think NR have 'assumed' the original credit agreement would continue. However, they haven't made that statement anywhere - the only sentence relating to CCA is the one about 'we will not ask your customer to sign a new Credit Agreement'. I would not think they can 'assume' anything when dealing with a loan of any amount, let alone £10k and therefore I don't think they would have an argument that the original agreement could be considered to cover the completely new loan as it is for a different loan value and repayment schedule from the first, together with a completely new account number - therefore (to me) it can have no relation to the original loan/CCA.

To me the wording on the all paperwork seems as if it has almost been written by an office junior/clerk rather than having gone through any legal team at NR - it is just so short/simple. I mean don't they ususally offer things like this by heading the letter 'without prejudice' or something like that?

As I said above, I have no background or experience in this sort of thing and this is my 'simplistic view' - what you really need someone iswith more knowledge than me on this.

I do think someone at NR really stuffed up the paperwork on this settlement and if yours is this bad I wonder how many more are out there waiting to be challenged:)NR [STRIKE]£5542[/STRIKE]£2771 BC [STRIKE]£7987[/STRIKE]£7700 BC [STRIKE]£3000[/STRIKE]£5100 Cat1 Pd Cat2 Pd Ulstr [STRIKE]£3400[/STRIKE]£3070 TSB [STRIKE]£4851[/STRIKE]£4400 MBNA [STRIKE]£7700[/STRIKE]£3887 NWst [STRIKE]£950[/STRIKE] £700 Hfx [STRIKE]£10097[/STRIKE]£10050 Asda [STRIKE]£398[/STRIKE] £315 HFX1 Pd Hfx2 [STRIKE]£3133[/STRIKE] £3000

LBM 15/1/10 £47,728 now £40,993 14.11% pd

Snowball at LBM [STRIKE]1050[/STRIKE] 871 days left (745 days to Olympics 2012)

£365/365 - £388 (that's for DH & me!)0 -

Hi nonnynonny

Is there a particular reason you want to try and go down the route of unenforceability - other than because you possibly can?NR [STRIKE]£5542[/STRIKE]£2771 BC [STRIKE]£7987[/STRIKE]£7700 BC [STRIKE]£3000[/STRIKE]£5100 Cat1 Pd Cat2 Pd Ulstr [STRIKE]£3400[/STRIKE]£3070 TSB [STRIKE]£4851[/STRIKE]£4400 MBNA [STRIKE]£7700[/STRIKE]£3887 NWst [STRIKE]£950[/STRIKE] £700 Hfx [STRIKE]£10097[/STRIKE]£10050 Asda [STRIKE]£398[/STRIKE] £315 HFX1 Pd Hfx2 [STRIKE]£3133[/STRIKE] £3000

LBM 15/1/10 £47,728 now £40,993 14.11% pd

Snowball at LBM [STRIKE]1050[/STRIKE] 871 days left (745 days to Olympics 2012)

£365/365 - £388 (that's for DH & me!)0 -

Hello,

It may be the difference between taking on a DMP and not, and if i can get those at Northern Rock, i would love to.

If i can hassle Northern Rock and prove this unenforcable then i should have the facility to stay 'live' if you like, and avoid a DMP.

The £129 a month will become £300 a month additional to my income in 12 months time when a tesco loan completes, i can then start to chip away at 2 other cards (3.5k Virgin, 4.5k Halifax) and cahoot overdraft 1k and flexible loan - now closed, which caused the problem - of £3k.

I have around £520 a month for shopping, fuel e.t.c so the £129 released will give almost £650 and then in a years time it will be near £800, so this is my dilema.LBM - Jan'10

DMP Start - 01st March 2010 - Debt £31,614

Debts at Highest - £36k Mid Jan 2010

Debt Free Date 22nd December 2015!

DMP - Just do it, don't hesitate.0 -

If I was in your situation then I admit I would go for it. I don't think you have anything to lose - but I wish someone else with more knowledge would come along and offer you advice.

My advice is just my thoughts and therefore not really worth anything.

Good luck and please let us know how you get on whichever way you decide to go.NR [STRIKE]£5542[/STRIKE]£2771 BC [STRIKE]£7987[/STRIKE]£7700 BC [STRIKE]£3000[/STRIKE]£5100 Cat1 Pd Cat2 Pd Ulstr [STRIKE]£3400[/STRIKE]£3070 TSB [STRIKE]£4851[/STRIKE]£4400 MBNA [STRIKE]£7700[/STRIKE]£3887 NWst [STRIKE]£950[/STRIKE] £700 Hfx [STRIKE]£10097[/STRIKE]£10050 Asda [STRIKE]£398[/STRIKE] £315 HFX1 Pd Hfx2 [STRIKE]£3133[/STRIKE] £3000

LBM 15/1/10 £47,728 now £40,993 14.11% pd

Snowball at LBM [STRIKE]1050[/STRIKE] 871 days left (745 days to Olympics 2012)

£365/365 - £388 (that's for DH & me!)0 -

Thanks, i hope someone else can take a look.

After my experiences over on the CAG forum, i am glad this site seems more friendly and people are actually interested and enthusiastic for the topics.LBM - Jan'10

DMP Start - 01st March 2010 - Debt £31,614

Debts at Highest - £36k Mid Jan 2010

Debt Free Date 22nd December 2015!

DMP - Just do it, don't hesitate.0 -

I found CAG hard to navigate the forums, but i found their templates easier to find. Didn't stay long enough to really vouch for the community.Although no trees were harmed during the creation of this post, a large number of electrons were greatly inconvenienced.

There are two ways of constructing a software design: One way is to make it so simple that there are obviously no deficiencies, and the other way is to make it so complicated that there are no obvious deficiencies0

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards