We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Option ARM timebomb set to explode....

Comments

-

To put it another way, how many that have reset already have been foreclosed?

I'm sceptical of things that are going to be a disaster that haven't been reported in the FT or The Economist in any particular depth.0 -

C0ckmunch

Your intelligent and coherant arguments are clearly winning the day.

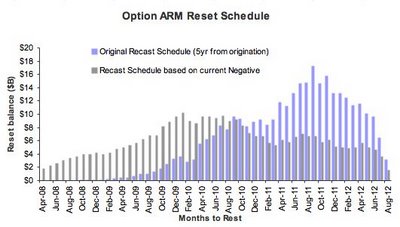

It might hep it you stopped cutting and pasting a graph you don't understand, and cutting and pasting from other peoples blogs that you don't understand either, and maybe make an argument yourself, and back it up with FACTS, rather than the opinions of other people.'In nature, there are neither rewards nor punishments - there are Consequences.'0 -

Purch Go on then, counter the argument C0kcmunch. Show me I am wrong.

Generali, I take it the FT picked up on the same arguements just prior to October 2007 then? Despite all the evidence staring them in the face?

As to previous resets, its pretty obvious the scale of resets prior to 2009 due to option arm are miniscule.

Will the WSJ do you?

http://online.wsj.com/article/SB121798100185115205.html?mod=yahoo_hs&ru=yahooLOS ANGELES -- Like many mortgage lenders, FirstFed Financial Corp. is struggling with rising losses. The bank posted a loss of nearly $70 million in the first quarter -- reversing years of profit. Forty percent of its borrowers became at least 30 days delinquent after the payments on their adjustable-rate mortgages were recast. The number of foreclosed homes held by the bank doubled in the second quarter from the first quarter.

#other points:- The number of foreclosed homes held by the bank doubled in the second quarter from the first quarter.

- the Los Angeles bank (First Fed) is on the front lines of what could be the next big mortgage debacle: payment option mortgages.

- These loans went mainly to people with good credit, but they are likely to experience defaults that are nearly as high as — in some cases higher than — those for subprime.

- Barclays Capital estimates that as many as 45% of option ARMs originated in 2006 and 2007 could wind up in default.

- UBS AG, suggests that defaults on option ARMs originated in 2006 could be as high as 48%, slightly higher than its estimate for defaults on subprime loans.

- FirstFed’s experience highlights the challenges lenders face as option ARMs recast.

- FirstFed is a relatively small lender, with just $7.2 billion in assets.

- option ARMs were “a very good loan for the borrower and the bank” for more than 20 years. But that changed, she said, when investment-banking firms entered the industry and set lower lending standards, which FirstFed and others followed.

- As long as interest rates were flat or falling, the minimum payment was enough to cover the interest due, making the option ARM equivalent to an interest-only loan in the early years of the mortgage.

- As competition increased, lenders dropped the introductory rate on option ARMs to 1% or even lower and made more loans to borrowers who didn’t fully document their income or assets.

- Rather than shut its doors, FirstFed joined the crowd and business boomed.

- borrowers making the minimum payment weren’t covering even the interest due.

- Others lenders are seeing borrowers fall behind even before recasts.

- FirstFed is scrambling to modify the loans of borrowers who can’t afford the higher payments.

- Instead of waiting for borrowers to fall behind, the company sends borrowers letters as their loan balances swell, offering them a chance to modify their mortgages. From January through June, the company had modified 705 loans totaling $345 million.

- Many borrowers took out home-equity loans with other lenders after getting an option ARM from FirstFed..

0 -

Pi$$ off steve. If you havent got the intellect to come up with a counter argument dont bother.

People want to hear justification why these are not green shoots of recovery but a bull trap plain and simple.

You have previously called these loans prime lending. Prime lending with a self-cert rate of 83%?

A product that 80% are making continuous mimimum payments, despite the economic carnage they are about to reap upon themselves.

Do yourself a favour. look up the definition of Full Amortization and compare payments from minimum payment to Full Amortization....

There is no point conversing with half wits. Stevie responds to most posts I've seen with a lot of nonsense. Trying to make halfwitted "joke" comments just emphasise the lack of intelligence.

Stevie, if you can't understand, Butt out, there is no point in trying to wind up people.0 -

Ah yes, the 18 month old graph that was produced prior to interest rate cuts.This is a system account and does not represent a real person. To contact the Forum Team email forumteam@moneysavingexpert.com0

-

Go on then, counter the argument C0kcmunch. Show me I am wrong.

Generali, I take it the FT picked up on the same arguements just prior to October 2007 then? Despite all the evidence staring them in the face?

If we want to say that there are going to be problems caused by these mortgages resetting then perhaps the best thing to do is to look at the foreclosure rate from those that have reset so far. Any idea what this is?

mbga9pgf, I'm really not known for my bullish calls on the economy on this board but there are limits. These mortgages would be a problem if they were going to be reset at rates of 10% or something.

The thing is that if the lenders do that then the courts won't allow lenders to foreclose, they'll force lenders to renegotiate terms instead.

The biggest change over the course of the financial car crash we've witnessed over the past 2 years is the amazing political reaction to it IMO.

Your post seems to be assuming that the forces of today will be met using the political rules of a couple of years back.

I suspect this whole thing will end in disaster. That doesn't mean that some bloke with a keyboard, a graph and his Dad's old sandwich board "The End is Nigh" is correct.0 -

Generali, Business Weekly highlighted the danger of these loans as far back as 2006.

http://www.businessweek.com/magazine/content/06_37/b4000001.htm

I wonder how much burying of heads in the sand is going on presently... I would be interested to see how many in the know are deeply re-invested and how many have their cash reserves out of equities at the mo.

I cant imagine many will be going out and splashing the cash on houses though tbh.0 -

Ah yes, the 18 month old graph that was produced prior to interest rate cuts.

Yes, with the products that were issued with 1% teaser rates, with a product you could make payments that didnt even cover the interest for the first 5 years... Those resets are now due. Most of which (80%) are facing mortgage payments of 110-125% of the original loan.

See the significance? Or are you a bit thick?0 -

Generali, Business Weekly highlighted the danger of these loans as far back as 2006.

http://www.businessweek.com/magazine/content/06_37/b4000001.htm

I wonder how much burying of heads in the sand is going on presently... I would be interested to see how many in the know are deeply re-invested and how many have their cash reserves out of equities at the mo.

I cant imagine many will be going out and splashing the cash on houses though tbh.

Great. I've been clear that mortgage markets have posed a significant risk to world economies since 2005.

My point remains - what data do you have to show to back up your argument given policy responses over the last couple of years?0 -

mbga9pgf, I'm really not known for my bullish calls on the economy on this board but there are limits. These mortgages would be a problem if they were going to be reset at rates of 10% or something.

How does 40% doodle do you then?

http://online.wsj.com/article/SB121798100185115205.html?mod=yahoo_hs&ru=yahoo

Edit: sorry, 40% default rate. Still pretty serious. As I said, an increase of between 60%-102% overnight (which 80% of these mortgage holders face) is a bloodbath waiting to happen. The figures are out there, in trustworthy articles and are widely knoiwn about. Dropping IRs will delay the recast, but as sure as eggs are eggs, those 80% making minimum payments still face growing mortages in a declining market. When are they going to start paying off these mortgages, and what happens when they finally do reset?0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards