We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Looks like the bank losses are stopping Goldman Sachs post $1.8bn 1st 1/4 profit.

Really2

Posts: 12,397 Forumite

Looks like the US banks have now got there head above the water.

http://news.bbc.co.uk/1/hi/business/7997377.stm

Goldman Sachs has reported a $1.8bn (£1.2bn) net quarterly profit, beating analyst expectations and a day early. In contrast, the previous quarter had seen the firm post its first quarterly loss since going public in 1999.

http://news.bbc.co.uk/1/hi/business/7997377.stm

Goldman Sachs has reported a $1.8bn (£1.2bn) net quarterly profit, beating analyst expectations and a day early. In contrast, the previous quarter had seen the firm post its first quarterly loss since going public in 1999.

0

Comments

-

We are in the dip.

See:

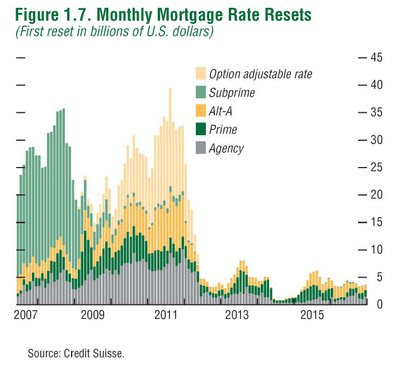

It isnt going to be pretty once those option ARM resets start to hit home, which, apparently could be a bigger problem than sub-prime.

Oh, Alt-A is going to be a little problem for them too. :eek::eek::eek:0 -

Should they not still be writing down?

Are those figures in the graph not hypothetical?

What affect does the "Troubled Asset Relief Program" have on that graph?0 -

Nobody wants to read your good news on here.

Move along nothing to see here..

Doomed were all doomed.0 -

The International Monetary Fund is likely to raise its estimate of total credit losses on US assets from $2,200bn to about $2,800bn when it releases its Global Financial Stability report later this month.

The IMF is also expected to release for the first time an estimate of total losses on European assets, which is likely to exceed $1,000bn.

The fund is likely to put total losses globally at slightly above $4,000bn, including some additional losses on Asian assets.

Experts think that up to three-quarters of these losses will fall on banks globally, with the balance hitting other financial institutions.

Source:

http://www.ft.com/cms/s/0/40d39f36-23d6-11de-996a-00144feabdc0,dwp_uuid=5c2cbae4-433f-11db-9574-0000779e2340.html?nclick_check=1

There are still big big losses out there. The report from the IMF is due 20/04.If many little people, in many little places, do many little things,

they can change the face of the world.

- African proverb -0 -

Should they not still be writing down?

I don't know how all banks work. I know that some are posting two sets of figures some initial figures and some a few days later with write downs included. I don't know if all figures are public or if some are just for the IMF or Bank of England or what.") I'll pay better attention this month. 0

I'll pay better attention this month. 0 -

Should they not still be writing down?

Are those figures in the graph not hypothetical?

What affect does the "Troubled Asset Relief Program" have on that graph?

Those figures are not hypothetical. They are real. TARP is too small to account for the losses we will see in 2010. They are going to need a bigger bailout.

I believe they are still writing down however, at nowhere near the levels we saw last year. They WILL spike again though, especially when you understand how an option ARM mortgage works.An "option ARM" is typically a 30-year ARM that initially offers the borrower four monthly payment options: a specified minimum payment, an interest-only payment, a 15-year fully amortizing payment, and a 30-year fully amortizing payment.[4]

These types of loans are also called "pick-a-payment" or "pay-option" ARMs.

When a borrower makes a Pay-Option ARM payment that is less than the accruing interest, there is "negative amortization", which means that the unpaid portion of the accruing interest is added to the outstanding principal balance. For example, if the borrower makes a minimum payment of $1,000 and the ARM has accrued monthly interest in arrears of $1,500, $500 will be added to the borrower's loan balance. Moreover, the next month's interest-only payment will be calculated using the new, higher principal balance.

Option ARMs are popular because they are usually offered with a very low teaser rate (often as low as 1%) which translates into very low minimum payments for the first year of the ARM. During boom times, lenders often underwrite borrowers based on mortgage payments that are below the fully amortizing payment level. This enables borrowers to qualify for a much larger loan (i.e., take on more debt) than would otherwise be possible. When evaluating an Option ARM, prudent borrowers will not focus on the teaser rate or initial payment level, but will consider the characteristics of the index, the size of the "mortgage margin" that is added to the index value, and the other terms of the ARM. Specifically, they need to consider the possibilities that (1) long-term interest rates go up; (2) their home may not appreciate or may even lose value or even (3) that both risks may materialize.

Option ARMs are best suited to sophisticated borrowers with growing incomes, particularly if their incomes fluctuate seasonally and they need the payment flexibility that such an ARM may provide. Sophisticated borrowers will carefully manage the level of negative amortization that they allow to accrue.

In this way, a borrower can control the main risk of an Option ARM, which is "payment shock", when the negative amortization and other features of this product can trigger substantial payment increases in short periods of time.[5]

For example, the minimum payment on an Option ARM can jump dramatically if its unpaid principal balance hits the maximum limit on negative amortization (typically 110% to 125% of the original loan amount). If that happens, the next minimum monthly payment will be at a level that would fully amortize the ARM over its remaining term. In addition, Option ARMs typically have automatic "recast" dates (often every fifth year) when the payment is adjusted to get the ARM back on pace to amortize the ARM in full over its remaining term.

For example, a $200,000 ARM with a 110% "neg am" cap will typically adjust to a fully amortizing payment, based on the current fully-indexed interest rate and the remaining term of the loan, if negative amortization causes the loan balance to exceed $220,000. For a 125% recast, this will happen if the loan balance reaches $250,000.

Any loan that is allowed to generate negative amortization means that the borrower is reducing his equity in his home, which increases the chance that he won't be able to sell it for enough to repay the loan. Declining property values would exacerbate this risk.

Option ARMs may also be available as "hybrids," with longer fixed-rate periods. These products would not be likely to have low teaser rates. As a result, such ARMs mitigate the possibility of negative amortization, and would likely not appeal to borrowers seeking an "affordability" product.

One important word above there. Negative amortization.

:rotfl::rotfl::rotfl::rotfl:

I just love it. Its a mortgage that GETS BIGGER ha ha ha!

Worth noting job losses have not peaked as of yet in the US or the UK. not gloating, observing. Until they do, repossessions wont stop nor will the write downs.0 -

to repay an emergency $10bn loan provided by the US government

So already the TARP "Bailout" funds that are a such a huge millstone around the necks of future generations, and must all be considered a 'writeoff' for the Government are starting to be repaid !!!'In nature, there are neither rewards nor punishments - there are Consequences.'0 -

Those figures are not hypothetical. They are real. TARP is too small to account for the losses we will see in 2010. They are going to need a bigger bailout.

I believe they are still writing down however, at nowhere near the levels we saw last year. They WILL spike again though, especially when you understand how an option ARM mortgage works.

One important word above there. Negative amortization.

:rotfl::rotfl::rotfl::rotfl:

But they do not know if the reset rate wil be higher so do not know if will triger defaults. To me a fair bit of that graph is hypothetical.0 -

lostinrates wrote: »I don't know how all banks work. I know that some are posting two sets of figures some initial figures and some a few days later with write downs included. I don't know if all figures are public or if some are just for the IMF.

They were producing writedowns in quarters before. I can't see them being alowed to change acounting methods.

In the US they have to write down loans to the asset value on the open market as far as I know (simplisticaly).0 -

That graph simply shows when mortgages reset. it does not predict the scale of the losses. All we have to go on is what has happened before in relation to the graph and correlate what will happen in the future with the graph.they do not know if the reset rate wil be higher

you want to hazard a guess at the reset rates for sub-prime, alt-a (liar loan) and Option ARM mortgages? We aint talking base +1% here!0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards