We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

MSE News: Best-buy savings accounts often beat investing in stock market, study...

Legacy_user

Posts: 0 Newbie

Putting money into a best-buy savings account may no longer be the poor relation of investing in shares...

Read the full story:

'Best-buy savings accounts often beat investing in the stock market, study finds'

Click reply below to discuss. If you haven’t already, join the forum to reply. If you aren’t sure how it all works, read our New to Forum? Intro Guide.

'Best-buy savings accounts often beat investing in the stock market, study finds'

Click reply below to discuss. If you haven’t already, join the forum to reply. If you aren’t sure how it all works, read our New to Forum? Intro Guide.

0

Comments

-

Of course what the comparison with cash should comprise is a well diversified portfolio of investments and not a comparison with one tracker that most people would never have as their only investment. If a sensible comparison was made there would only be one hands-down winner. How many people would have a Footsie 100 tracker as their only investment? It's stating the obvious that you could hit problems at times.

But, even after all that, the tracker still won over the whole 21-year period. So, what's the point? As far as I can see the only point seems to be that if you make an extremely poor investment decision, sometimes you would have been better in cash if you hunted down the best deals. But even then overall the extremely poor investment decision can still come out on top over an extended period.0 -

So they compared someone who was happy to research best buy accounts and fill in the forms to transfer each year with someone who just stuck the money in the FTSE 100 without considering any kind of diversification.

It makes very little sense to assume that someone who put the effort into getting the best possible cash deal would not put similar effort into researching stockmarket investments, which means it is extremely unlikely they would just put it all in the FTSE 100 of all indices.

And they still needed to restrict the data to post 1995 (i.e. just before the dot-com crash) to get the conclusion they wanted.

Very poor research. But if it makes mattress-stuffers happier to believe it then it's no skin off my nose.0 -

Does anyone know, 1) what fees they assumed on the tracker (which can go into a PEP/ISA), 2) what tax they assumed would be payable on the cash interest (which can't at decent rates for much of the last decade)?I am not a financial adviser and neither do I play one on television. I might occasionally give bad advice but at least it's free.

Like all religions, the Faith of the Invisible Pink Unicorns is based upon both logic and faith. We have faith that they are pink; we logically know that they are invisible because we can't see them.0 -

The link is here

http://www.bbc.co.uk/news/business-36531071

Rather disappointing that they created such a missed opportunity and potentially misleading headlines. Why just stick with FTSE100 when that's not considered sensible, balanced investing? The presenter of a programme called MoneyBox should know better.Remember the saying: if it looks too good to be true it almost certainly is.0 -

Even with all of the flaws the end result is interesting in one way: £28,105 if using accounts available for small amounts of money vs £34,098 using a share tracker available for any practical amount of money. That's a big long term cost for using cash and in other numbers he suggests that the loss is about 20% a year (that is, shares grew by 20% more before tax effects than cash did, so 6% vs 5%).

Some of the ways in which the results appear to have been loaded, though presumably not with intent, in one particular direction include:

1. Ignoring income tax that is normally paid on interest. It's not normally paid on dividends or capital gains and the reasoning he gives only applies to small amounts of money (the allowance of up to £1,000 of interest being tax free) or in ISA or pension accounts where you can't get the best interest rates but can get the best equity returns.

2. Assuming a perfect shopper for savings who always chose the best rates but choosing a mediocre share tracker fund but not disclosing what its charges were. They could have been 1.5% or more. Today they are reasonably competitive at 0.17% but that is probably not so for the whole period. The comparison suggests that the actual charges were 1.3% a year because that is the difference between the Equity Gilt study returns without charges and the returns with charges that he gives.

3. The fund used is "HSBC FTSE 100 Index Retail Income" but the results are described as for dividends being reinvested. The income versions of funds don't reinvest the dividends, they pay them out. Even so the results suggest that dividends must have been accounted for somehow because they are too good to be ignoring them.

4. The choice of fund was poor given that it was relatively easy to select far better performers during the times being considered.

5. The choice of stock market index was poor being the UK only.

6. The choice of investments was poor, being equities only rather than the more normal advice to use a mixture of equities and bonds and rebalance around annually, an approach which has been shown to produce an increase of 0.5-1% in investment returns.

7. The best buy term deposit account was selected from those available for amounts "less than £2500 where possible and not exceeding £10,000". It's relatively easy to get above normal rates on relatively small amounts of money.

What's interesting is that all of those effects move the results in directions which make cash look better.

What could have been very interesting was the data set for the best buy term deposit account so it could have been compared to other studies like the Equity Gilt Study. Unfortunately it isn't made available.

It's also interesting he appears to be using a study that doesn't use real shares or stock markets but instead seems to be using a mathematical model to assert that the riskiness of shares purchased and held for longer periods doesn't decrease when studies of real markets show that it does and very substantially so.

If you choose a more capable investor they might also be aware of the Guyton rule for taming sequence of returns risks that uses Shiller's cyclically adjusted price/earnings ratio result to increase returns by about 1% by selecting the best and worst times to hold equities and adjusting the amount accordingly. Though that's a little unfair because it's doable now but the research is relatively recent so it's more relevant for people deciding now than the results of this.0 -

Paul Lewis was talking on You and Yours, today on Radio 4, about 28 minutes into the program. He is using "BEST BUY" cash deposit accounts. 20 years ago, 5% one year bond was easy to get.

"one-year deposit account"?

I supposed a set of well spaced out Regular Savers could be considered "One Year" Savings accounts, but otherwise the one year bonds these days are pretty dire. NS&I has just dropped the interest rate on Income Bond from 1.25% down to 1.00%.

The tax regime does not favour interest these days.

Assume a person makes £30k, so has about £13k of 20% tax band left. If you use up the £1,000 Savings Allowance, which is easily done with the usual 3~5% current accounts and Regular Savers, you start paying 20% tax. If you had £100k, and you managed to set up A LOT of these 5% accounts, you get £5,000 of interest, of which £1,000 is tax free, but £4,000 pays 20% tax.

If you got 5% in either dividends or capital gains by investing the £100k, it's all TAX FREE. £5,000 tax free for dividend (starting this year), and £11,100 tax free for capital gains. Even if you manage to exceed the allowances, the tax rate is 7.5% (dividend) and 10% (capital gains).

For the higher tax payer:

Savings 40%

Dividend 32.5%

Capital Gains 20%

Still better to get dividend and capital gains.

In extremis, getting 1% interest and paying 40% tax is self-abuse.

As far as I'm concerned, use up the £1,000 Savings Allowance, and then aim for dividend and capital gains. Use up the £5,000 and £11,100 allowances first, which is quite a job already.0 -

Wasn't there a report or a book or something "monkey with a pin" a while back which also claimed that the return from cash wasn't nearly as bad as portrayed by the financial industry ? Again, because the numbers quoted for cash were always base rates or normal savings accounts or something.0

-

Always interesting to see the cash v equities comparisons..

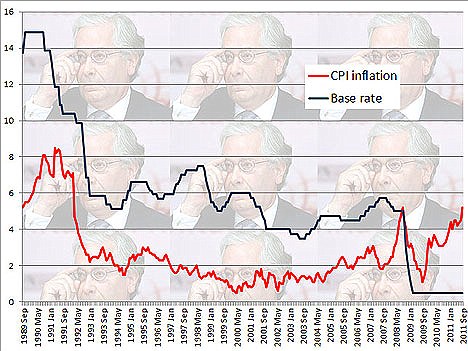

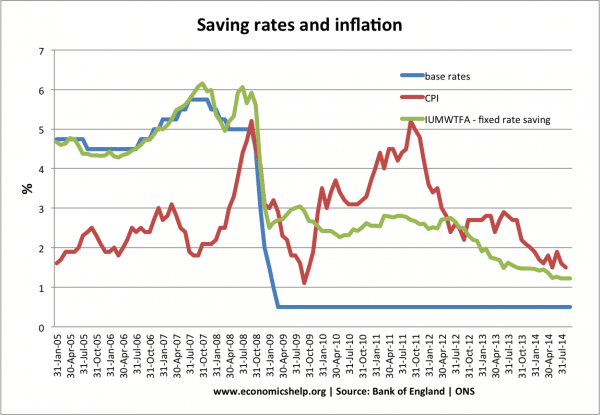

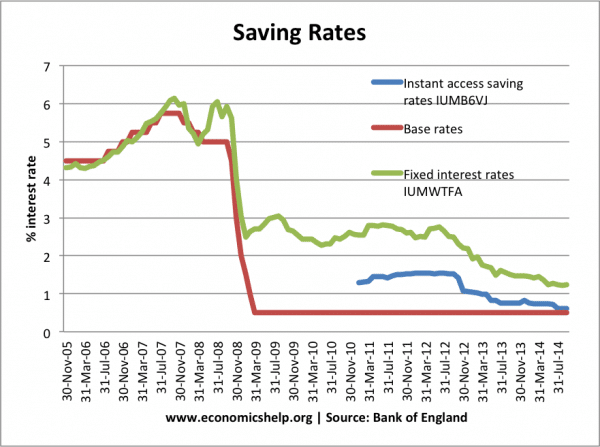

Looking at the link below from the BOE you can see during the period 1995 to present 2016 base rates have been in single figures.

I would imagine it wouldn't be hard to pick up a savings rate which didn't match or even beat the base rate.

http://www.bankofengland.co.uk/boeapps/iadb/Repo.asp

Around 2008 the link between base rates and RPI/CPI was broken and rates plummeted which hasn't helped cash savers at all.

http://3.bp.blogspot.com/-8U3p91Pd3Q0/Tp5yZ4sbUgI/AAAAAAAACxE/ZMj0QWe7shg/s1600/Inflation%2Bvs%2Bbase%2Brate.jpg

http://www.economicshelp.org/wp-content/uploads/2014/10/saving-rates-inflation-since-05-600x415.png

http://www.economicshelp.org/wp-content/uploads/2014/10/saving-rates-base-fixed-instant-600x447.png

Not that many years ago equity investment in funds came with a set up charge of around 5% and an annual management fee of 1.5% plus VAT.

Today as we can see from the posts on here the fees can easily be less than 1% a year so that's a massive improvement.

The FTSE 100 has been used in the survey and although its not the best it has matched the performance of the MSCI World Index from January 1995 to present.

https://www.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NUKX,NASX

Over the 21 years quoted cash savers have struggled not only in a low inflation environment but the link that acted as a cushion was broken in 2008 to present.

Another thing I'd like to add is investing 100% equity is considered high risk so how did multi asset funds perform during the same period ?0 -

The FTSE 100 has been used in the survey and although its not the best it has matched the performance of the MSCI World Index from January 1995 to present.

https://www.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NUKX,NASX

I'm not about the data from the link you've given.

In last 10 years it's been 110% for MSCI World vs 55% for FTSE100. That doesn't look like matching. Since launch 7296% vs 1231%Remember the saying: if it looks too good to be true it almost certainly is.0 -

I'm not about the data from the link you've given.

In last 10 years it's been 110% for MSCI World vs 55% for FTSE100. That doesn't look like matching. Since launch 7296% vs 1231%

There's no doubt the Ftse 100 has been poor over the last 10 years due to the heavyweights in the index and investors wouldn't be advised to use it on its own.

MSCI World was launched in 1969 and the FTSE 1985 so theres bound to be a massive difference since launch.

Using the same link the since launch returns are MSCI 9.7% and FTSE 8.9%.

I've managed to get the link back to 1992 and again the three indices are close.

From Jan 1986 to 2016 the cumulative performance is showing FTSE 1200% and MSCI 1000% and I would imagine this is down to the magic of dividends as the FTSE tends to pay above 3%.

https://www.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NUKX,NASX

Looking again at the BOE base rates for the previous 20 years 1975 to 1995 most are in double figures.

As a young lad my first share purchase was the BT floatation so I've experienced the turmoil of the markets over the years.

http://www.bankofengland.co.uk/boeapps/iadb/Repo.asp0

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards