We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Money Left After bills - *New thread*

Edenrose1

Posts: 13 Forumite

Hello All,

I could see old threads on this subject, but nothing new... I am keen to know what people / families manage on after bills, mortgage and essential items.

We have a fairly good income / bills ratio. Just bought a new house - on paper we will be £200 a month better off...as we cleared unsecured credit cards and the childcare costs will end. However I do worry that we are stretching ourselves a bit... took a 5 year fixed, on a slightly higher rate, and less term...yikes... we will be mortgage free by 58 years old...

After all essential bills and mortgage, school dinners (Not including travel and food ) we are left with approx £2,500 to 2,900 (depending if my husbands does overtime)

Out of this we buy food, travel to work...I believe our shopping bills are approx. £750 a month (this includes clothes), fuel is approx. £600 a month as we both commute... so on paper we are left with £1,150 for 'fun money'...which we should be saving, but it soon goes...

On top of this I get a bonus each year of £3000 *(after tax). This is used for a holiday...

Running 2 cars and commuting seems very costly... we probably save approx. £400 a month give or take...however keen to hear from other families ... sometimes I worry that we have stretched ourselves by taking on this mortgage...even though each month we are £200 better off ..

We are a family of 4 (2 adults and 1 teenager and 1 toddler)

Just out of interest - how do other families make it work and what does your household budget look like....

Thanks

I could see old threads on this subject, but nothing new... I am keen to know what people / families manage on after bills, mortgage and essential items.

We have a fairly good income / bills ratio. Just bought a new house - on paper we will be £200 a month better off...as we cleared unsecured credit cards and the childcare costs will end. However I do worry that we are stretching ourselves a bit... took a 5 year fixed, on a slightly higher rate, and less term...yikes... we will be mortgage free by 58 years old...

After all essential bills and mortgage, school dinners (Not including travel and food ) we are left with approx £2,500 to 2,900 (depending if my husbands does overtime)

Out of this we buy food, travel to work...I believe our shopping bills are approx. £750 a month (this includes clothes), fuel is approx. £600 a month as we both commute... so on paper we are left with £1,150 for 'fun money'...which we should be saving, but it soon goes...

On top of this I get a bonus each year of £3000 *(after tax). This is used for a holiday...

Running 2 cars and commuting seems very costly... we probably save approx. £400 a month give or take...however keen to hear from other families ... sometimes I worry that we have stretched ourselves by taking on this mortgage...even though each month we are £200 better off ..

We are a family of 4 (2 adults and 1 teenager and 1 toddler)

Just out of interest - how do other families make it work and what does your household budget look like....

Thanks

0

Comments

-

Look at how much money I've got.0

-

In general, I'm not sure how helpful knowing what other people's budget is as there's so many variables.

I'd say £750 per month on food for your family is pretty high.

Out of this we buy food, travel to work...I believe our shopping bills are approx. £750 a month (this includes clothes), fuel is approx. £600 a month as we both commute... so on paper we are left with £1,150 for 'fun money'...which we should be saving, but it soon goes...

Thanks

Have you ever watched Eat Well for Less?

If you have over £1k for 'fun money' but don't appear to know where it goes, I'd say this is the first thing you need to get a handle on? (if you really want to, that is).0 -

£1,150 a month 'fun money' doesn't sound remotely 'stretched' to me.

Have you included things such as pension contributions and savings in your 'essential bills'? If not, I'd suggest doing so.

If you think of the surplus as fun money' it's easy to fritter it away, if you make a commitment to save and set it up to go out automatically like any other bill, it's harder for it to 'just go'All posts are my personal opinion, not formal advice Always get proper, professional advice (particularly about anything legal!)0 -

What are you doing with your spare £200 a month if you're feeling that yiu might have overstretched yourself with the mortgage.

Should you be using some of it to create a untouchable emergency fund, or indeed using some of it to reduce your mortgage every month?

Life has a ha it do throwing the unexpected at us when we are least prepared for it so having that money out aside or being used to reduce your o going mortgage debt isat least making some provision for the future.

But set up a monthly standing order for that purposes. Spare cash has a nasty habit of disappearing without being accounted for0 -

You need to start doing proper budgets, that's a plan of where you want your money to go.

Then track where it really goes and iterate till you get it right.

You don't know where £15k+ a years is going finding out would be a good start.

Once you know that you can plan better.0 -

Hello All,

I could see old threads on this subject, but nothing new... I am keen to know what people / families manage on after bills, mortgage and essential items.

We have a fairly good income / bills ratio. Just bought a new house - on paper we will be £200 a month better off...as we cleared unsecured credit cards and the childcare costs will end. However I do worry that we are stretching ourselves a bit... took a 5 year fixed, on a slightly higher rate, and less term...yikes... we will be mortgage free by 58 years old...

After all essential bills and mortgage, school dinners (Not including travel and food ) we are left with approx £2,500 to 2,900 (depending if my husbands does overtime)

Out of this we buy food, travel to work...I believe our shopping bills are approx. £750 a month (this includes clothes), fuel is approx. £600 a month as we both commute... so on paper we are left with £1,150 for 'fun money'...which we should be saving, but it soon goes...

On top of this I get a bonus each year of £3000 *(after tax). This is used for a holiday...

Running 2 cars and commuting seems very costly... we probably save approx. £400 a month give or take...however keen to hear from other families ... sometimes I worry that we have stretched ourselves by taking on this mortgage...even though each month we are £200 better off ..

We are a family of 4 (2 adults and 1 teenager and 1 toddler)

Just out of interest - how do other families make it work and what does your household budget look like....

Thanks

Like others have said you need to do a proper budget and work out exactly how much you are spending each month and where it is going so you know exactly how much you have left.

Do you put away an amount each month to cover car and house maintenance and the eventual replacement repairs of items in your house such as TV, washing machine etc?.

You need to make sure you have this money saved each month before it's considered "fun money".0 -

If you've got £1150 'spare' money each month, I suspect you are in a significantly better position than lots of other people.0

-

Do a £ by £ diary for a month - record every single thing you buy- every cup of coffee, every newspaper, every £ you put in a charity box, your teenagers pocket money

Go through all the annual bills - the car tax, insurance, holiday money and all those that come at varying times - the council tax, water rates, school bits and bobs

EverythingNever pay on an estimated bill. Always read and understand your bill0 -

After all essential bills and mortgage, school dinners (Not including travel and food ) we are left with approx £2,500 to 2,900 (depending if my husbands does overtime)

Your "left over" money is slightly more than our joint income before we've even paid anything.

As others have said, do a proper monthly budget, on a spreadsheet. Add in each and every purchase (even if it's just a coffee in the morning from Pret) - you may be surprised at where you're leaking money. Check all your direct debits and give them a spring clean. Switch supermarkets - Aldi is excellent.0 -

If you've got £1150 'spare' money each month, I suspect you are in a significantly better position than lots of other people.

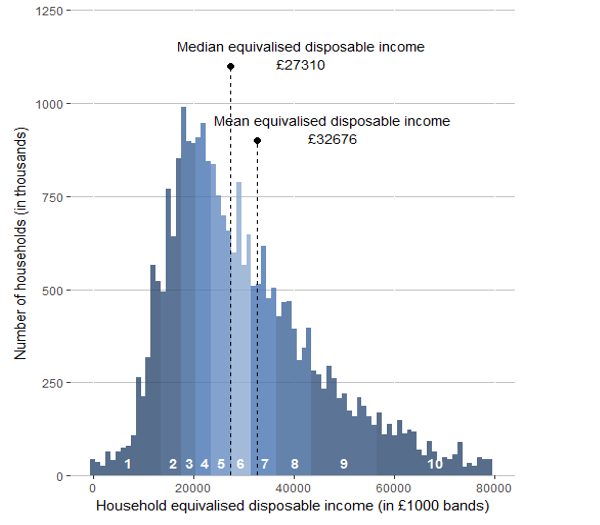

Significantly better than the vast majority I would say. Based on what the OP has said I'd be surprised if

they're not in the top 10% of household incomes:

https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/householddisposableincomeandinequality/financialyearending20170

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards