We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

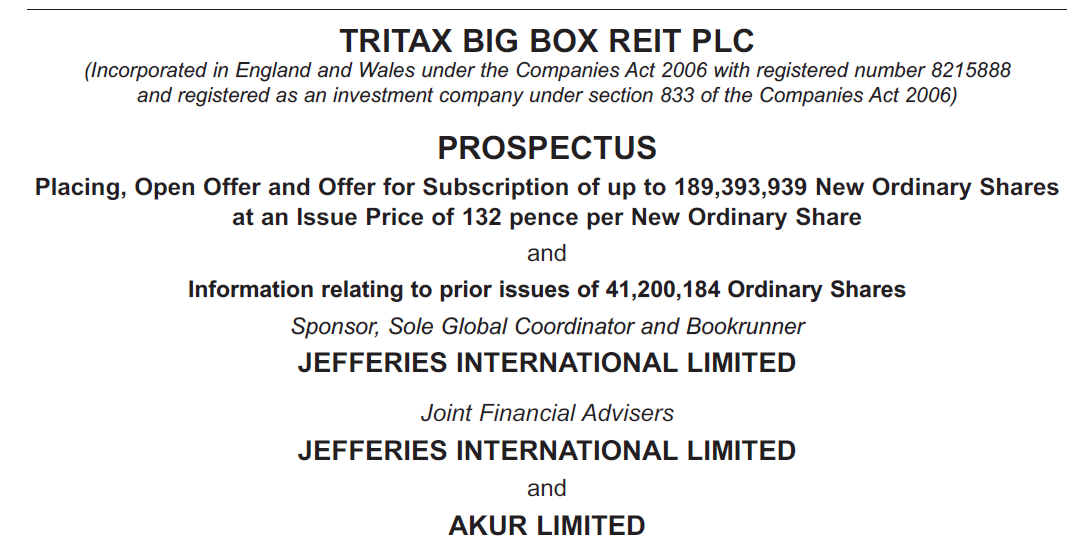

Tritax Big Box IPO

bigfreddiel

Posts: 4,263 Forumite

Anyone going for this? Applications close on Wednesday 12th

The price is set st 132p

If not why not

Cheers fj

The price is set st 132p

If not why not

Cheers fj

0

Comments

-

I am not.

The fact that they invest only in a narrow segment of the property market (the "big boxes") would concern me.

Should anything happen to impact the value of these boxes (any kind of shift in the operating model of these distribution companies) it may hit all of them.

Similar eggs in similar baskets?

But could be a good investment for others?0 -

It is not an IPO, the company are placing ~190m shares to the market to raise more capital to fund acquisitions.

I am not getting involved because there isn't space to add this company to the portfolio, and I don't particularly like the company's prospects enough to invest."If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” Warren Buffett

Save £12k in 2025 - #024 £1,450 / £15,000 (9%)0 -

george4064 wrote: »It is not an IPO, the company are placing ~190m shares to the market to raise more capital to fund acquisitions.

I am not getting involved because there isn't space to add this company to the portfolio, and I don't particularly like the company's prospects enough to invest.

Hmmm, that's odd, td direct investing show it as an ipo, I think they mean it comes in under ipo t&c's.

And to respond to eggs in one basket, I only intend to buy about 5% of my portfolio value, only a few thousand pounds. If it all goes belly up in future it's no big deal. fj0 -

bigfreddiel wrote: »And to respond to eggs in one basket, I only intend to buy about 5% of my portfolio value, only a few thousand pounds.

5% of what? (e.g. total equities, UK equities, equities in individual companies)0 -

Hmmm, 5% of my portfolio of equities.

I realise it could have meant something else.

Portfolio consists of etf's, it's, individual companies, but following a 60/20/20 ratio of equities/bonds/property

IT magazine recommends taking up the offer

fj0 -

bigfreddiel wrote: »Hmmm, 5% of my portfolio of equities.

I realise it could have meant something else.

Portfolio consists of etf's, it's, individual companies, but following a 60/20/20 ratio of equities/bonds/property

in that case, 5% is a fairly bold move, i'd say. not crazy, but you must be quite keen on this investment.IT magazine recommends taking up the offer

though presumably you will also be consulting an IFA. well worth the assurance, for only 1% or 2% of your total portfolio value.0 -

You are thinking of putting 5% of your equity money into this mid sized company with a current total market cap of about £1bn on the advice of a mag? £1bn's only about 0.03% of the UK equity market, never mind the world equity market. I take it you arent a fan of trackers and passive investing! 5% is enough to reasonably cover the whole of S Korea, Singapore, Taiwan and Hong Kong (the "4 tigers").0

-

I had a few thousand pounds of Tritax and added more at their last fundraising at 124p which swiftly moved back over 130-odd. However, I reduced my holding significantly again after it fell back to the high 120s after the Brexit vote result.

Their previous results webcast had been positive and it's an interesting niche. But much of the future return was to be delivered through yield from the big boxes rather than capital growth. With the ongoing uncertainty created by the Brexit vote, and the consequential negative impact on business confidence and investment for a few years, a logistics business is significantly more likely to be impacted in a negative way than some of my other specialist funds such as the healthcare ones PHP or THRL which are less driven by consumer and business confidence. So, I throttled back my holdings in favour of some other things at home and abroad.

Having done that, I saw Big Box had advanced a bit over the couple of months that followed (reduction in UK interest rates is helpful when your shares are being bought for their yield, and you use gearing) and it was over 140p a couple of weeks ago before they announced the discounted placing. There is not the demand to confidently get the placing away at the price it had risen to, otherwise they would have gone for something higher than the 132p, but the idea that people would pay over 140p recently is positive for buying in at 132p for the long long term.

The existing shareholder offer was only made on a 1 for 11 basis but for the open offer I'll put in for an extra thousand shares. This would still leave me at a lower holding than I had pre Brexit. Fundamentally I don't like them as much as I did, but based on the yield and the fact that interest rates aren't going through the roof any time soon, they are probably more stable than piling into massively expensive defensive equities. I'm just adding as I have a bit of money spare in the SIPP and too lazy to decide where to put it right now")

As a specialist UK logistics-focused holding i wouldn't have it anywhere near as high as 5% of my investments, but it does depend whether when you say 5% of your equities you mean of all your equities and bonds and funds etc, or whether you literally mean a twentieth of just your direct equities. The latter would probably be more sensible.0 -

CREI (Custodian REIT) is another company in the same business but on a less demanding valuation than BBOX. Might be worth getting some of those instead of more BBOX.0

-

132p with market price current 134.

Not very tempting really?

David0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards