We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

When to switch a Gilt ladder from nominal to index-linked?

Comments

-

Yes, you need to look at the dirty value using a site such as https://www.dividenddata.co.uk/index-linked-gilts-prices-yields.py or

🐻 A little FIRE lights the cigar0 -

With ii, you'll also (unless things have changed recently) need to buy them by phone. But when I did this, they still charged the 'online' dealing price, since online dealing wasn't available.

0 -

is it a fixed 9 year bridge and then its done - eg to state pension? If so I think the relatively short period, the simplicity of nominal vs linkers, and a bit of managing your budget - I’d be tempted to stay nominal just for behavioural reasons mainly. I’d accept the potential of some inflation erosion (although potentially limited in that timeframe) for the ability to plan wiht nominal figures in my spreadsheet

0 -

I hold normal gilts, with a weighted return over a 10 year term of 4.5%.

Now that AJ Bell offer regular investing with no fee, I have set my SIPP to buy my ETF of choice from coupon income - I look at this as a hedge against sticky inflation and inflation spikes, although I cannot really see inflation averaging near or over 4.5% for the next 9 or 10 years. What my personal inflation rate will be is another matter.0 -

You'd need to weigh up the costs of trading your existing conventional gilts and then buying the linkers to replace them…….both in terms of what you actually paid vs what you'll actually receive from any sales, as well as the bid/offer spreads involved (plus the minor costs of the actual trades themselves)…….all in all the cost could be quite high (though I suppose that's a relative term).

Have you considered simply buying some more gilts (linkers or conventional) to cover the expected real term loss of value on your current conventional gilts?

I suppose it depends how accurately you want to track RPI (and it's replacement in 2030…ie CPIH), and how this measures against your personal inflation rate.

0 -

I have a ladder of maturities over the next ~7 years all conventional. I've also taken a punt on ~5.5% out until 2056.

I've previously held ILGs but they've matured over the past few years and I'm not rushing to replace but they are in the mix.

0 -

10 year nominal pays about 4.9%. 10 year Index Linked pays inflation plus 1.8% So your break-even is inflation of about 3.1%. If you think inflation will be 2%, maybe you choose nominal. If you think it will be 3%, then the two are about equal, and you get insurance against it being 8% for free.

1 -

Thanks but my calculation is based on from when the gilts were purchased to their redemption - and I do not think a weighted inflation will average 4.5% during that term, let alone 8.0%.

0 -

Do you remember the 1970s?

0 -

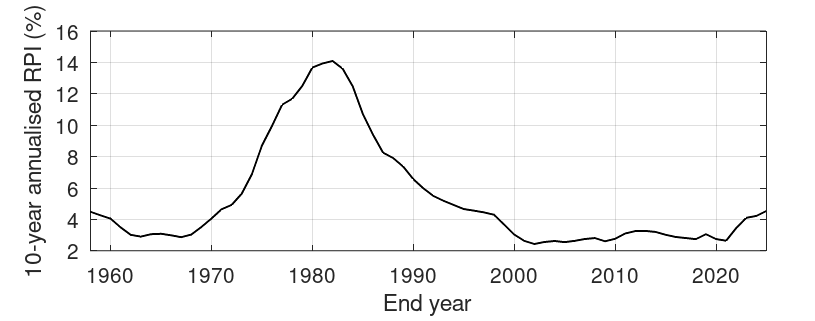

As I've said before, IMV, trying to predict future inflation is a futile exercise. However, it is instructive to look at the past. In the following graph I've plotted the annualised RPI* calculated over rolling 10 year periods since 1948 (the inflation value is plotted at the end of the 10 year period).

As @DRS1 suggests, the 1970s (and 1980s - inflation wasn't really tamed until the 90s) had very high values of inflation. Of course, for those purchasing new gilts, yields also increased over that period (e.g., 10 year yields were about 8.8% in 1970 and 14.7% in 1980 before falling to 10.9% in 1990), but those holding a 10 year gilt bought at the start of the 1970s would have seen their coupons and capital value hit hard. It is also worth noting that inflation in the last decade or two have been unusually low in a historical context since in the period after 1932 (i.e., when the UK came off the gold standard) annualised inflation has run at about 4.5%.

* Data from ONS

4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards