We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Parent Offering to clear debt.

Hello all,

As some may be aware my long term relationship is ending and I have a lot of debt. My Mum initially was going to get a regulated BTL to buy my ex out of the house so I could stay in and pay her rent. Her financial advisor put her off the idea using figures of 6.5% mortgage and that I'd pay £915 rent (which is the ballpark figure I'd be looking at privately to rent).

I've explained to my Mum and Sister the best I can about defaulting and self managing a DMP but they don't grasp that it might not be all payable, and full and finals may reduce the amount owed.

This morning Mum has texted and said she thinks paying all the debt off now to stop me digging further into debt would be the best option. My sister and sister in law are willing to be on a Joint Buyer Sole Proprietorship Mortgage and so if the debts are paid off that's an option. However it's such a huge chunk of money she's offering, and I am selling a rental house and equity in this house would mean their maybe £130,000 that my sister could get a regulated BTL. I rent off them and enter a DMP once housing situation is secured.

TLDR-: should I pay off debt or ask Mum to give to my sister as a deposit on a house that I would rent from them and default on my debts from there. I feel guilty I'm in this mess and feel a wholesale change is needed and so paying off the debts is a cop out. Is that the wrong attitude?

My sister and I went to a solicitor this week and there's a possibility of financial/domestic abuse, and misadvice about a deed of trust. But whilst that rumbles on my debt in accruing so stopping payments or paying them off (feels like wasted money if I'm cynical) is only a couple of months away now.

Comments

-

Her financial advisor put her off the idea using figures of 6.5% mortgage and that I'd pay £915 rent (which is the ballpark figure I'd be looking at privately to rent).

So you paying 915 a month rent would not cover the mortgage?

Remind us, how large are your total debts at the moment?

And how much equity is theri in the BTL in your name? is this on the market, if not, why not?1 -

£915 would be the cost of the repayment mortgage payments. Mum was hoping that it would be in the region of £600 leaving me with £3-400 to throw at the debt. My sister spoke to her and Mum thought what's the point if he'll have no money to throw at debts. This was without her fully understanding the DMP process and assuming the debts would still be in good standing.

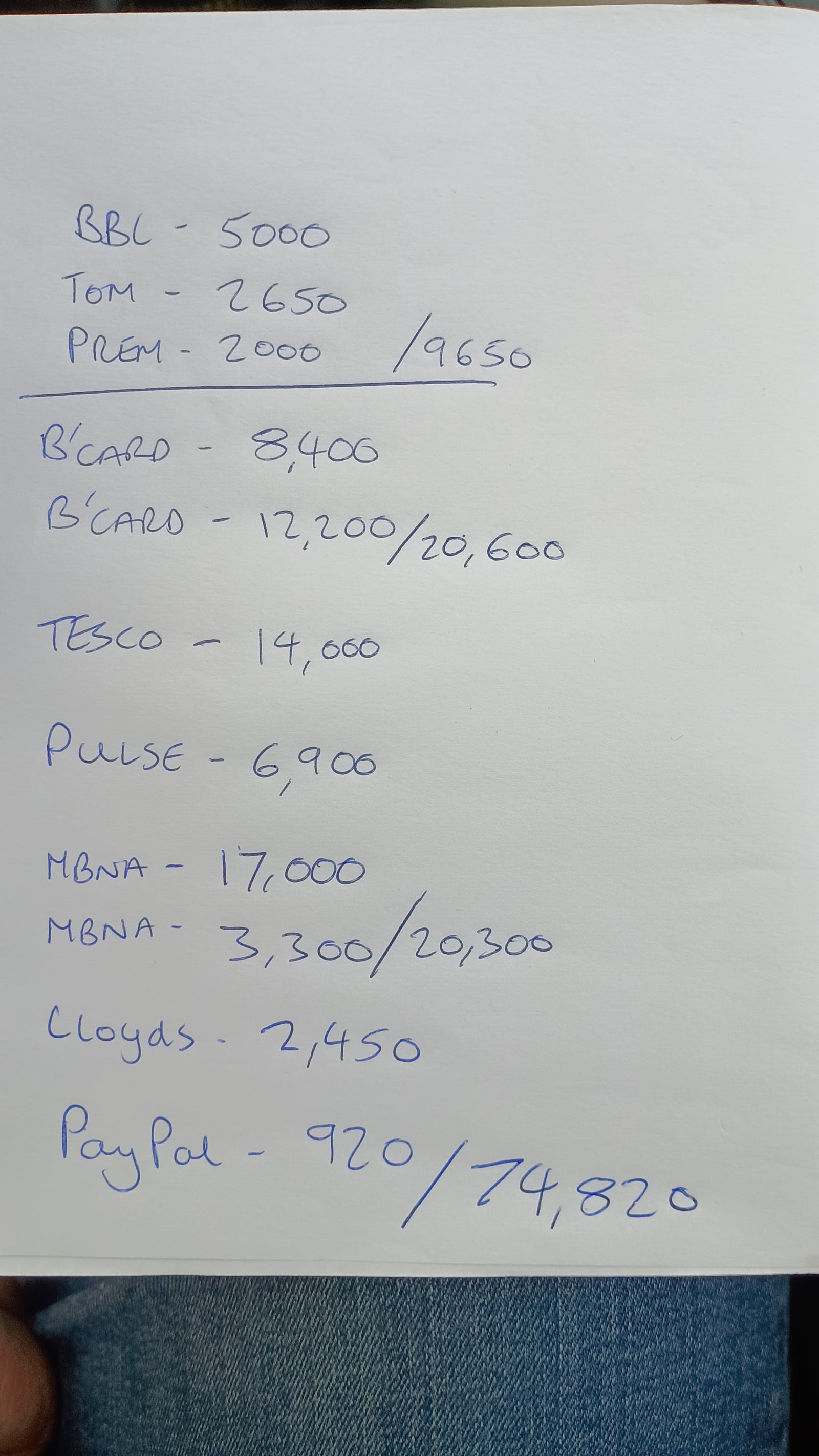

I've just totted up balances currently whilst sat in Aldi carpark. Worse than my credit report shows as the bounce back loan and business overdraft don't show on consumer credit reports. £75k debts.

My mortgage broker and my sister have both said sell rental. Mum says shame to dispose of an appreciating asset (she has 5+ rentals so in better position to cover tax etc than my sole property now)

I know I need to sell just worried how the tenant will react. I will offer her a Gifted Deposit of 5-10% so no deposit needed. Valuation maybe £110k so offer her £99k. That would be £34k equity but CGT to take out maybe £4k.

0

0 -

Tom and Prem are Barclays business and personal overdraft in that order.

0 -

can you really afford to be so generous with your tenant?

Mortgage at 01.01.14 £119,481.83:eek: today £0 Emergency fund £5.5/5.5k & £200/200 cash.:jWeight 24/02/19 14st 7lb now 12st 1lb determined to stop defining myself by my mistakes. Progress not perfection.:T100%through my 1% mortgage challenge. 100% through my pb challenge. I’m not perfect but I’m good enough.0 -

I'm erring on the side that it would save on Estate Agent fees, possible few months void period whilst it's marketed, paying the mortgage and council tax and sweeten the deal if no money down for her. I'm not sure her financial situation, if I mention it to her it may even spur her to move in with her long term partner and but the property for her son in his 20s that lives with her. I'm not sure at all and too scared to ask and rock the boat. She's been in 10 years with no hassle but her rent is below market value (and even below local housing allowance by £50…)

I think 5% is the minimum gifted deposit but if she has money she could match it to increase her Loan to Value.

0 -

I rad my Mum's message (as previously my anxiety made me clam up and not read past ye 1st line on Saturday) it's as follows

Morning *****

I think 1 way I can help u feel some positivity about ur situation is to deal with ur debt.

It needs capping at whatever total it is right now, then we know what we're aiming at.

I'm proposing giving u a monthly living wage to cover what u wd normally need to spend on ur cards. Any extra u have and I have we'll use on paying off those cards.

U will then have to live within ur means, budget ting and saying NO to ***** and her extras - vet bills, etc.

So...I need u to sit down and work out ur incomings and outgoings, work out the shortfall and give me a figure that u cn live within.

I'd like to know what cards u have, how much u owe on each and what the payback date is on each so we cn closely monitor our progress.

I will eventually cover all ur debt so, by the time ur house is on the market, u'll b in a position - debt free - to get a mortgage.

I hope that's lifted ur spirits! Have a good day! :-) xx

But we'll still access the debt charity to see if the debt can b decreased. Xx

I'm sure if that proposal is even feasible as she thinks the debt could be cleared by the time our house is up for sale.

I think I need to go nuclear and default on all my debts as planned and then just rent somewhere. Save the money from house sale for full and finals in a few years.

Just at a complete loss my head's spinning and don't know where I'll be living or affording to live with my 3 boys when it's my turn to have them.

0 -

you assume that you won’t be the parent with care. Why is this?

Mortgage at 01.01.14 £119,481.83:eek: today £0 Emergency fund £5.5/5.5k & £200/200 cash.:jWeight 24/02/19 14st 7lb now 12st 1lb determined to stop defining myself by my mistakes. Progress not perfection.:T100%through my 1% mortgage challenge. 100% through my pb challenge. I’m not perfect but I’m good enough.0 -

I'm still unsure of all the permutations. The solicitor we saw said as far as practicable a court would aim for shared care unless one parent has to move out of the area for housing reasons.

That's what I'm aiming for shared parental responsibility as that's what they're used to. Where I'm unsure her plans is the fact my ex poo-pooed when I suggested 50/50 nights or at least 150+ and she said that I need to be working all hours humanly possible when we separate. I assume it's for CMS and other entitlements. The solicitor mentioned mediation if we need help formulating a parenting plan.

She will have to go up to full time hours and I'm flexible for any dentists/doctors/appointments etc as working locally for myself.

0 -

You need to be thinking about yourself & not what your ex wants which is to benefit her.

I am a Forum Ambassador and I support the Forum Team on Mortgage Free Wannabe & Local Money Saving Scotland & Disability Money Matters. If you need any help on those boards, do let me know.Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button , or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.

Lou~ Debt free Wanabe No 55 DF 03/14.**Credit card debt free 30/06/10~** MFW. Finally mortgage free O2/ 2021****

"A large income is the best recipe for happiness I ever heard of" Jane Austen in Mansfield Park.

***Fall down seven times,stand up eight*** in ~~Japanese proverb. ***Keep plodding*** Out of debt, out of danger.

One debt remaining. Home improvement loan. 19months left.1 -

Yes that whole mindset shift will take some work after 19 years together. Just don't want to "pole the bear" so to speak and make her limit access to boys or anything.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards