We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Early Retirement Refused

I’m 55 and I have a deferred DB pension with Diageo, I started in 1999 and left in 2001. I had transferred in my previous DB pension from IMI who I worked for from1988 to 1999.

I recently asked for a benefit statement and they mistakenly thought I had asked for early retirement (no plans to retire until aged 60). They sent me a letter saying:-

Unfortunately you are not able to take early retirement at this time, as your early retirement pension would not be high enough to cover your Guaranteed Minimum Pension.

GMP is accrued due to you having been contracted out of the State Second Pension (at the time called the State Earnings Related Pension Scheme). Your contracted out status means that you paid lower national insurance contributions and as a result accrued GMP under the Scheme in place of any additional state benefit. GMP has its own rules regarding how it is to be treated and this must be the minimum amount of pension paid to you by the Scheme when you reach your 65th birthday.

When you retire from the Scheme before your normal retirement date, your 65th birthday, an actuarial reduction must be applied to take into consideration the additional time your benefit will be in payment. As a large proportion of your benefits are related to your GMP entitlement, any reduction that would have to be applied to it due to early retirement will mean your GMP would not be covered at your 65th birthday. Therefore early retirement will not be available to you at this time.

I asked for my GMP at date of leaving and got this:-

I can confirm that your benefits at your Date of Leaving (DOL) 03/08/2001 were split as below:

Benefits derived for GMP: £457.08 per annum

Benefits in excess of GMP: £2,959.71 per annum

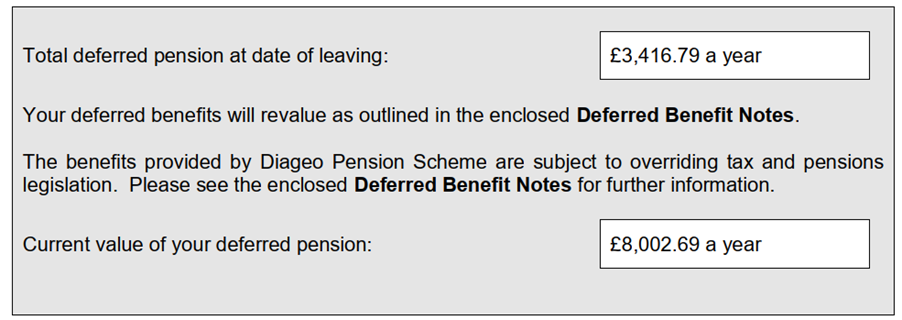

Total: £3,416.79 per annum

They sent me this current benefit statement

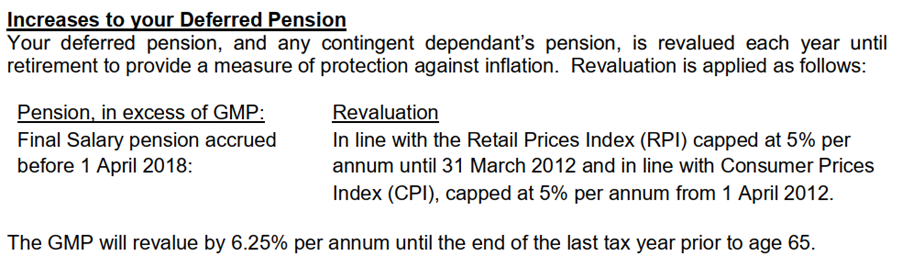

Using the GMP revalue rate of 6.25% I have calculated that the GMP will be approximately £3,590.68 at NRD So why couldn’t I take early retirement now if I wanted to as I would be receiving more than that amount?

Any advice welcome.

Comments

-

Do you know how much they would reduce your pension if you took it early? Your post is very long but I couldn't spot that information anywhere. It would have to be reduced a lot if you took it 10 years early and so it might not then cover the GMP, which is why they would refuse to allow you to do it.

1 -

Their early retirement factors were equally as wooley in the scheme rules:

The reduction will be on a basis agreed by the trustee and the company after considering advice from an Actuary.

My illustration for retiring aged 55 shows a pension of £7703 which is greater than my GMP at 65

0 -

That figure of £7703 is hardly less than the deferred pension. A quick google of early retirement factors suggests that maybe 5% for each year early is common, but each scheme will be different and the numbers will change over time due to changes in interest rates and life expectancy, which is why they don't set them in stone. The only way to find out is to ask them. Also make sure you understand what increases you will get on the two different parts of the pension after they come into payment and whether there is a lump sum to take into consideration.

1 -

See

https://forums.moneysavingexpert.com/discussion/comment/18024759/#Comment_18024759

2 -

Thanks xylophone.

What I don't get is the GMP element of my pension at leaving date was approx 14% of the Total value at £457.08. Revaluing this forward to 65 gives it a value of approx £3600. If my current pension value is £8000 then allowing for a 5% reduction for 10 years would mean I'd be getting £4000 now before any index linking up to 65, which is more than the GMP at 65.

0 -

You will need to request a fuller explanation from the administrator (although if you do not intend to claim the pension until normal scheme retirement age, you may feel that this would not be worthwhile).

It occurs to me that factors not so far considered are those relating to how a pension in payment increases pre and post GMP age and what might be the situation with regard to your total pension at GMP age.

If the pension were taken ten years early, would the starting amount amount be the total of GMP revalued to date and excess revalued to date less the actuarial reduction?

Would escalation in payment be as detailed here up to GMP age?

In the background the GMP element would have to be revaluing by 6.25 % up to GMP age - how much of your pension would be GMP at that age?

The actuarial reduction has been mentioned but not how much this might be. One poster who was allowed early retirement nine years early from a DB scheme mentioned 35%+.

https://forums.moneysavingexpert.com/discussion/comment/81680163/#Comment_81680163

1 -

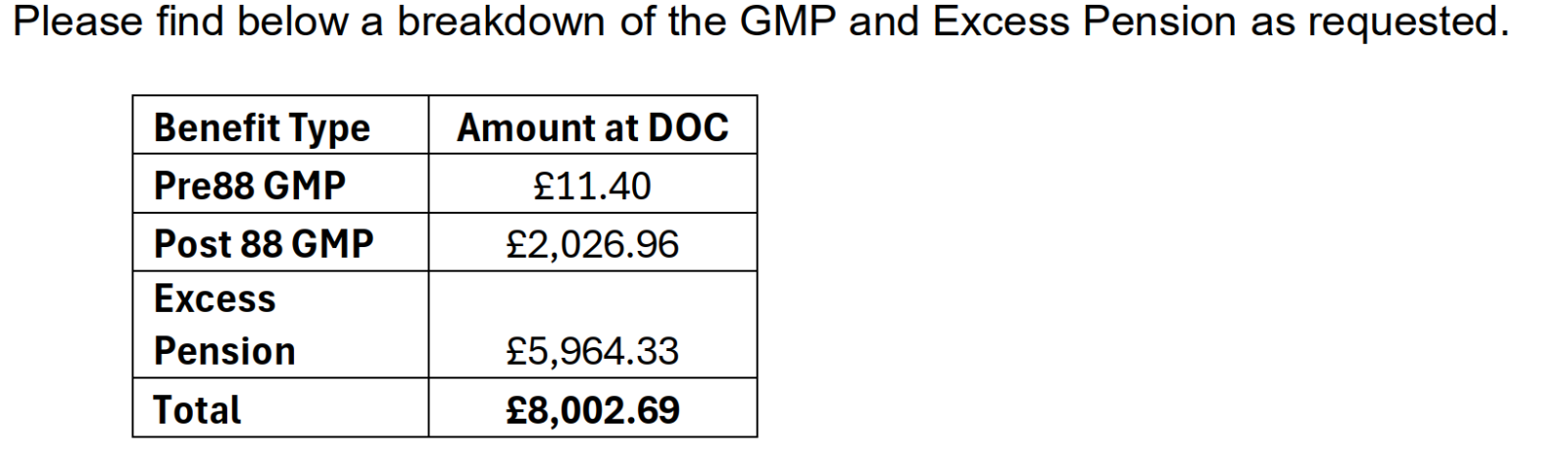

I have just received this after asking for my GMP/Excess split as of this month:-

0

0 -

One other point to consider is that it's not the total pension which has to be at least equal to the GMP at age 65, it's the element in respect of service prior to 6 April 1997. The figures above don't give a split of the non-GMP Pre/Post 97, and the fact that all of the Pre97 element comes from a transfer-in in your case makes it difficult to guess what the split would be on the info we have, but you'll have less headroom than you think.

In addition, a mistake I have seen administrators make before is to say "we received your transfer-in after 1997, we're giving it the pension increase that applied to pension currently accruing when we received it [fine so far], so we'll treat it all as Post97 [less fine]". If that were the case they might think you had no Pre97 non-GMP pension, in which case they wouldn't let you retire until age 65. Hopefully they're not making this mistake, but it may be worth checking how they're splitting your excess pension Pre/Post97.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards