We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Advice please

Evening all,

In July 2026 our 7 year fixed rate mortgage finishes (Interest rate 2.43%!), that leaves us with 2 years left of our 25 year mortgage and a balance of around £15,000.

So my question is:

do we take out a 2 year mortgage to finish (probably not)

OR

pay it off with a stocks and shares ISA - we have 2 around £24,000 (decreasing rapidly at present!)

OR

we've amalgamated some pension pots that we've accumulated over the years, we're going to take out the 25% tax free lump sum (which we were going to use for some nice holidays over the next few years) but could use this to pay off the mortgage.

I'm 58 my husband is 62 - we're fit and well and are both self - employed and work not part time but probably not full time either. We both have good on-going pensions.

Many thanks.

Comments

-

It is very chaotic time due to wars etc. so markets and interest rates behave irrational too.

Nobody knows what's best, you should know closer to July really.

In the meantime check of you can actually get a 2 year fixed mortgage as sometimes your two years could be 23 months etc.

But also as it's just £15k you may as well pull some money from ISA and call it a day and have less stress in the future - and then continue rebuilding the savings instead of paying mortgage.

1 -

First question is what are they offering you after you fixed rate ends? If they aren’t offering anything, what is their SVR? Then see if you would prefer to pay that rather than surrender pensions etc

Just a thought, at that level you could probably play around with interest free periods on credit card loans.

I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.3 -

Why is the ISA decreasing rapidly?

The best approach is what suits your spending habits and whether you could get yourself into a worse situation financially.

I do like @silvercar 's suggestion about an interest free credit card, you might not get the full 15k, but possibly 10k and pay off the 5k (full amount paid within the interest free period, otherwise the interest rate is often too high). But it all falls down to how disciplined you are not to make things worse. Otherwise, I'd pay it off from whichever pot not generating a return on investment.

I'm FTB, not an expert, all my comments are from personal experience and not a professional advice.Mortgage debt start date = 11/2024 = 175k (5.19% interest rate, 20 year term)- Q4/2024 = 139.3k (5.19% -> 4.94%)

- **/2025 = 44k (4.94% -> 3.94%)

- Q1/2026 = PAID (3.94%)

1 -

Trump said the war will be over in 2 weeks and oil prices went down, share prices went up (2%).

I know trump says a lot so who knows how true it is.

IF the war does end in 2 weeks, then you might find your ISA shoots back up again and that might alter your decision. I know its only 2-3 months off, but you might find your plans change because of one person.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

Trump isn't the sole person who'll decide when it's over - the Iranians and the Israelis also need to agree to stop shooting.

0 -

Either way, in July when OP mortgage renews will know much more - so for now probably stay put, and review things in June.

0 -

pay it off with a stocks and shares ISA - we have 2 around £24,000 (decreasing rapidly at present!)

There isnt much that is decreasing rapidly at present. The short term loss is mild and its not a daily drop but a volatile slope. The last few days of gains are yet to appear on values due to lag (US for example is a day behind).

we've amalgamated some pension pots that we've accumulated over the years, we're going to take out the 25% tax free lump sum (which we were going to use for some nice holidays over the next few years) but could use this to pay off the mortgage.

Is robbing your retirement years to pay for things in your working years a sensible thing to do?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

The impact on a £15K balance is pretty marginal anyway.

The narrative around this non war 'war' is pretty odd, I guess it's the sign of the times. There will always be instability of some sort, terrorist threats, terrorist action etc. If global markets couldn't anticipate what has happened, we have no chance!

If it was me I would secure the lowest cost option that can be achieved (with existing lender), which shouldn't be high. It will just be higher than the abnormally low rate you have been enjoying for so long.

0 -

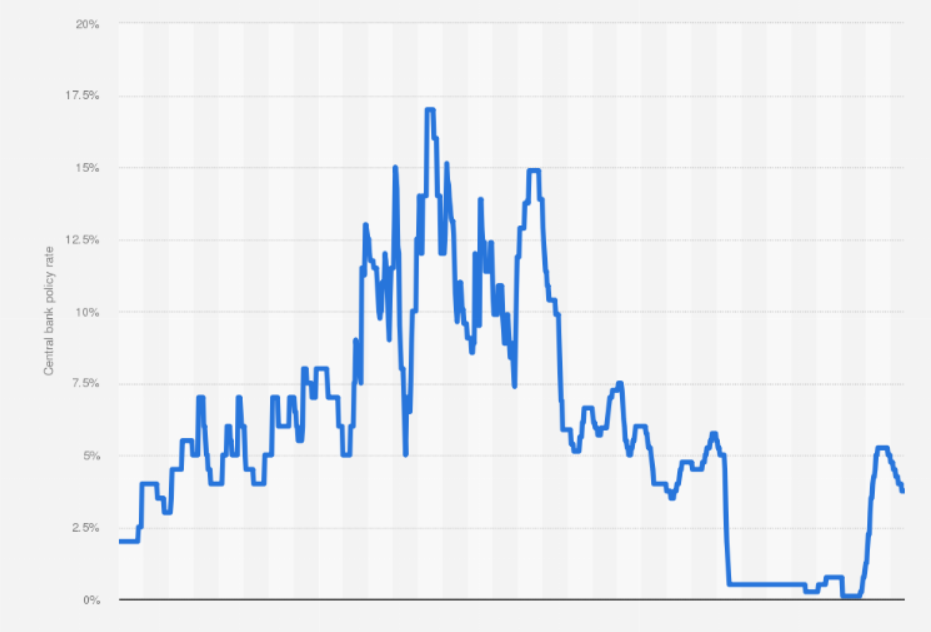

Some perspective, this is the bank rate history for the last 75 years

0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards