We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Advice with regards mortgage renewal

Comments

-

2022 was more about the unwinding of QE, and ending of lockdowns [massive pent up demand along with saved up resources] than what was happening in Ukraine.

Of course those events coincided, but people still seem to think 1% mortgage rates are the norm ! And it was politically convenient to blame what happened on other events that coincided with the rapid normalising of interest rates (aka cost of living crisis).

There is no genuine prospect of returning to massive QE, as the US and other western countries are leveraged to their eyeballs.

The economist is correct in that it is different to 2022. But to the extent that this is just a typical geopolitical event, and there is no global pandemic or once in a century type of unwinding of extended huge fiat money printing.

We need to make our own judgement calls obviously, personally I see nothing that would cause the US to massively hike base rates from what they are now. Of course, there could always be a significant event that we know is possible, but not obviously on the cards (nuke dropped, credit crisis II, China invades Taiwan et al).

0 -

Not a chance we'll go back to below 3% interest rates for a considerable period.

Option 1 or 2 is by far your Option

0 -

Thanks for all the comments. Job security wise, I work in public sector which was always “safe” but with recent government changes and cuts who knows what the future holds with our jobs anymore.

With regards the mortgage, when it comes to renew its balance will be around £190k. We are looking to lump sum pay around £20k off it plus we can do some extra bits each month (smaller amounts).

My concern with all the talk at the moment is that the last time the world had similar issues with oil supplies mortgage interest rates where into double digits.From what I understand mortgage rates while related to BoE rates also cha he themselves based on the swap rates between lenders?

1 -

Mortgage rates never hit double digits? (I have been a broker for 15 years and have only done one mortgage at 10% and that was back in maybe 2013-14).

There was the odd lender who operates in the real heavy adverse (together money for example) who have rates at double digits, but their rates were 7-8% when the high street was 1-2%.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

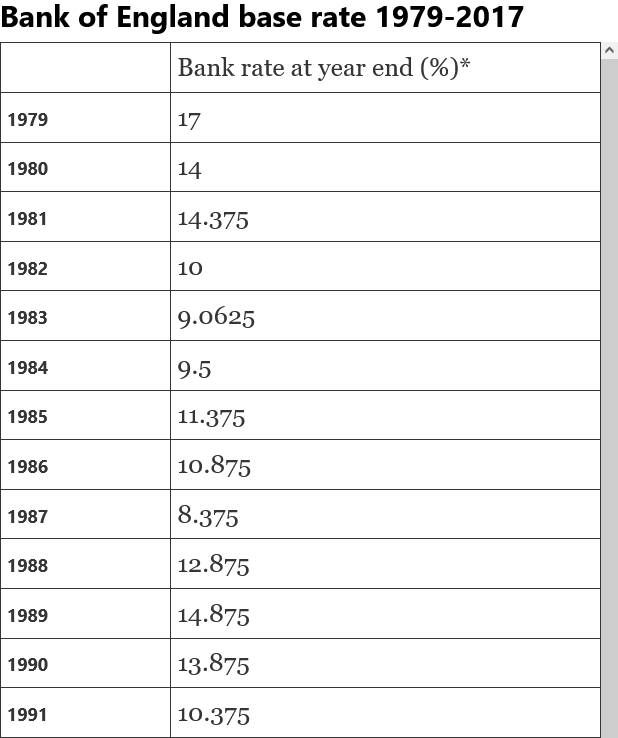

The late 70's to 80's were an interesting time to be getting into the mortgage market…

… thankfully not been that bad since.

0 -

@MWT and @garyh_uk I didnt mean they have NEVER hit double digits.

I meant they never hit them during the russia/ukraine war…

My response was to this:

My concern with all the talk at the moment is that the last time the world had similar issues with oil supplies mortgage interest rates where into double digits.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

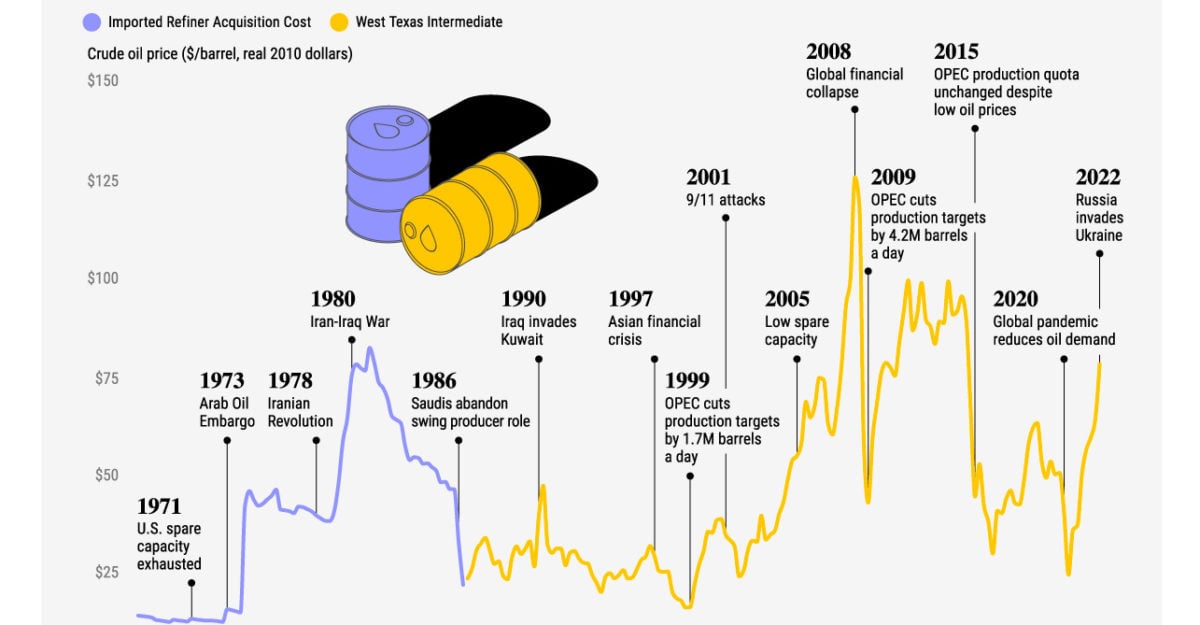

As per my earlier post, it's not the oil price fluctuation in isolation that is a trigger for higher interest rates. For example the GFC created manufactured unusually low interest rates due to QE.

This chart is a decent representation. The oil price will always be volatile.

0

0 -

I said it comes down to judgement earlier, and in my judgement the 'world' has irrevocably changed, primarily due to t'internet and social media. Western populations simply won't tolerate high interest rates, even if economically they are the right thing to do. In my view we have already witnessed this in the demand led double digit inflation, post QE and lockdown.

If you have the means, there is also the hedging option of retaining capital in cash/MM.

0 -

In 2023 I hated my job. Every call was a bad one, people I have known for years worried about their mortgage, their home etc. Thankfully we found options for all of them, but a lot of it involved extending terms.

I genuinely think the 4.5x income multiple that came in after 2008 helped a lot of people during that period. But the govt/FCA in their wisdom have decided to water that down and its not possible to get 7x income with a 3% deposit! Mental!

BUT what I did notice was that within about 12 months, the conversations had changed. People had stopped complaining about the higher rates and had got used to them.

Dont underestimate people. We are generally quite resilient and will change with the situation around us.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards