We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Capital Gains & the annual exempt allowance

I know there are lots of threads about this already, but most get bogged down with incorrect opinions or misunderstandings. So, I thought it might be useful to attempt another one.

Any single personal possession (ie. not something you purchased with the intention to sell on) that you sell for less than £6000 does not attract capital gains tax.

There is an Annual Exempt Allowance of £3000 that covers the sale of personal possessions.

This, it seems, is where there is confusion. Some interpret that to mean that if, for example, someone sells 10 items, all for under £6000 each but the total profit is more than £3000 in a single year, they have to declare that amount. The other interpretation is that it's only the amounts from items that sold for over £6000 each that are added up & the first £3000 is exempt.

Reading official guidance can be read in ways that supports both interpretations. So, if there are an tax experts reading this perhaps we can get a definitive one.

Comments

-

The £3,000 Annual Exempt Amount is not a special allowance for personal possessions. It applies to your total chargeable gains for the tax year. Personal possessions, or chattels, have a separate rule: if an individual item is sold for £6,000 or less, any gain on that item is normally exempt. So selling ten separate items for under £6,000 each does not usually create a CGT bill just because the total profit exceeds £3,000. The main caveat is where the items form a set, because HMRC can then treat the set as one asset for the £6,000 threshold purposes. Example to clarify:

You decide to sell your collection of 10 old cameras over the year. Each one sells for £2,000 and cost you £1,000, so £1,000 gain each, £10,000 total.

Because each item sold for under £6,000, they are treated as exempt chattels. Those gains are ignored for CGT, so the £3,000 Annual Exempt Amount is not even needed.

Contrast that with one camera sold for £7,000 with a £3,000 gain. That gain is chargeable, and you would then use your £3,000 Annual Exempt Amount against it, leaving nothing to pay.

NB the £1,000 trading allowance for income tax is only applicable if HMRC considered you to have been trading, e.g. buying cameras to resell for profit. Simply selling your own used gear doesn’t usually trigger that.

2 -

Im not an expert, but to me it's pretty clear:

You only need to calculate gains on personal possessions you sell if they are worth more than £6,000 (with some exceptions, e.g. cars)

You only pay CGT if your gains in a tax year exceed your £3,000 personal allowance.

So in your post above, its the second scenario that is correct. You can sell as many items as you want below £6k and you won't attract cgt.

0 -

Yep, exactly this.

For the example of a set, imagine you have a tea set of 10 cups, each worth £1000, bought for £100 each.

If you sell the set for £10k, you've made £9k profit and as the set is worth more than £6k you would incur cgt liabilities.

You cant avoid this by selling each cup separately, or splitting the set into parts less than £3k each. For cgt purposes hmrc treat it as one item.

0 -

Thanks for the replies, though I would say they do include comments that are one reason for confusion, such as;

"The £3,000 Annual Exempt Amount is not a special allowance for personal possessions. It applies to your total chargeable gains for the tax year. Personal possessions, or chattels, have a separate rule".

&

"You only pay CGT if your gains in a tax year exceed your £3,000 personal allowance."

The rules do not make it clear that personal possessions (under the £6000 single item limit & not part of a set) are outside of chargeable gains.0 -

I've not seen this gov.uk page before, but it opens up a lot of questions:

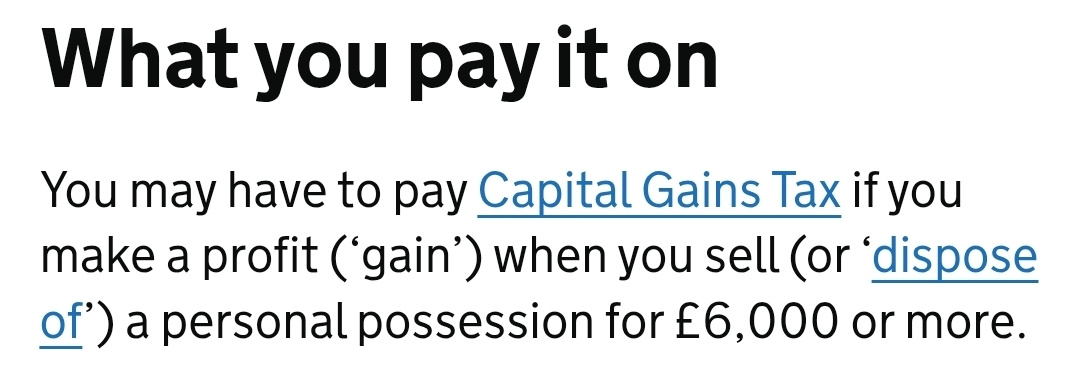

Regarding the page for personal possessions, the wording is certainly "succinct", but the sentence:"You may have to pay Capital Gains Tax if you make a profit (‘gain’) when you sell (or ‘dispose of’) a personal possession for £6,000 or more"

…..certainly implies that you do not need to consider any personal item sold for £6000 or less.The working on the next page for larger sales also supports this:

You may be able to reduce your gain if you got between £6,000 and £15,000 for your possession when you sold or disposed of it.- Subtract £6,000 from the amount you’ve received.

- Multiply this by 1.667.

- Compare this with the actual gain - use the lower amount as your capital gain.

So assuming the same rule applied for items under £6000, subtracting £6000 first and using the lower would always result in a CGT of zero.

There is also another doozy on that page:

You can claim losses for possessions sold for less than £6,000. Work out your loss by using £6,000 as the amount you sold your possession for, and report it in your tax return.

So any personal possession I own (I assume it would apply only those that would be equally eligible for a CGT Gain) which cost more than £6,000 and which I sold for less than £6,000 can be partially (or wholly) offset against any other taxable gains for the year? I knew you could offset investment losses against other investment losses, but didn't realise you could include general personal crap.Made a large gain on some shares? Sell that overpriced designer necklace you bought a decade ago for £15,000 for £6,000 and get £9,000 of offset against your gains? Nice!

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

The government website couldn't be much clearer:

0

0 -

I don't think that's clear at all as it can be read as 'the total of all items you sell where you've made more than £6000, or only on items that you sell for more than £6000 each.

It seems obvious based on the replies so far that there is still confusion.0 -

It literally says 'a personal possession', I.e. each one that is sold for over £6k.

0 -

I think your missing the point. Yes, it says that but as others have pointed out there is another section of the rules that refers to the AEA & that is where the confusion is; is it £3000 total for all items sold based on the amounts over the £6000 individual limit, or are all items under that not included at all in that £3000 calculation.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards