We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Advice on moving pension fund now due to unplanned retirement

Hello

I was hoping I could get some advice on what the best approach would be to my current situation, which is as follows…

I’m 54 and will turn 55 later this year, I hadn’t planned on retiring any time soon but some health issues have made me have to consider retiring in the next year or two.

I have a defined contribution pension at work which is currently at about 500k, it’s lost about 30k in the last few weeks due to the current uncertainty.

As I hadn’t planned on retiring anytime soon the retirement age on my pension is set as 63 and it’s currently invested in a medium to high risk fund. So due to a change in my plans because of my health and the fact I will now likely want to retire in the next year or two, do I change the retirement age on my pension now to 56/57 which I believe would trigger the pension to be invested in lower risk funds. I also have the option of manually changing to a lower risk fund.

If I do this I suppose I’m locking in those recent losses, however is it best to take that hit to lower the risk of it dropping further with these current events? Or should I leave it as it is for now and ride this out then make changes in a year or so when hopefully things have recovered? My worry is that I may have limited time to recover from what’s currently going on.

Comments

-

With a £500k pot and health issues affecting timing, this is one of those cases where proper regulated advice from an IFA may be money well spent.

3 -

What do you plan to do with your DC scheme when you retire? Are you planning to buy an annuity, or are you planning to draw down? Or some combination of the two?

For drawdown, you're going to remain invested for another 30-40 years so it might be a bit premature to de-risk now.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.2 -

As said above, it would be silly to change your investments now.

Sounds like you are in default fund, designed for anulty at set retirement age.

If it was me, once market dust settle down, I would look to move all investments from any default fund.

Unless you are day trader, ignore news about market. News stations/papers need sensational hedlines to make money.

Better spend time planning how you are going to straucture your drawdowns, to be most tax effective.2 -

I’m planning to draw down, I had considered the fact the majority of the money would stay invested so would have time to recover. So yes using that logic I guess it would have time to recover, although once I start to access the pension won’t it then be put into much safer lower risk funds so would take much longer to recover?

I didn’t realise you could have a combination of draw down and annuity? So I could use half my pot to buy an annuity and the other half as draw down to spread the risk?

0 -

Yes it’s in a default fund, I believe it automatically switches to the lower risk default funds as I get nearer to the set retirement age, that’s why I’m thinking leave the retirement age set on the pension for now as I don’t want to trigger that just yet.

I agree that it feels best to let this play out, then once things have recovered think about moving to a lower risk fund. When you say move it from a default fund, are you suggesting move it to a non default fund?

0 -

… although once I start to access the pension won’t it then be put into much safer lower risk funds so would take much longer to recover?

Only if you choose to. Msany people would leave their pension in the same funds when starting drawdown. (There's a bit more nuance about reducing sequence-of-returns risk, but this might not be the thread for that.)

I didn’t realise you could have a combination of draw down and annuity? So I could use half my pot to buy an annuity and the other half as draw down to spread the risk?

Yes, that's an option.

You might want to take Vitor's suggestion and speak to a specialist about what exactly youcan do with your pension once you retire.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1 -

Okay that’s good to know about splitting between annuity and draw down, thank you for that.

Also worth thinking about staying invested with more risk whilst drawing down, I’d been thinking just leave it in lower risk funds but makes sense in the early years whilst time to ride the markets.

And yes I do think I should get professional advice as I’m just not aware of all the various options.

0 -

You need to know what the target is for the default fund.

Traditionally these funds would be targeted at someone planning to buy an annuity, so they would derisk in the last couple of years down to cash and gilts.

Nowadays the default is more targeted at someone wanting to drawdown, although you can change it to an annuity targeted one if you like normally.. These funds do still derisk, but still keep a % of equities.

You need to check which one you are in.

You see people on this forum who stick with 100% equities right through retirement, although it is not common and you need strong nerves. Most historical analysis of drawdown, is based around approx 50% equities.

3 -

You may find this page useful

Buy an annuity for a guaranteed pension income | MoneyHelper

Buried in there somewhere is their annuity comparison tool. You could play with that to see how much you might get with an annuity - it allows you to put in details of your health conditions to see if you would qualify for an enhanced annuity.

1 -

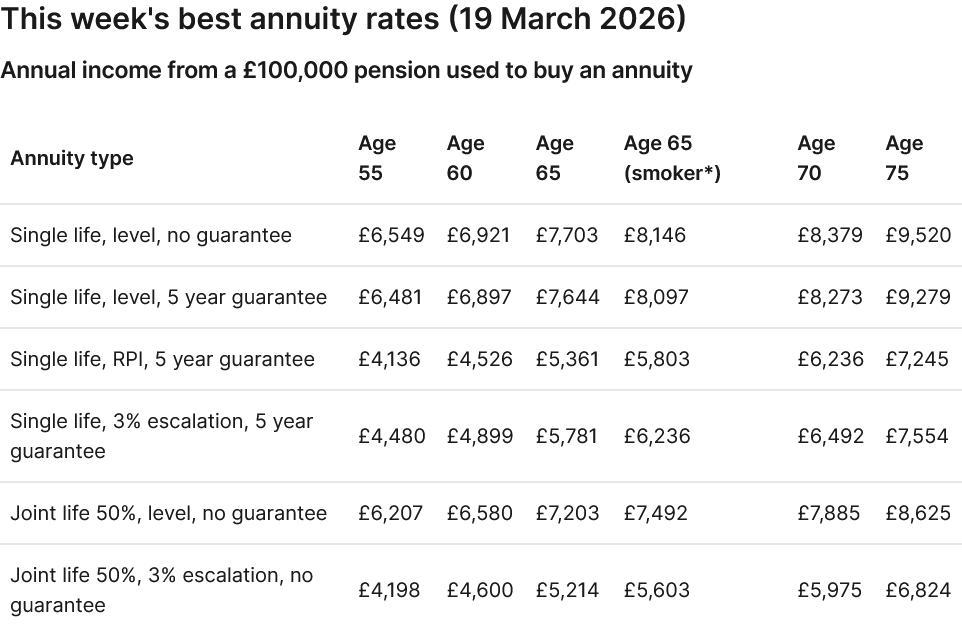

Buried in there somewhere is their annuity comparison tool.

Indicative rates at a glance for the healthy retiree from Hargreaves Lansdown's best buy table:

Latest table, for future reference:

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards