We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Small DB Pension transfer?

I'm trying to get on top of the several pensions that have built up over the years. Most are DC pots but I have a DB pension from my first job back in 1992-1996 - I was only an apprentice and left the scheme on 14k salary and it looks like my benefits are based on that final salary.

It currently has a transfer value of a smidge over 30k which I am wondering about moving into a SIPP I have - although being over 30k by a few quid looks like I need to pay for advice, which sounds costly and possibly scuppers this idea?

I ran a quote for retiring in 10 years (which is a bit early as I'll be 60 then, but the system doesn't like me asking for years after that) and it suggested it will pay out just under 2k a year, or a 9k tax free lump + 1400/year.

Is there an obvious choice here?

Comments

-

Once you have deducted the cost of the (mandatory) advice do you think you will be able to do better than the DB scheme?

Also, why would it be based on a different salary?

The amount of pension earned should increase with some form of inflation protection (this is a key thing for you to find out) but your salary won't change.

1 -

I was quoted a up front fee of £8k for an IFA to look at what he thought was a DB pension I have (it isn't, but it's complicated). That's a huge amount of money for you to lose particularly when the overall value of the pension is so small.

I'd suggest you take it as soon as you can without a reduction (age 60?), with the lump sum (pop that into one of your DCs?) and then happily have a great birthday party each year with an annual payout.

I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅1 -

It currently has a transfer value of a smidge over 30k which I am wondering about moving into a SIPP I have - although being over 30k by a few quid looks like I need to pay for advice, which sounds costly and possibly scuppers this idea?

A DB transfer value fluctuates the whole time - and not necessarily upwards. Depends on market conditions and a whole host of other factors. It could be that the value will drop below £30K and advice would no longer be mandatory. Whether transferring at all would be a good idea is, of course, another matter entirely…

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

I ran a quote for retiring in 10 years (which is a bit early as I'll be 60 then, but the system doesn't like me asking for years after that) and it suggested it will pay out just under 2k a year, or a 9k tax free lump + 1400/year.

£2k pa at age 60 for £30k could be a pretty good deal.

How is it indexed once it's in payment?

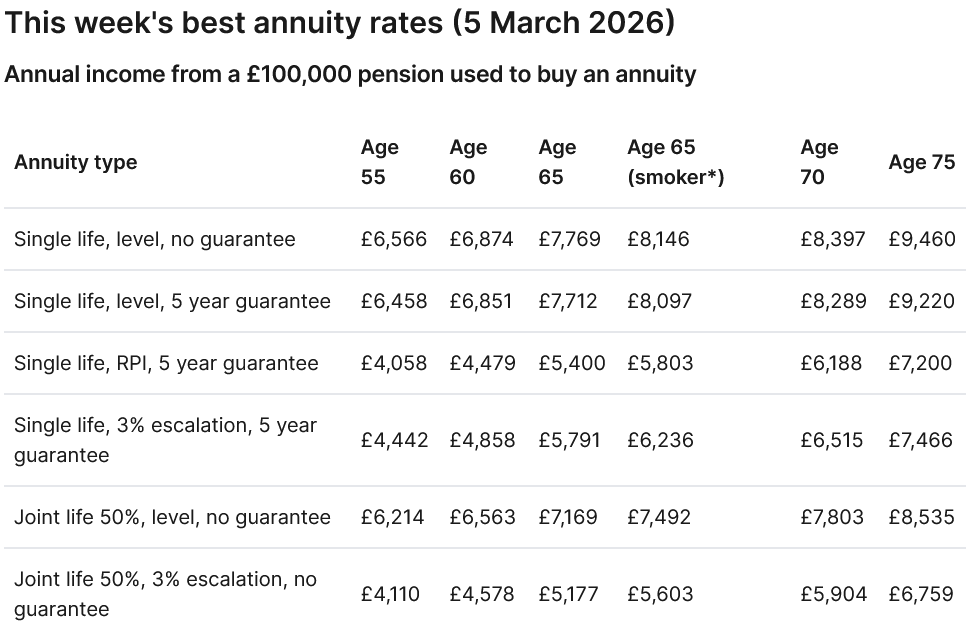

£2k pa indexed to RPI for a 60-yo would cost about £45k per the current HL best buy list.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1 -

Thanks all, I'll have a dig through the website and see what I can find out, it seems its not a clear cut "get out now" situation though. I did find the company will pay for 2 advice sessions with their IFA but only if you are within 9 months or later of becoming eligible to claim the pension - I'm a few years off that.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards