We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

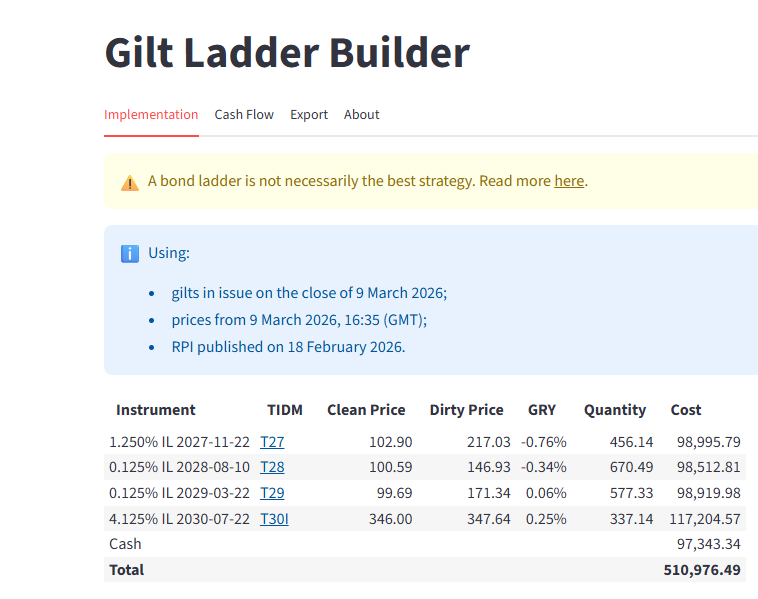

ILG ladder query

Below shows ILG ladder costs and GRY for 100K withdrawal each year for 5 years as a means of preserving wealth until SP kicks in.

I understand the assumed inflation rate is 3% - and is currently 3.2%. The first 2 gilts show a negative GRY in real terms - I assume at 3% inflation.

Q then - Assuming the above is correct, and stays that way for the foreseeable, would it be wise to purchase the first 2 gilts? If not, then what - MMF?

If I believe inflation will rise, I assume GRY will rise, and the first 2 gilts may be a considered to be a more sound purchase?

Apologies in advance - just seeking some clarity.

Comments

-

Once you buy ( say ) T27, you're locking in a real terms overall loss of 0.76%.

If inflation was to balloon to 20% between now and its maturity, you'd make a nominal return of about 19% but still be down a little in real terms.

In a MMF you might find you get 4% now, and it might rise a bit with inflation, but could potentially incur a much larger real terms loss.

1 -

Many thanks - why then would anyone buy T27 and T28 if locking in a real term loss?

0 -

It's still a known amount you will lose out on to inflation, every other option you don't know what position you will be in w.r.t inflation. It removes gambling on which way inflation will go on your return.

It's because of this certainty that it can be attractive.

0 -

Because it protects you from a potential larger loss on a MMF and larger risk (but potentially larger return) on an equity fund.

loose does not rhyme with choose but lose does and is the word you meant to write.0 -

Worth remembering that the real returns of T27 and T28 are relative to RPI inflation. RPI is typically on average about 1% higher than CPI inflation. At the moment RPI is 3.8%pa and CPI 3%. So still possible they would provide a real return over CPI inflation.

Note the official tradeweb real returns based on around the very close of business yesterday were -0.47% for T27 and -0.13% for T28, figures I agree with.

The real returns based on those lategenexer closing prices should be -0.45% and -0.12% for T27 and T28 by my calculations, not -0.76% and -0.34% so not quite as negative.

And T27 and T28 have both fallen in price today (so their real yields will have increased)

I came, I saw, I melted1 -

Many thanks to all for the explanations - All very useful.

0 -

one more perhaps…again assuming the 100K withdrawal every year for 5 years and the Streamlit yield curves for ILG and conventional gilts - break even rate suggests @ 3.7% (4.2 - 0.5).

Simplistically perhaps, were I to think average inflation over the next 5 years will be higher than 3.7%, then am I right in thinking ILG would be the better bet, and conventional if not.

0 -

Yes, if held to maturity.

0 -

Also on streamlit you have to enter your expected return on cash as the gilt maturity dates don't align with the notional income dates.

I think....1 -

Fair point. I guess this is - in my case - whatever interest rate Bell pays on the cash account?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards