We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Income tax and Car allowance - Tax trap

Hey all.

Struggling to get a straight answer out of my finance team so thought i'd ask you clever people.

I've been lucky enough to receive a decent pay rise this year and also a good bonus - Good news!

However

This now trips me over the £100k threshold into what i've seen described as the tax trap. As a result i am looking at options to reduce my taxable income without actually harming my take home pay (which i need every penny of!).

I understand i can increase my AVC and SIP share contributions, which is one option but better for long-term saving than short term disposable income.

My questions

- I get a car allowance, which i currently take as a cash payment

- If i was to take a company car rather than cash, would this reduce my taxable income directly (if so is it the £550 allowance or the £330 pos-tax that gets reduced?

- How does the BIK play in?

Janet and John level responses please to keep this really simple!!

Many thanks to all you wonderful people in advance !!

Comments

-

Your taxable income would decrease by £550/month but would increase by the car-related BIK.

1 -

The BIK charge will depend on what car you get.

https://www.gov.uk/tax-company-benefits/tax-on-company-cars

0 -

Simple Answer.

Company car would be a 'benefit in kind' so you would be taxed on it depending upon the list price of the car and emissions. There was a big incentive for electric cars but this is reducing every year. You would be taxed on a company car that would never be yours.

Most calculations would work out that a company car is not a way of saving tax.

Getting an allowance at least lets you pay towards your own car. If you ever leave your work you will have a car to take with you.

1 -

Are you expecting to exceed the £100k for 2025-26 tax year, or only from 2026-27 tax year onwards?

I ask because a pay rise late in the tax year might not trip you over the threshold if there is only 2 or 3 months at the higher level.

If you are looking to mitigate the tax liability this tax year (2025-26) you are probably too late to switch from car allowance to car because these things take time. Your best option, if it is available to you and if the employer can process it in time will be SS pension contributions.

In trying to get your taxable income below the £100k threshold, consider any other income that might impact your ANI - interest and such like.

As to the question about changing the car allowance for a company car. It is more complicated that a very short answer so I will try to do my best and also try to keep it simple.

- You currently receive £550 per month car allowance. That is £6.6k per year, subject to NI and income tax at the appropriate marginal rates.

- If you give up the car allowance for a company car, your salary (hence your ANI) reduces by that £6.6k.

- You then get a company car which will be subject to BIK taxation. Your ANI will then increase by the relevant BIK. How much the BIK is will depend greatly on the car - list price and fuel type.

- The most tax advantageous type of car will be fully electric to get the lowest BIK. Assume an EV with a (P11D) list price of £40k. 2026-27 will be at 4% BIK, so £1.6k.

- Switching from the current car allowance (£6.6k) to the £40k EV (£1.6k) will reduce your taxable income by £5k (£6.6k - £1.6k).

In considering this, have to considered and claimed any tax allowances that allow you to reduce your ANI? The most immediate one to consider would be whether there is any business mileage and you that is reimbursed by your employer.

Finally, and given the short time until the end of this tax year, have you considered working less? Would you be able to take a short time of unpaid leave before the end of the tax year so that you get back below the £100k?

How far over the £100k are you and do you currently benefit from free child care hours for your children (if you have any)? If you will trip over by a small amount this year, but stand to lose childcare, you might consider more substantial measures to get back below £100k ANI.

1 -

Assuming you're referring to the tapering of the Personal Allowance then there is no need for you to reduce your taxable income.

Personal Allowance is based on adjusted net income so there are ways around it that don't necessarily involve a reduction in taxable income.

0 -

Pls elaborate? Yes i think i am talking about the adjusted personal allowance as a result of tripping over. What are the 'ways around it' please?

0 -

And in response to other queries i accept this has come too late for this year and is only likely to be an issue going forwards.

If i have gone from e.g. 95k to say 105k am i correct in saying that the extra tax burden is only on the 5k over?

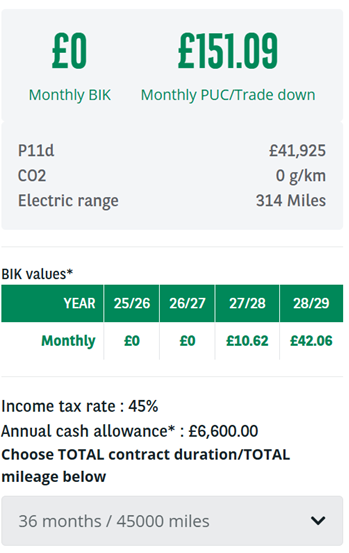

Also - thanks to all on the guidance on the car. If i can find an option with relatively low BIK i wonder if that might be a way forward? A tesla is currently £0 BIK on my scheme for example albeit with a £150 trade up. Overall i think i'd be in a better place perhaps? £550 pm less on ANI, £0 BIK adjustment, £150 trade up so £300 overall ANI adjustment? Is that correct?

0 -

Relief at source pension contributions or Gift Aid donations.

They both increase your basic rate band and also reduce your adjusted net income. They do NOT reduce your taxable income.

0 -

That is not correct.

If you have a Tesla today, the BIK will be at 3% of the (P11D) list price.

That will increase to 4% of the list price from April 2026.

5% from April 2027.

The days of zero-BIK EV are passed.

Future tax rates are subject to change.

You are correct that the higher rate tax will only apply to the £5k above £100k. In fact, assuming not Scotland, you will still be in Higher Rate Tax (40%) but the withdrawal of the Personal Allowance makes the "effective" tax rate for that £5k at 60% plus the benefit of paying 2% NI on that amount, so for the £5k income you get £1.9k in extra money in your pocket.

Hence, the attractiveness of extra pension contributions, unpaid leave, gift aid donations and such like.

EDIT TO ADD - If you are impacted by the withdrawal of childcare at the £100k threshold, that is a cliff-edge so the extra £1.9k in your pocket has cost you a lot more than that.

0 -

Thanks again - all really useful. I'm intrigued by the "relief at source contributions" - who qualifies and how do you apply. FYI i'm part of a big company standard payment plan.

I'm not current effected by the childcare aspect (kids are older) but that may change soon as i'm in the process of adopting.

The BIK question must be unique to my scheme or maybe its because its an older car (24) as per below image. the bit i'm struggling with (sorry) is whether the £550 reduction in taxable income offsets the 151 trade up so that i am better off overall e.g. £550 cash increases my taxable income by ~6.6k per year. Reducing this would bring my Annual income below the £100k threshold and save me £XX. However i then have to pay the £151montly trade up. Overall how can i calculate it better or worse???

Sorry if i'm being thick - I'm a sales man not an accountant !!!

0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards