We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Drawing down one pot and continuing to pay into other SIPPs? plus backdated contributions questions

Hello again, hoping some forumites can help confirm how things work in terms of continuing to pay INTO a personal pension in the same year as taking some funds OUT (via drawdown) of a different personal pension (both DC not DB pensions). Also, I have some associated questions on paying personal pension contributions for previous years where I haven’t already used up my allowance. I’m not very knowledgeable on all this stuff! I turn 58 this year by the way.

As my earnings will be so low this tax year (2025-26), prob under £2k, it seems like a good idea to cash in one of my personal pension pots of around £10k (detailed in this recent post) as I could use up my full personal allowance, and thus end up not actually paying any income tax on the usually “liable for tax” 75% portion of this pot (approx. £7,500)

I have some extra questions:

- Today’s value on the pension pot in question (a legacy one I haven’t contributed to in many years) is only just under £10k – the £10k threshold is crucial under the small pots rule so as not to trigger the MPAA reduction, correct? Is the day that I request the drawdown, the day that the value is set or should I request to withdraw £10k only?

- Can I continue paying into other SIPPs in the same year that I do this, and indeed in the next couple of years? I’m trying to get to grips with the “pension recycling” rules and it seems unlikely that this will come into play on this occasion. The 25% TFLS here would be around £2,500 and apparently one of the pension recycling criteria is to have received a TFLS of at least £7,500?

- After triggering the drawdown of this pension pot, am I also still allowed to make backdated pension contributions (not sure if this is up to date terminology) for the last few years? As a self employed person I have not used up anywhere near my full annual allowance for pension savings in the last three years

- I understand that the maximum I’m allowed to contribute each year is equivalent to my annual earnings (apart from the low/no earnings one of £2,880 net which is what I'd be looking to contribute for this year. My previous years' annual earnings (2022-23/2023-24/2024-25) were higher than this year, but always still way below the £40k/£60k pa allowance. Presumably the “earnings” figure that I use should NOT include savings interest income, just my sole trader net income?

Thanks for any clarification on how this all works!

Comments

-

I think you have misunderstood the MPAA rules. Any amount of taxable money taken from a DC pension will trigger the MPAA. Bearing this in mind you're going to have to rethink the whole strategy.

0 -

MPAA not triggered if you use the small pots withdrawal method, which I think the OP is referring to when he is mentioning only wanted to take 10k. This is a specific method and you must make sure the proivder is using the small pots rules, its not as simple as just withdrawing 10k (or less) from a pension.

3 -

And you can never make pension contributions for a previous tax year. Once the year has finished (or the point your pension company will allow contributions has passed) then you have missed the boat for that tax year.

0 -

Ah yes, thanks for the correction.

OP: It is possible to put more than £60k into a pension and still get tax relief. However you are still capped by the amount you earn this tax year. So even if you have lots of carry over and you earn (for example) £50k this year then you can only pay £50k into your pension, not more than that. If you were to earn say £100k and you had £40k or more carryover available then it would be possible to pay £100k gross into a pension and get tax relief on all of it.

0 -

Really?? I am now feeling very confused about this point… have been searching around for info on this point today and read the following on this HL page headlined "Pension Carry Forward" (in my case the annual allowance would obvs be my "earnings" figure instead - or that was my understanding!).

Can you backdate pension contributions?

You can carry forward unused annual allowances from the three previous tax years, as long as you were a member of a pension during that time. In the last two tax years, the annual allowance was £60,000 for most people, and in the tax year before that it was £40,000 for most people.

It can be confusing, so here's an example to show you how it works. Remember though, you normally need to be at least 55 (57 from 2028) before you can access money in your pension.

Tax year

Annual allowance

Contributions made

Unused allowance

2022/23

£40,000

£15,000

£25,000

2023/24

£60,000

£5,000

£55,000

2024/25

£60,000

£20,000

£40,000

2025/26 (current)

£60,000

£60,000

£0

0 -

That is all about carrying forward unused relief from previous years.

A totally different concept to making contributions for those previous years.

Before getting embroiled in this aspect any further do you actually earn enough to be able to contribute more than £60k in the current tax year. This isn't a question about whether you have the funds available, it is about the rules for carrying forward unused relief.

You mentioned earning less than £2k so I fail to see how carry forward is a viable option for you in this current tax year 🤔

1 -

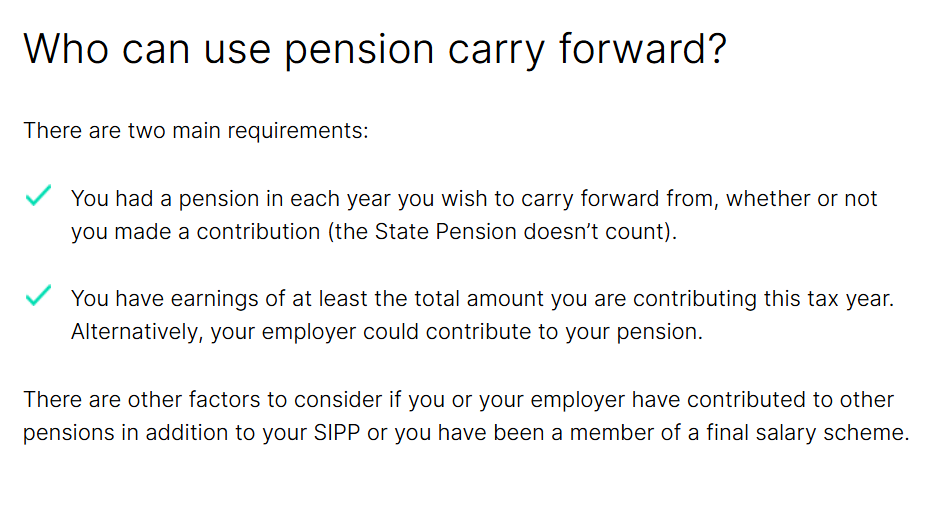

From the same link the OP provided :

Note the second requirement. As Dazed_and_C0nfused has explained

2 -

Apologies if I used the wrong terminology, I thought I had explained it carefully. To try and clarify on that particular area:

- no, I don't earn enough to contribute more than £60k this tax year, I earned a very low amount (winding down to retirement) this year and therefore want to contribute the max £2,880 net for 2025-26

- after I've done that, am I allowed to carry forward unused relief for previous years? eg make a further contribution for 2024-25 where the difference between pension contribs I made that year, and my earnings (way below £60k), was about £2,500

- and in particular, is the above affected by having drawn down £10k this year?

0 -

You don't carry forward unused relief, your earnings in previous years are irrelevant.

You carry forward unused allowance, however, to make use of this allowance you need enough earnings in the current tax year to use it.

1 -

If you can't cannot use your normal annual allowance of £60k (which you clearly can't) then you cannot use carry forward.

What use would carry forward be if you have this year's allowance left unused 🤔

You still seem to talking about making contributions for tax years that have ended when you cannot do that.

The impact of the existing withdrawal would depend on whether you specifically used the "small pots" rule but as you only earn £2k it is in reality unlikely to be a factor, you will be limited to a gross contribution of £3,600.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards