We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

State Pension Forecast and Buying Years

A couple of years ago my wife checked her state pension forecast and was missing a couple of years, we duly paid the amounts which brought it up to date and she was then showing a full pension.

We've just checked now and because she now has more missing years ( she doesn't work, doesn't claim benefits etc ) it's saying she's about £1.80 a week short.

She's only 56 and not intending on going back to work - does this mean that as each financial year passes her "full" pension will get reduced unless we pay each year?

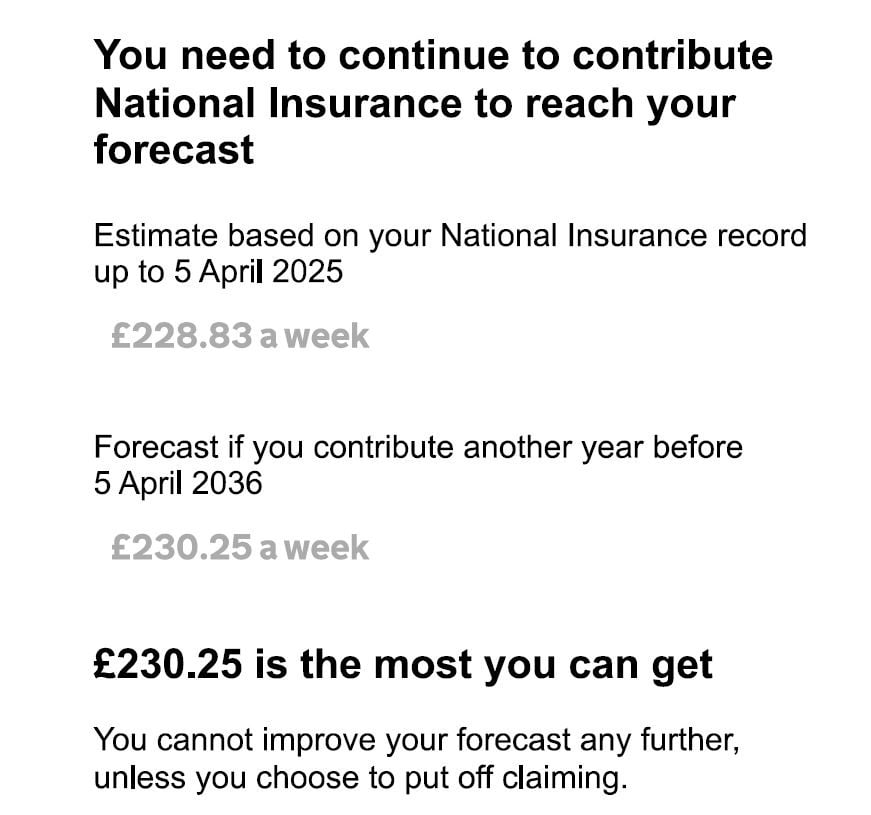

I've added a screenshot which seems to say she can't do anything to improve this position - in which case can she not now pay for the years?

Comments

-

Do you have the screenshot showing she had in fact accrued the standard new State Pension?

0 -

I've added a screenshot which seems to say she can't do anything to improve this position - in which case can she not now pay for the years?

It says the current record is £228.83 and over the next 10 years, your wife needs just one year to qualify for the maximum.

If she isn't going to work or qualify by other means, then the £228.83 applies (ignoring indexation here).

You may take the view that its not worth making up that difference as the extra year at £923 would take about 12 years to breakeven. Normally £923 buys you around £6.58 pw. It is not discounted if you only need £1.42.

That is possibly why you never paid for that one extra bit. It is very common for people to only pay extra for the full entitlement (or amounts close to full) but not pay for the tiny bit of difference.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

The wording is precise and accurate. £230.25 is the current value of a full state pension.

She can pay for an extra NI year voluntarily but if she does so the only beneft she would get is an extra £1.42 a week state pension which is arguably not worth the effort/cost - it would take about 12 years to break even.

1 -

Her pension cannot be reduced by not paying, what is showing is what she will get, you do not have to keep on paying.

Are you sure that she did in fact top up to the full amount, not just filled what was available at the time - did the forecast actually state she had reached the full amount ? What years did she fill - the shortage is roughly the difference between 2 contracted out pre 2016 and 2 post 2016 years in value. Any screenshots ? - one thing I always did was screenshot / download the new forecast. Or maybe she is one of those, as mentioned in the news, whose forecasts were incorrect and have now been corrected. Without going into fairly microscopic detail it will be difficult to see what has happened. Maybe posting up the usual points may help to form some sort of opinion

Number of full NI years 15-16 and earlier

Number of full NI years 16-17 and later

Any COPE amount. If you have "You've been in a contracted-out pension scheme" on your forecast then click

here https://www.tax.service.gov.uk/check-your-state-pension/account/cope whilst logged into your tax account

Years which show not full0 -

Thanks for the help - thinking about it there may have been an odd £1ish that we didn't pay - based on the fact that it would cost £923 for a whole year, the additional £923 would take 650 weeks or 12+ years to get the money back, taking her to 79…

0 -

It may have been the right choice for her but just remember it will be an ever increasing disparity as each year passes.

Now £1.42/week but closer to £1.50/week from April.

0 -

When we were buying we looked at the overall repayment period, the big picture, rather than how long it would take for each year to be repaid. In your case, using today's amounts and a £907.40 year cost, 2 years would cost £1814.80 and pay £13.16 per week so 138 weeks payback, 3 years would cost £2722.20 and pay back £14.58 per week so taking 187 weeks, only 49 weeks longer to recover the whole outlay.

0 -

Yes when I topped up in 2022 I was £2.85 pw shy of the max. Now I am £3.55 pw shy. At this rate it may be worth me topping up the extra year.

1 -

But presumably the cost of topping up a year will be increasing at the same rate, i.e. the payback period should remain constant?

0 -

Interesting thought since the cost seems to move in fits and starts. Back in 2022 the cheapest year was £795.60 but most were £824.20. Now I have a few at £907.40. So it has gone from costing 289.2 weeks of the increase in the pension to costing 255.6 weeks of it. Of course I am comparing a cheap rate to an expensive one but still.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards